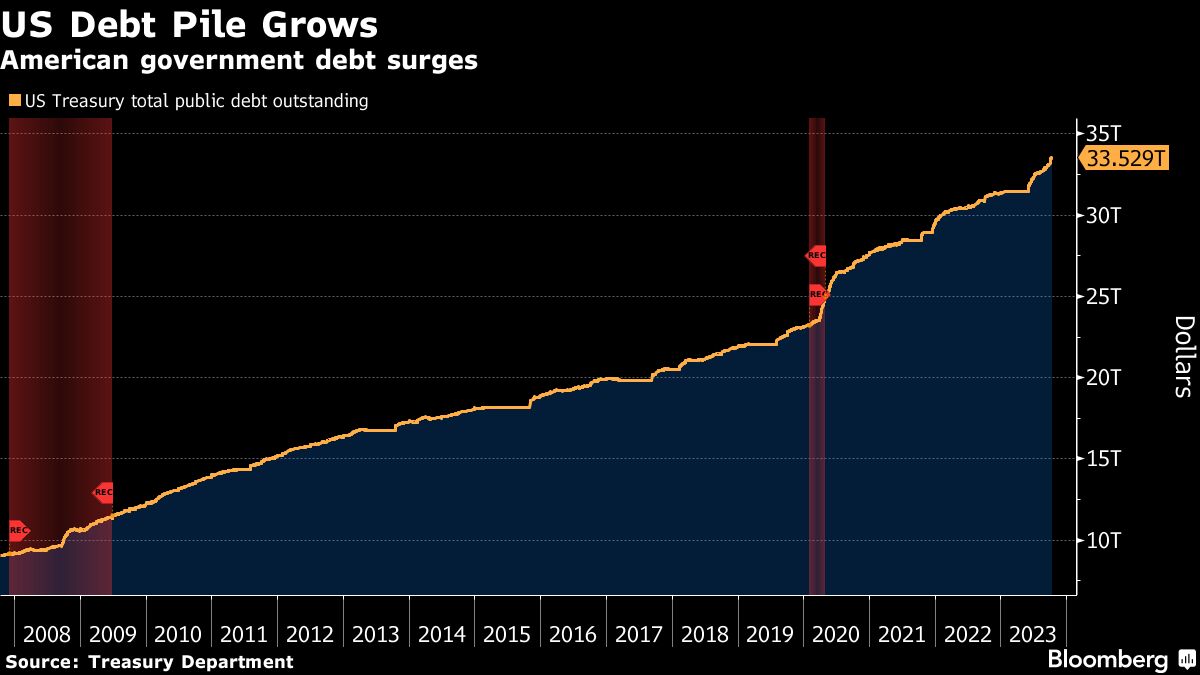

The Federal Reserve faces potential policy pitfalls ahead as it wrestles with how to respond to investor angst about the US government’s $33.5 trillion mountain of debt.

Concerns about America’s fiscal future have already contributed to a run-up in US bond yields that has surprised policymakers and prompted them to consider postponing for now plans for another interest-rate increase.

Worries on Wall Street about the US budgetary morass pose risks to both sides of the central bank’s dual mandate.

The disquiet over deficits and debt puts upward pressure on long-term interest rates, threatening to slow growth and push up unemployment. At the same time, it can also act as kindling for higher inflation, especially if the Fed is perceived as downplaying its goal of price stability in order to limit the federal government’s borrowing costs.

“We are witnessing the beginning of a regime change in how investors perceive America’s fiscal sustainability,” said former Fed Governor Kevin Warsh, who was an adviser to President George W. Bush from 2002 to 2006.

To be sure, there are other forces at play behind a downdraft in bond prices that has driven the yield on the benchmark 10-year Treasury note to 4.83% yesterday from this year’s low of 3.31% on April 6. Prime among them: the resilience of the US economy in the face of the most aggressive credit-tightening campaign by the Fed in decades.

Fed Chair Jerome Powell will weigh in with his views in an appearance before the Economic Club of New York on Thursday.

Fed watchers expect him to tacitly back an emerging consensus among policymakers that the higher yields give them a chance to hold policy steady at their Oct. 31-Nov. 1 meeting as they assess the outlook.

But with inflation still running faster than the Fed’s 2% objective, Powell will likely hold out the possibility of a rate increase later in the year.

What Bloomberg Economics Says...

"The recent surge in 10-year Treasury yields will dampen economic growth, similar to a Fed rate hike. Bloomberg Economics estimates the increase since the Sept. 19-20 FOMC meeting, if sustained, should reduce the need for 50 basis points of interest rates," Anna Wong, chief US economist.

“The threat of another hike will remain with us as long as we’re approaching inflation from so far above their target,” MacroPolicy Perspectives LLC founder and former Fed economist Julia Coronado said.

Ex-Fed Vice Chair Donald Kohn said that in general, Powell and other officials should speak out about the impact of fiscal policy on the economy, interest rates and the central bank.

“It would help the economic conversation in the country if they at least talked about the consequences for monetary policy and the economy,” said Kohn, who is now a senior fellow at the Brookings Institution.

Former Treasury official Mark Sobel — who served under both Republican and Democratic administrations — is blunter. Fed officials need to warn the public about the potentially deleterious impact of US profligacy on markets and the economy, said Sobel, who’s US chairman of the Official Monetary and Financial Institutions Forum, a research organization.

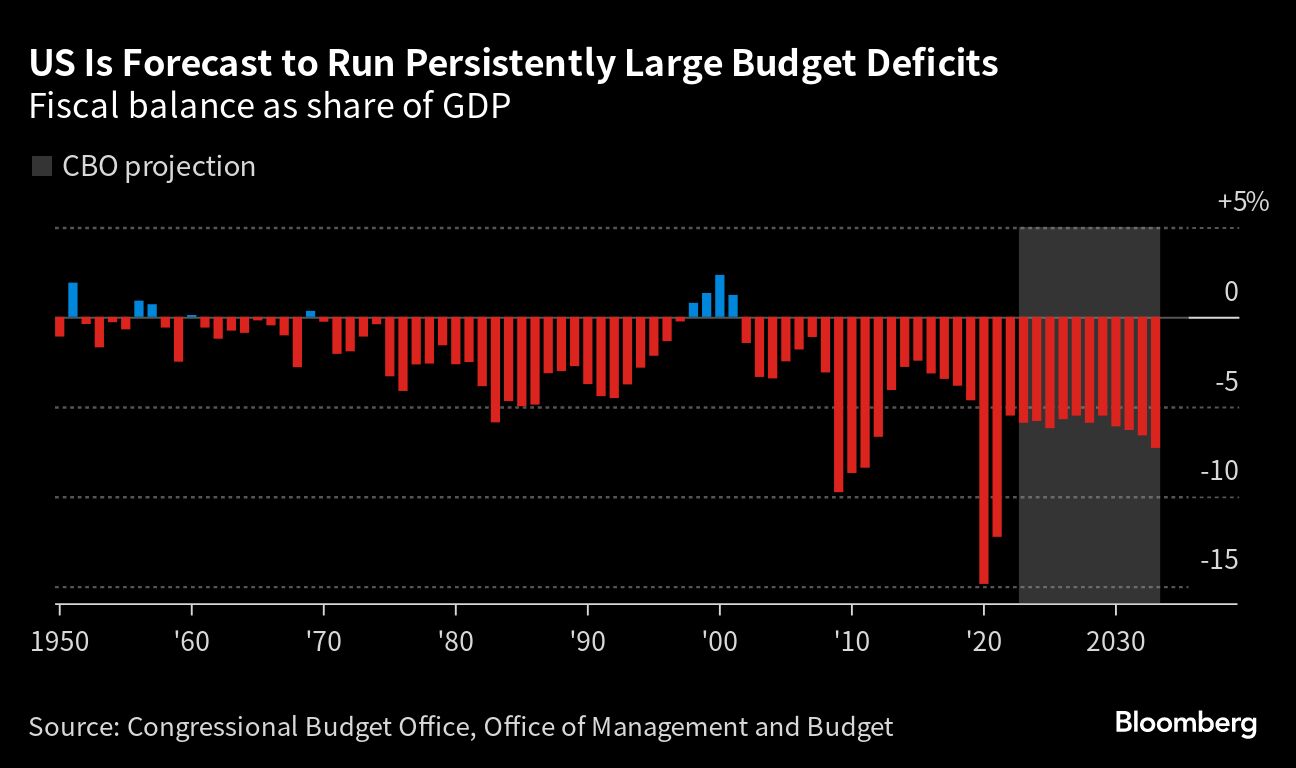

It’s been conventional wisdom for a while that the federal budget is on an unsustainable path of mushrooming debt. But a confluence of recent events has pushed those concerns to the forefront.

In August, Fitch Ratings Inc. stripped the US of its top-tier AAA credit rating while the Treasury announced a bigger-than-expected quarterly borrowing requirement. An estimate last week from the Congressional Budget Office that the deficit jumped by more than 20% in the just-ended fiscal year, to $1.7 trillion, added to the unease.

“It’s just hard to believe that this is a sustainable policy going forward,” Fed Governor Christopher Waller said on Oct. 11 at the E2 Summit in Park City, Utah.

Administration officials insist that President Joe Biden is committed to reducing the budget shortfall and they argue that his initiatives to boost public infrastructure spending and promote private investment to fight climate change will help the economy in the long run.

Other Worries

But it’s not just the mounting supply of Treasury securities that’s spooked investors. It’s also weakening demand. Many investors worry that the two biggest foreign holders of US debt, China and Japan, will scale back their purchases.

The Fed itself is already cutting back, methodically reducing its bond holdings in an operation known as quantitative tightening. And officials have signaled they’ll continue to do so even after they begin expected cuts in interest rates sometime next year.

“The bar is very high” to the Fed veering from that path, Coronado said.

The rise in yields is threatening to make the untenable fiscal outlook even worse, said former CBO Director Douglas Holtz-Eakin, who advised George W. Bush while he was in office.

“We have a super-interest-sensitive budget,” said Holtz-Eakin, president of the American Action Forum. “If the bond market is starting to decipher more accurately the effective fiscal position of the US, then we’re in trouble.”

Warsh agreed. “It’s exceedingly difficult to have sound monetary policy without sound fiscal policy,” the Hoover Institution visiting fellow said. “And US fiscal policy is decidedly unsound.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Rich Miller