Bond yields are sending an economic warning as this past week 10-year Treasury yields dropped back to 1.3%.

Following the June Federal Open Market Committee (FOMC) meeting, the Treasury curve flattened as the market reacted to a more aggressive hiking schedule than previously expected. Risk continued to perform well as investment grade (IG) corporates outperformed again and tightened through levels not seen since 2018. Economic data continues to improve showing the reopening remains on track, but investors remain focused on elevated levels of inflation.

Gold notched its third straight week of higher prices as the yield on the 10-year Treasury dipped below 1.3% for the first time since February. The highly transmissible Delta variant was also ruled the most dominant strain of coronavirus in the U.S., threatening economic growth and raising uncertainty about the next interest rate hike.

TINA has been applied to investing. You must buy stocks because TINA. You can’t make money any other way. Just close your eyes, buy and hold forever. Or at least through a full market cycle. Frankly, I think that’s stupid.

In the last few weeks, stock market leadership reversed back to lockdown-era defensives as the stock market made new all-time highs.

Investors are backtracking on reflation bets, with the bond rally extending as central banks signal continued support and stocks falling as Covid-19 variants threatened reopening prospects.

The pristine surface of a lake on a perfectly calm and sunny day is easy on the eyes. Yet it usually offers no insight as to what lies beneath.

With so much focus being placed on the inflation versus deflation debate of late and many financial pundits declaring a new inflation paradigm is upon us, what better a time to argue the case for deflation.

The reflation trade that hammered bonds, drove stock gauges to repeated records and re-energized long dormant value shares this year is in rapid retreat.

For international investors, we believe the United Kingdom is home to many companies that offer an especially attractive combination of growth, value and quality.

As the world convalesced from the pandemic, stocks advanced in the second quarter and earnings rebounded across sectors.

In Part-2 of “Capitalism” does not equal “Corporatism,” we delve into why bailouts support corporatism and how to fix the system.

As stocks around the world continue to smash one record after another, some of the world’s biggest money managers have a simple message: Get used to it.

Bond investors are worried, and who can blame them?

The ever-important payroll report came in ahead of expectations for June, but will ultimately do little to sway policy in toward the hawkish faction of the Federal Reserve Board.

Raymond James Chief Investment Officer Larry Adam examines the current investing environment through the lens of classic games.

Ken Leech, Chief Investment Officer at Western Asset takes a dive into his outlook for various segments of the fixed income markets in the second half of 2021.

Over the past few months, we’ve heard plenty about the rotation to value putting pressure on growth stocks.

Legendary global investor John Templeton once said that the best time to buy was when there was “maximum pessimism,” and the best time to sell was when there was “maximum optimism.”

There is always a lot of controversy around the implications of high and rising government debt. Over the past 70 years, rising government debt has generally been accompanied by weaker economic activity.

We have been long-term owners of Amgen (AMGN), Merck (MRK) and Pfizer (PFE) among the major pharma/biotech companies

The global economic reopening remains on track as COVID-19 vaccination rates climb.

Brexit and the pandemic didn’t change the fundamental attractiveness of great U.K. companies.

Claiming Social Security too early is economically equivalent to delaying claiming, withdrawing $100,000 from a portfolio, and setting it on fire.

If we could travel back in time to the beginning of 2020, many of us would be surprised at how good things were.

A couple of weeks ago, in “Warning Signs A Correction Is Ahead,” we said quite a few indicators set the stage for a pick-up in volatility.

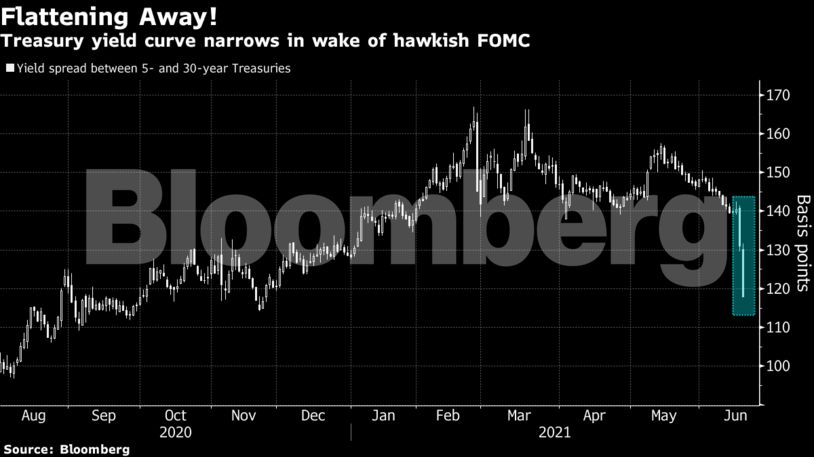

Last week the 10-year to 2-year US Treasury yield curve spread narrowed from 133bps to 119bps in just three trading days.

Bitcoin erased its 2021 gains this week as China ramped up its crackdown on mining of the cryptocurrency, a move that’s expected to help shift the industry’s center of gravity from Asia to North America.

Inflation continues to be a concern these days, and many investors are looking for investments that can keep pace with, or hopefully beat, the rate of inflation

Growth stocks have lagged cyclicals so far in 2021, but we remain steadfast in our belief that secular growth is the key to generating long-term returns. In this piece, we discuss how we find attractive opportunities in the small cap universe.

The Fed meeting last week led to higher asset price volatility across asset classes.

Over the past few months, economic recoveries have been uneven across regions and sectors.

Sir John Templeton famously said that “this time is different” are the four most dangerous words for investors.

The GMO Asset Allocation Team has released its latest 7-Year Asset Class Forecasts through May 2021 (click to view online or see chart below).

Hedge funds couldn’t have picked a worse time to be short the dollar while holding Treasury curve steepener positions.

Through the first half of 2021, fixed-income investors have been faced with their greatest fear: inflation.

The Fed now acknowledges inflation risks are to the upside.

Domestic business travel is well on its way to recovery. Forty percent of poll respondents said that business travel within the country where their firm is based has already resumed, while a third said that their company has either decided on a start date or is working toward a date.

The Fed made no changes to its interest rate or balance sheet policies; but some of the language in its statement was tweaked, reflecting recent hotter inflation data.

As Europe’s economy continues to recover from COVID-19, it appears the central bank will remain accommodative, but for how long?

This week’s aggressive repricing in U.S. Treasuries is going global, with long-end borrowing costs from Germany to the U.K. sliding as traders brace for central banks to quell fears over rising inflation.

“We are a long way from 1970s-style inflation,” Scott Minerd said. The data does not support the view that inflation is non-transitory, he said, despite what some people, including hedge fund manager Paul Tudor Jones, are claiming.

Chief Economist Scott Brown discusses current economic conditions.

Paul Tudor Jones is super bullish on Bitcoin right now and may give the crypto the same 5% weighting as gold, commodities and cash.

The Rorschach inkblot test was created in 1921 to analyze how individuals who view the exact same picture perceive and interpret external reality.

More and more, investors are wondering whether the Federal Reserve will tweak its monetary policy toolkit to help out money markets that are starting to drown in a sea of cash.

Coherent thinking is interested in how things are related; where they come from, where they go, and the mechanisms by which they affect each other.

Over the last couple of months, the Fed started its campaign to prepare markets for a “taper” of its asset purchases.

Federal Reserve Chairman Jerome Powell and his colleagues appear to be winning over investors with the argument that the current surge in consumer prices won’t last.

With investors anxious to hear the Federal Reserve’s latest take on inflation after last week’s hot reading, certain corners of the market are already simmering down.