Reverting to old fiscal rules will create a strong economic headwind for Europe.

For years, euro area countries could not agree on when it was appropriate to breach fiscal limits. The pandemic and the Ukraine war changed the game: suspension of debt and deficit limits in the wake of those events proved instrumental as Europe sought to avoid an economic and political catastrophe.

With the economy moving beyond these exogenous shocks, age-old differences in economic thinking between the north and south of Europe have come to the fore again. As a result, negotiations on reforming budget rules set out under the Stability and Growth Pact have stalled.

The European Commission’s (EC) proposal is to reinstate the original Maastricht Treaty targets of deficits under 3% and debt under 60% of gross domestic product (GDP). But the proposed reform offers more flexibility when a country breaches one or both of these thresholds. Instead of a rigid, formulaic approach, regaining compliance will be negotiated on a case by case basis. Plans will be unique to each member state and based on a debt sustainability analysis. The plan also aims to provide states four years to reduce their debt/GDP ratios, or seven years if they also undertake reforms and investments that are in line with Europe’s strategic priorities, instead of the current uniform 1/20th debt deduction rule.

There are two major sticking points around the EC’s proposition. Germany, along with other northern states, is pushing for fixed spending caps and yearly reduction targets. On the other end of the spectrum are nations like France and Italy, which favor negotiated debt reduction paths instead of a one-size-fits-all approach. Member states are also at odds over how much enforcement power the EC should have if countries fail to hit planned targets.

If no agreement is struck by the end of the year, the former fiscal system will apply in 2024. Compliance with the old framework is untenable for several countries. Up to ten member states are at risk of being placed in a corrective Excessive Deficit Procedure (EDP) in 2024. Though the EC could use its discretion over how rigidly it enforces the rules, an EDP would create substantial fiscal headwinds for a number of countries. This would have economic, political and social consequences.

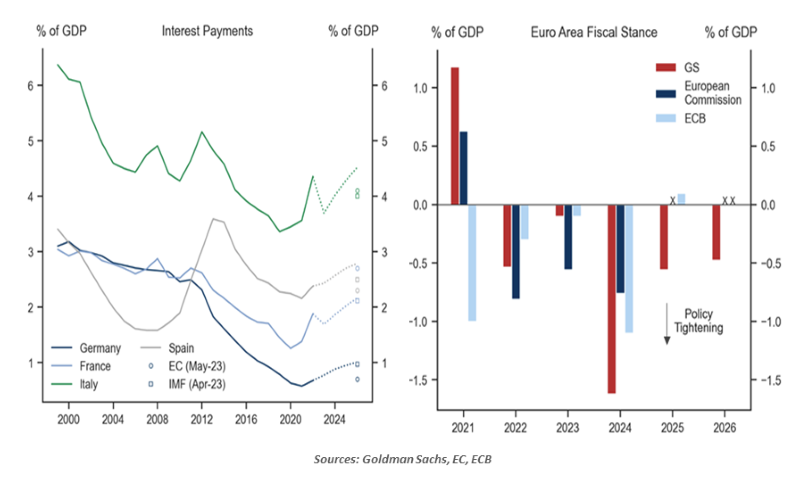

Persistent inflation and the resultant higher-for-longer interest rate environment will continue to add to fiscal pressures and debt risks across Europe. Interest expense as a share of GDP is expected to rise, as yields on newly-issued bonds will be higher than those on current maturities.

A major dilemma for European governments is that fiscal space has declined, while at the same time, the need for more public investment in areas like defense, energy security and climate has increased. While most member states will likely be able to improve their public finances by withdrawing energy support measures, weaker growth and the potential public backlash against more austere policies will prevent a meaningful tightening.

Europe needs to reform its fiscal framework, with the objective of striking the right balance between sustainable debt reduction and ensuring room for investments to deal with evolving challenges. Alas, the bloc is letting a once in a decade opportunity slip away.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust