The popular 60/40 portfolio isn’t dead, and in fact is a significantly more compelling investment than cash over the coming decade, according to JPMorgan Asset Management.

Higher long-term bond yields will allow the Fed to do less on short rates.

The third largest ETF recently reached the age of 13. Yes, the Vanguard 500 ETF (VOO) is now Taylor Swift’s lucky number. (Am I one of the first people to use Ms. Swift and Vanguard ETFs in the same sentence?)

Some investors are considering making tactical tilts to their fixed income portfolios to take advantage of the current high-yield environment.

Jeff and Ron Muhlenkamp give an update on the relevant economic indicators impacting investments. They also provide their thoughts on inflation, the possibility of a recession, and a list of things “broken” by the Fed due to it raising interest rates.

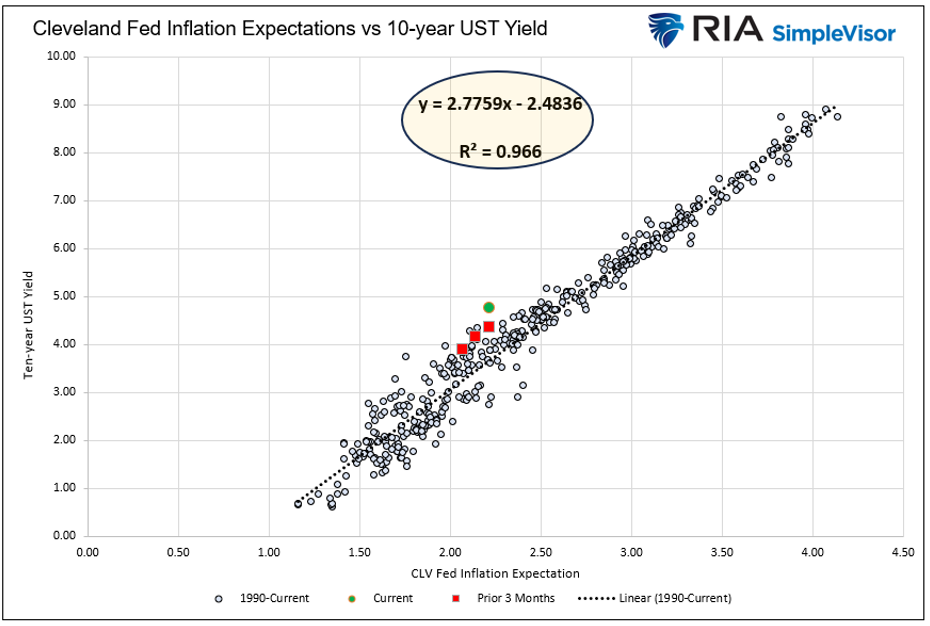

This article discusses one of my favorite bond fair-value models to show you the true bond-yield signal.

The Federal Reserve faces potential policy pitfalls ahead as it wrestles with how to respond to investor angst about the US government’s $33.5 trillion mountain of debt.

Treasury-market liquidity has mostly righted itself since the dislocations caused by the several regional bank failures in March, according to a Federal Reserve Bank of New York economist.

Muni bond ETFs gathered $6.3 billion in the first nine months of 2023. However, a healthy $1.4 billion flowed in during September alone. According to Columbia Threadneedle, there is good reason to focus on the asset category.

Interest expense is a large and growing issue for both the economy and stock market, which reinforces why investors should stay up in quality amid interest-rate-driven headwinds.

Research Affiliates’ Rob Arnott offers his views on the current market environment and the future of smart beta. VettaFi’s Tom Lydon discusses the recent fake bitcoin ETF news, equity market technicals, TLT inflows, and ETF stories to watch the remainder of the year.

Howard Marks, the legendary credit investor and Oaktree Capital Management co-founder, has historically taken a humble approach to investing: the macro future is essentially unknowable, so active investors should focus on the small-picture things where they can gain an informational advantage.

A robust earnings season could be all it takes to fuel a year-end rally on Wall Street, eclipsing recent jitters from geopolitical tensions.

Municipal bonds sold off considerably in September alongside vastly rising interest rates.

Value-conscious, historically-informed, full-cycle investors place a great deal of emphasis on the relationship between the price an investor pays today and the cash flows they can expect to receive in the future. The reason is simple.

The High Yield Bond category is up 5.9% through September, ranking it among the best performers in the fixed income space. Payden & Rygel’s Jordan Lopez and Nick Burns outline three factors contributing to the market’s strength.

How worried should we be about AI and what should we do about it? There is risk on both sides: of not taking warnings about AI seriously enough, and of taking them too seriously.

Psychology in markets is always fascinating. In February 2009, I wrote “8 Reasons For A Bull Market.” While in hindsight, it is easy to see that was the right call, overall, psychology was highly negative at the time.

JPMorgan Chase & Co. Chief Executive Jamie Dimon calls it “over-earning,” but his isn’t the only bank that still hasn’t felt much pain from loan losses or rising deposit costs

Florida’s farmers have spent nearly two decades fending off plagues, freezes and storms that decimated their orange crops. A growing number of them have had enough.

Investors are growing more confident that a year-long slump in profits for Corporate America is about to end. Yet a fragile economic outlook, wary consumers and the highest interest rates in 16 years mean any relief for stocks could be short-lived.

A money market fund is a type of mutual fund that invests in debt securities, specifically those characterized by short maturities and minimal credit risk. A money market fund generates income with little to no capital appreciation, making it a low-risk, low-return investment.

Our September Cyclical Forum was the first to be held in London, where the economic situation today reflects what’s happening around the world.

As a strategist, I work with financial advisors every day creating custom fixed income portfolios based on client’s financial needs and goals – with a keen eye on the importance of a balanced portfolio.

“Restrictive for longer” is now the mantra as monetary policymakers seek to bring inflation reliably to target.

US housing affordability worsened to a fresh record low in August as Americans continue to bend under the weight of soaring mortgage rates and sticky prices.

When US banks kick off the third-quarter earnings season Friday, it will mark the first in a long line of hurdles the group needs to clear in order to assuage investor fears.

As the second quarter came to a close, the Fed’s elusive soft landing appeared to be within reach. However, inflation resurfaced during the third quarter, substantially complicating the near-term economic outlook.

Savvy investors are aware that geopolitical tensions and uncertainty can significantly influence the financial markets.

Reverting to old fiscal rules will create a strong economic headwind for Europe.

The spike in bond yields presents an opportunity for fixed income investors to earn capital gains and diversify portfolios.

After three quarters of improving economic outlook amid increasing expectations for a painless decline in global inflation, markets and pundits alike have become less optimistic about a soft landing as they reacted to frustration from the Fed.

With all eyes on generative AI (genAI) and its transformative potential, individual investors’ interest has been piqued. The market-moving innovation certainly has generated a lot of hype ― and questions. Equity CIO Tony DeSpirito parses three reasons for excitement and three areas for awareness.

Slower growth and rising interest rates have tapped the brakes on private deal activity this year. But as banks continue to retreat from lending, we see plenty of opportunity for investors to pick their spots across the broad private credit universe.

The first nine months of 2023 have seen significant growth. Despite this growth, questions remain. Income is top of mind as many investors worry about the potential of a recession, the ongoing high-rate environment, and market uncertainty. Enter the Income Strategy symposium.

A liquidity gap is growing as banks curtail specialty lending, providing specialty finance investors opportunities for potential better risk-adjusted returns than we’ve seen since the GFC.

Market pricing, verbal cues from Federal Reserve members and the likely evolution of the economic data over the next couple of months all point in the same direction — the central bank is likely done raising interest rates.

In his latest memo, Howard Marks provides a follow-up to Sea Change (December 2022). He argues that the trends highlighted in the original memo collectively represent a sweeping alteration of the investment environment that calls for significant capital reallocation.

Like a watched pot that refuses to boil, the much-anticipated recession of 2023 has yet to materialize. In our latest Strategic Income outlook, we examine the reasons and discuss what might finally cause the temperature to rise.

Making the case for municipal bonds today with Stephen Dover, Head of Franklin Templeton Institute.

Broadly speaking, large- and mega-cap tech stocks are far from bear market territory. But the Nasdaq-100 Index (NDX) closed 6% below its 52-week high last Friday.

New bank rules will raise borrowing costs and weigh on economic activity.

The Federal Reserve (Fed) only controls one rate of interest, and it is a very short-term rate called the federal funds rate, the rate that banks charge each other for overnight, intra-bank loans.

The quarter started off strong enough in July but gave up ground in both August and September. The total return of the S&P 500 was down 3.27% for the quarter.

One and three hundred years before the enormity of the present dilemma began to dawn on the Federal Reserve, a similar moment arrived within the stone walls of the Banque Royale. You may recall the scene we visited last year.

The odds of a unicorn spraying rainbows across the sky and the government running a surplus are the same: zero percent.

Stock markets that have refused to buckle under the highest yields since 2007 face a new test. Third-quarter results will shine a light on how much those rates are already hitting profits — and what they’ll do to lofty equity valuations.

After investment losses tore through the US financial system this year, a fresh slump in bank stocks shows some investors fear the problem — which at its most extreme claimed a handful of lenders — hasn’t gone away.

Three major housing-industry lobby groups called on Federal Reserve Chair Jerome Powell to refrain from raising interest rates any further and to pledge against selling mortgage bonds unless real estate financing stabilizes.

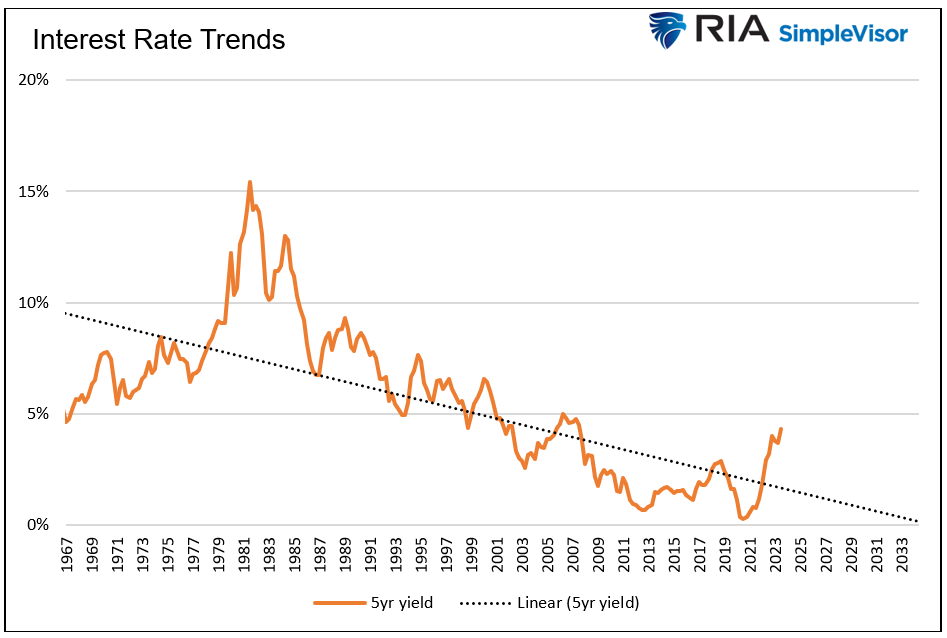

The recent repricing in longer-maturity yields has pushed the 10-year Treasury yield to levels not seen in 16 years.