Fed Seeking to Find Where ‘Phantom Menace’ Neutral Rate Sits

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFederal Reserve Chair Jerome Powell and his colleagues are on the march to return ultra-loose monetary policy and accommodative financial conditions to more normal levels. The trouble is, their destination is uncertain and the terrain may be shifting as they forge forward with higher interest rates.

Policy makers differ on what the neutral rate -- the rate that neither restricts nor spurs economic growth -- is and couch it in terms that don’t take account of the current high inflation environment. And they’re unsure what effect their removal of monetary largess will have on fickle financial markets and an economy that have grown accustomed to ultra-low rates.

“I doubt that anyone can say with confidence where neutral is,” said Allianz SE chief economic adviser Mohamed El-Erian.

That increases the risk that the Fed will make a policy mistake, either by raising rates too high and pushing the U.S. into recession or by not increasing them enough and allowing elevated inflation to become endemic.

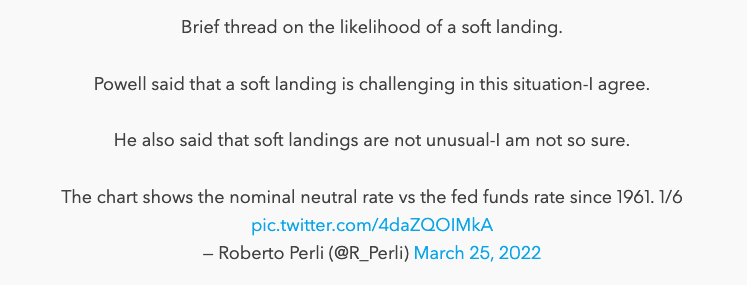

Stifel Nicolaus & Co. Chief Economist Lindsey Piegza puts the risk of an economic contraction within the next 21 months at well over 50% as the Fed tightens credit into a slowing economy. Roberto Perli of Piper Sandler & Co. reckons that over the past 35 years the economy faltered nearly every time the Fed reached or exceeded neutral.

In his first speech at the Fed’s annual Jackson Hole conference in 2018, Powell highlighted the uncertainties surrounding such economic concepts as R star, or the neutral rate, saying they are imprecise and subject to revision,

Where R star sits is often so elusive that St. Louis Fed President James Bullard once referred to it as the “The Phantom Menace,” using a line from Star Wars. It can be influenced by forces such as demographics, inequality, savings, inflation expectations, productivity and the fabric of the labor market, all of which are sometimes hard to interpret in real-time.

The Fed’s push toward higher rates received fresh impetus Friday with the release of another strong jobs report. The U.S. added 431,000 jobs in March while the unemployment rate fell to 3.6%, near its pre-pandemic low, according to the Labor Department.

After lifting rates from near zero by a quarter percentage point in March, Powell & Co. have signaled their readiness to press ahead expeditiously toward a more normal setting for monetary policy, and then perhaps beyond, where the level of rates holds back the economy and slows down growth.

As set out in its Summary of Economic Projections released on March 16, the median forecast of policy makers sees the federal funds rate rising to 1.9% by the end of this year and 2.8% by the close of 2023.

Policy makers probably can coalesce around doing two or three 50 basis-point increases in the near-term because they all agree that rates are well below neutral and inflation is much too high, said Vincent Reinhart, chief economist for Dreyfus and Mellon.

“The case for 50, barring any negative surprise between now and the next meeting, has grown,” San Francisco Fed President Mary Daly told the Financial Times in an interview conducted on Friday. “I’m more confident that taking these early adjustments would be appropriate.”

As rates approach more normal levels, it may be tougher to build a consensus on forging ahead, especially if President Joe Biden’s yet-to-be-confirmed nominees to the Fed board prove as dovish as expected, Reinhart said. Goldman Sachs Group Inc. and Citigroup Inc. economists are among those who see the Fed’s rate peaking at 3% or above.

One problem, according to Philadelphia Fed President Patrick Harker: “We don’t even agree on what neutral is.” Estimates in the SEP for neutral, or so-called R star, range from 2% to 3%, with a median of 2.4%.

Those estimates are predicated on inflation being at the Fed’s 2% target. It’s far above that now: The personal consumption expenditures price index, the Fed’s favored inflation gage, rose 6.4% in February from a year earlier. And it’s expected to be about 3% over the next five years, based on trading in Treasury securities.

That suggests that the neutral rate that the Fed is shooting for is above 3%, not comfortably below it, according to former Fed Vice Chairman Donald Kohn.

Further complicating the picture: The U.S. central bank plans to begin reducing its $8.9 trillion balance sheet sometime in the coming months. Harker told a March 29 webinar that a $3 trillion drawdown in the balance sheet over time would be equivalent to around two, quarter percentage-point increases in the federal funds rate, though he stressed there was a lot of uncertainty surrounding that estimate.

What’s ultimately important for the economy though is not the level of the fed funds rate, per se, but the financial conditions it engenders through changes in stock, bond and other asset prices. Those shifts impact the ability and willingness of consumers and companies to borrow and spend and thus shape the course of the economy.

“It’s a little mysterious about what’s going on” in financial markets, Kohn said. Financial conditions have tightened since the Fed pivoted in a hawkish direction, but not by a lot. Yields on Treasury securities have risen, yet real, inflation adjusted rates are still negative. Stock prices have fallen, but are not that far off record highs.

What Bloomberg Economists Say

“The Fed hikes at every meeting for the rest of 2022, with one 50 basis point move,” taking the benchmark to a 2% to 2.25% range by year-end, with a further percentage point of tightening in 2023.

-- Anna Wong, chief U.S. economist

Kohn, who is a senior fellow at the Brookings Institution, suggested that the financial markets may need to weaken further to help the Fed bring demand in the economy more in line with supply and reduce inflation. “There could be some interesting times in financial markets ahead,” he told a March 30 webinar convened by the American Enterprise Institute.

Because the markets have gotten so hooked on ultra-easy monetary policy, it’s hard to know how they’ll react as rates rise, Bloomberg Opinion columnist El-Erian said. That in turn is why it’s so difficult to pin down the level of the neutral fed funds rate.

But it’s where policy makers say they are headed -- even if they all don’t agree on exactly what that entails.

“Clearly, we need to get something more like normal or neutral, whatever that means,” New York Fed President John Williams told an audience in Princeton, New Jersey on Saturday.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All