New bank rules will raise borrowing costs and weigh on economic activity.

It’s been more than six months since the failure of Silicon Valley Bank (SVB). Fears of another financial crisis have, thus far, been unrealized. The Federal Reserve and the U.S. Treasury Department deserve great credit for dealing with the situation swiftly and effectively.

Overseers of the industry have been working through lessons learned, and proposing measures designed to prevent a recurrence. The result could be the biggest wave of banking re-regulation since 2010, which would have a substantial influence on the flow of credit through the American economy.

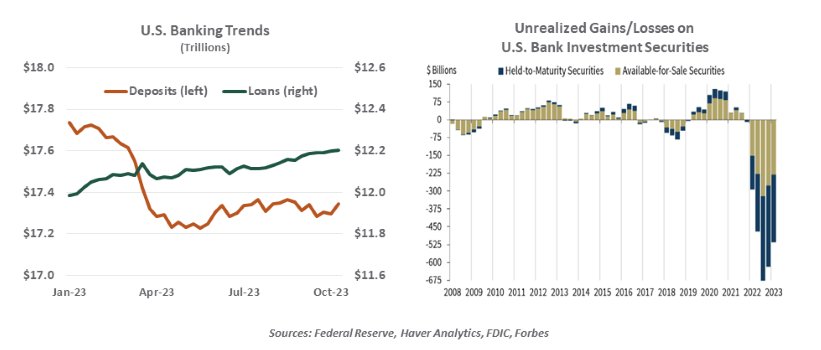

Interest rates are a primary driver of bank performance. They influence the yields earned on loans and the cost of deposits. Higher rates can lead to more credit defaults and limit underwriting revenues. The movement to higher yields diminishes the value of securities that banks hold as sources of liquidity.

Over the past 18 months, interest rates have risen rapidly, more rapidly than expected. Yields on bank assets have increased, but so has the cost of deposits. Banks that failed to pay up aggressively to keep their deposits saw some of them migrate to money funds.

For most financial institutions, the higher interest rate environment has been unwelcome but manageable. Banks actively monitor their exposure to interest rate changes, and adjust their investment and hedging strategies to limit risk. Banks maintain reservoirs of marketable assets which can be used to generate liquidity when deposit balances are declining, keeping maturities short enough so that funds are readily available. Regular stress tests of interest rate risk and liquidity are conducted to identify any weaknesses.

For a few firms, like SVB, higher interest rates proved fatal. The bank had invested monies in much longer-term securities; when deposits began to decline, they were forced to sell the securities at a loss. This news accelerated client flight; once the psychology around the situation turned negative, it was impossible to arrest. This year’s bank failures cost the Federal Deposit Insurance Corporation (FDIC) more than $30 billion, which was about one-quarter of the FDIC’s reserves.

In the wake of all of this, bank regulators have taken a series of steps:

· A special assessment has been taken to replenish reserves in the deposit insurance fund. Large banks have paid the lion’s share.

· Institutions have been encouraged to review their vulnerability to rapid losses of funding, and to increase the amount of short-term liquid assets held as a contingency.

· The FDIC has proposed that large banks be required to issue additional amounts of long-term debt, which can serve as a source of liquidity and provide additional loss-absorbing capacity.

· The Federal Reserve has proposed that a wider range of big banks count unrealized losses in investment portfolios against their capital ratios.

· U.S. regulators announced plans to migrate to the latest edition of international capital standards, which will require firms to hold larger buffers against the risks that they take. The new rules will be phased in over the next several years.

Ensuring that problems at private sector banks do not require public bailouts is a central goal of financial supervision. Liquidity and capital regulations are not only designed to build firewalls between the problems of an individual firm and the financial system, they are also designed to incent strong risk management practices. There are certainly debates over whether measures are well-designed, but their intentions make sense.

Requiring greater buffers of liquid assets and higher levels of capital will increase the rates that institutions will require to extend credit. This may price some prospective borrowers out of the market, and thereby limit economic activity.

Those seeking credit may turn to non-traditional lenders. Private equity pools have made more than $1 trillion in loans that would traditionally have come from banks. These providers are not subject to the same rules and levels of oversight, leaving an uneven playing field and reducing the transparency surrounding financial intermediation.

After a crisis, overseers have an understandable desire to reinforce safety and soundness. But unless it is intelligently designed, new regulation can raise costs without providing a cure.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust