After investment losses tore through the US financial system this year, a fresh slump in bank stocks shows some investors fear the problem — which at its most extreme claimed a handful of lenders — hasn’t gone away.

Unrealized losses on bank securities’ portfolios will likely increase in the third quarter after a steep rise in yields eroded the value of those holdings, according to analysts. That’s contributed to a sharp decline in bank stocks, with the KBW Bank Index falling 6% since a September Federal Reserve meeting signaled another hike could be on the way. The index is down 23% this year.

“Clearly the run-up in bond yields at the long end of the curve, which has led to the increases in unrealized bond losses, is weighing on the stocks,” said RBC Capital Markets analyst Gerard Cassidy. “The scar tissue is so thick in the long-only investment community from what happened in March, that they’re not ready to come back into the bank stocks in any meaningful way.”

But while such losses likely expanded, they don’t pose the kind of threat that ended up sinking Silicon Valley Bank, Signature Bank and First Republic Bank, according to analysts. Deposits at banks have stabilized, meaning they likely won’t be forced to sell these assets - and crystallize the losses.

“While SIVB continues to be the flashpoint comparison on this topic, we want to emphasize that banks will not be forced to sell one dollar of HTM securities unless there is a material deposit run,” UBS Group AG analysts led by Erika Najarian said in a note. “The reason we think the stocks are rather oversold is that macro funds appear to be back and shorting banks for existential reasons.”

The Federal Deposit Insurance Corp. pegged second-quarter unrealized losses at $558.4 billion, up 8% from the period before. The losses are split between $249 billion in their available-for-sale portfolios and $310 billion in their held-to-maturity books. Currently for the biggest US banks, none of the unrealized losses impact profit, but the ones in the AFS books do hit common equity. The held-to-maturity losses aren’t recognized because the banks plan to hold the bonds until they are paid off.

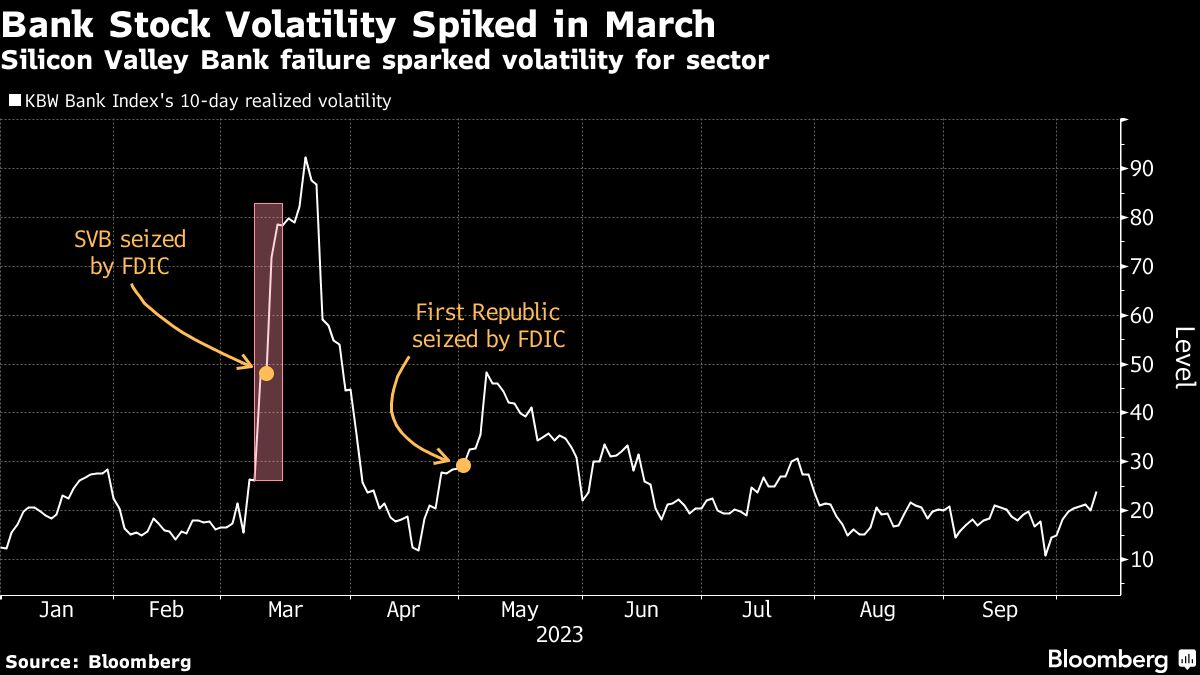

The recent surge in yields — which abated somewhat this week — has renewed investor focus on unrealized losses, a key issue during the turmoil that struck regional banks from March. Paper losses at banks that bet rates would remain low spooked depositors, triggering a series of fatal bank runs. While things have largely stabilized since then, investors have remained wary of the sector and have punished banks with long-dated portfolios.

Bank of America Corp. shares have fared the worst among the six largest US banks, down about 18% since the start of the year. The firm’s securities portfolio is bigger than its rivals and yielding less, potentially contributing to that lag.

It’s not just the specter of unrealized losses weighing on the sector. Since the tumult began, bank stocks have been pressured by regulatory proposals, higher deposit costs and the potential for worsening credit. Still, even as the stocks grind lower, the KBW Bank Index’s volatility is nowhere near levels last seen in March.

The group of banks staged a short-lived bounce in the middle of the year as the crisis receded, but failed to hold on to those gains. They’ve since retreated to near their May lows as rates march higher. Regional firms have been some of the hardest-hit within the sector, with KeyCorp and Comerica Inc. each down nearly 40% this year.

The conversation around bank stocks has shifted from the prospect of net interest income and net interest margin coming off their lows to “fears about securities marks and the handful of one-off credit events disclosed over the past few weeks,” Piper Sandler & Co. analysts led by R. Scott Siefers wrote in a note last week.

“‘Higher for longer’ and broader recession fears certainly don’t seem to be doing us any favors, either.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Max Reyes, Bre Bradham