The Case For Deflation

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWith so much focus being placed on the inflation versus deflation debate of late and many financial pundits declaring a new inflation paradigm is upon us, what better a time to argue the case for deflation.

Back in March, I laid out the case for inflation in comprehensive fashion, now, as all good investors ought to do, I will present my case why the disinflationary and deflationary trends that have engulfed markets over the past 40 or so years may continue.

We all know the major deflationary forces of today; debt, demographics, globalization and technology. I will endeavor to address these throughout this article. However, there are also a number of lesser known deflationary forces that perhaps do not get as much attention as they deserve. These too I will endeavor to explain below, along with where we stand with the current inflationary pressures, transitory or not.

Debt

For listeners of Erik Townsend’s excellent MacroVoices podcast, you will be aware of Erik’s proclamations of how many of the best and brightest minds in finance and macro have shifted from the deflation to inflation camps; with Vincent Deluard, Russell Napier and Louis-Vincent Gave being some such examples. However, there does remain a few “deflationists” out there, the most prominent being Lacy Hunt, and it is from Lacy’s arguments for debt and economic growth driving deflation where I will begin.

The chief problem facing most of the worlds developed economies today is the level of outstanding debt, both private and public. Whilst the creation of debt can represent an expansion in the broad money supply, the destruction of debt conversely equates to a contraction in the money supply. As all debts must eventually be repaid, debt by nature is deflationary over time.

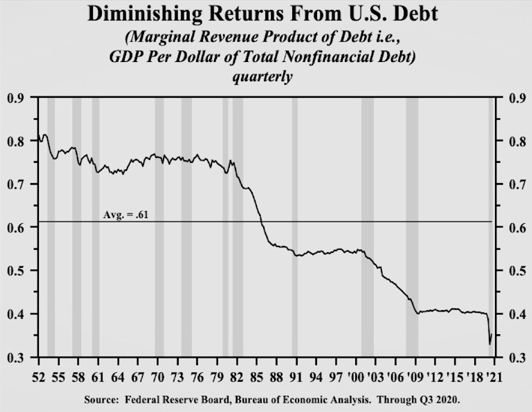

This is not so much a problem if the marginal return on debt exceeds the cost of debt. We have however long past that point whereby the creation of new debt lead to a greater increase in productivity. The marginal productivity of debt, or simply the return on debt, is at its lowest levels in over 70 years. As the below chart illustrates, we are now at the point whereby each new dollar of debt created is only able to increase GDP by less than 40 cents.

Source: Hoisington Investment Management

An increase in debt is an increase in current spending at the expense of future spending unless the income generated on the debt is sufficient to repay principal and interest. Stimulus hardly meets this criteria. Additionally, given central bankers and policy makers have never allowed the over indebtedness to resolve itself (rightfully or wrongfully) via the process of austerity and creative destruction, what has resulted is the dynamic of this ever falling return on debt being subjugated by the creation of even more debt in a negatively convex manner.

As much as the “MMTers” will argue this is solvable, what we know for sure is this has never worked in history. Folk love to harken how the tale of Japan will not be the fate of the US and how Japan was different (to which Lyn Alden has previously presented an excellent case for, and one in which I largely agree), though we are yet to see any evidence the United States’ spiral down this deflationary debt dynamic is actually different.

This is the greatest flaw in the argument fiscal dominance and MMT will create growth and inflation: we are searching for an easy solution to economic growth, one that has never worked in history. Yes, fiscal dominance may be the catalyst for inflation, but the debt overhang simply does not allow this to be accompanied by sustained growth. Instead, at best we may see stagflation accompanied by financial repression, as I discussed in my previous musing on inflation.

Debt & Money Velocity

To get inflation, we need a pickup in the velocity of money. Money velocity is largely a function of the level of debt relative to GDP. In the chart below, you can see how the year-over-year change in the velocity of money (red line, inverted) has a significant inverse relationship with government debt/GDP (blue line).

As debt is a constraint on money velocity, for velocity to increase, the economic growth needs to exceed the growth in debt, meaning the debt must be put to productive uses such that it spurs growth greater than its cost. A bet on inflation is a bet on an increase in the velocity of money, which is a bet on the increase in the marginal productivity of debt.

So long as the MMT-style stimulus is debt financed, this dynamic will struggle to reverse. As a result, the historic increases in money supply could be somewhat irrelevant unless the velocity of money increases. You simply cannot look at the growth in money supply without also looking at the velocity of money. Debt financed stimulus ultimately leads to the same conclusion; more debt and less growth. History tells us this has never been more than a temporary solution.

In the long-run, debt is simply a constraint on aggregate demand, and, for prices to rise demand must exceed supply. Whilst certainly possible, unless we go through a period of creative destruction and austerity (unlikely), the debt constraints on the US economy create a significant headwind for sustained inflation moving forward.

Demographics

Demographics remain one of the most powerful drivers of long-term economic growth. I have written extensively on the topic of demographics in the past, as it is a force whose impact on all facets of economics should not be underestimated or overlooked.

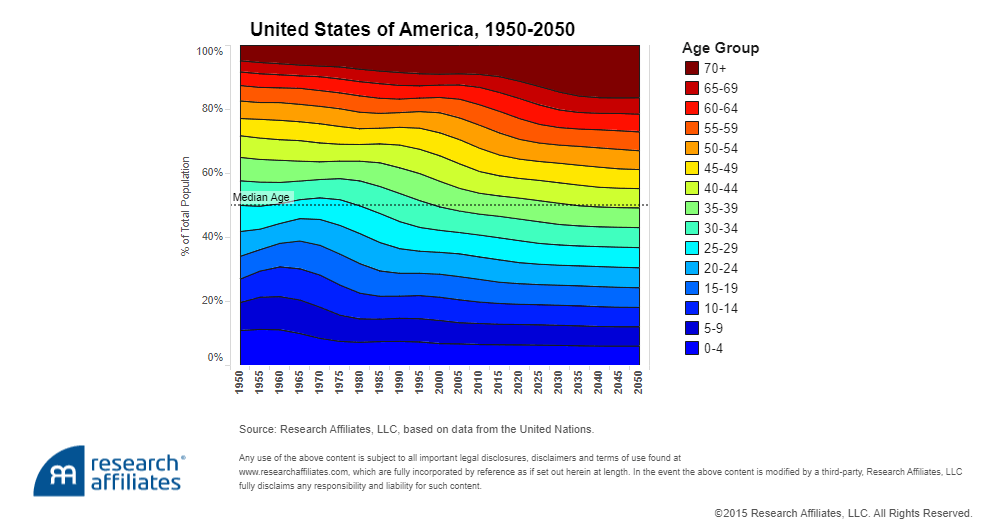

The developed world has a demographics problem that is not going away. The largest generation in history is retiring and as a result the number of retirees relative to workers is rising and is likely to continue to do so over the coming decades. Empirical evidence shows productivity, consumption and economic output peaks for workers roughly in their 20s-50s. Conversely, the contribution to GDP growth for the average worker falls negative as people enter their mid-to-late 50s and thus are no longer a contributor to economic growth.

The below chart from the work of Research Affiliates illustrates this relationship between age and economic output.

A falling support ratio (working age population relative to children and retirees) for countries with an aging population is a powerful constraint on economic growth. This makes sense, as consumption (being the largest input for GDP) is largely based on age. The older we get, the less we consume and contribute to the economy. This dynamic is a deflationary force over the long-term.

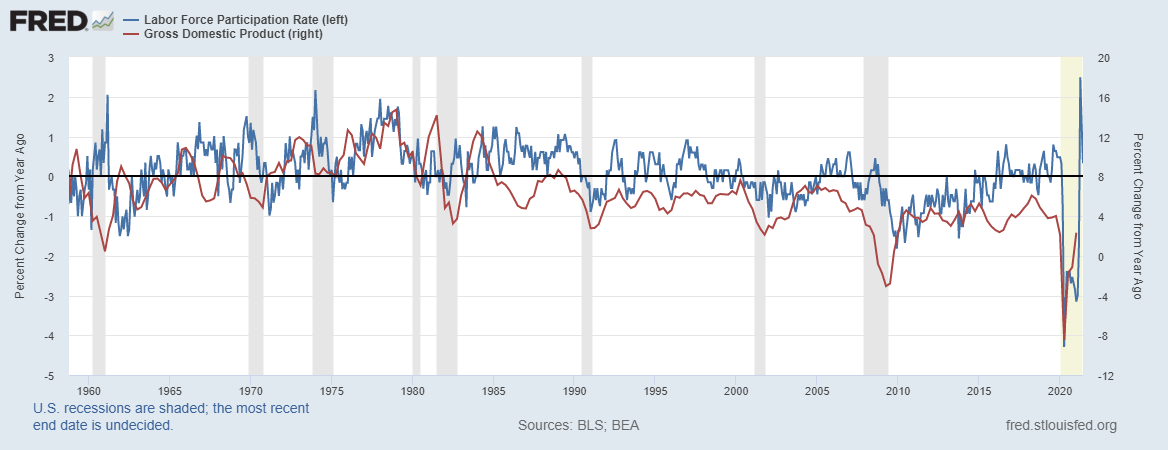

As we can see below, the labor force in the US has long since peaked.

The relationship between the labor force and economic growth is better comprehended when comparing the two in rate-of-change terms.

Clearly, we can see above how the two are related. Whilst there has been a significant jump in the labor force compared to 12 months ago, it is important to consider the base effects of year-over-year data. This time last year, the worlds economies were on stand-still. On an absolute basis, we remain near the lowest level of labor force participation in about 40 years.

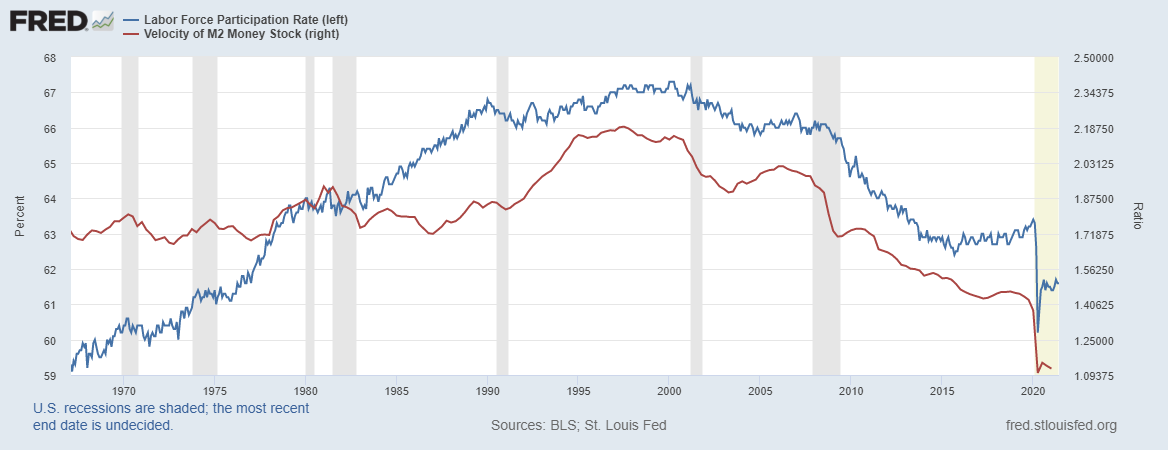

What’s more, similar to how debt is a constraint on the velocity of money, so too is the labor force participation rate.

The labor force is highly correlated to the velocity of money. To get a pick-up in velocity, what is really needed is a growth in the level of the population who are more willing to spend and consume, which, as we know from the previous chart comparing age groups and growth in GDP, is an increase in those aged between 20 and 50.

However, as we look forward, we can see the level of retirees relative to those working (support ratio) is only going to continue its downward trend for at least the next decade or two as the average age of the population increases. There is a stark contrast between the median age of today relative to that of the structural inflationary 1970s and 1980s.

The immediate future will continue to see more people leaving the economy and retiring compared to those entering the economy. The demographic headwinds facing not just the US, but most of the developed economies worldwide undoubtedly continues to provide a significant headwind to any form of sustained inflation.

Other Deflationary Forces

Whilst debt and demographics have been two of the most significant deflationary forces at play, along with technology and globalization, there remain a number of lesser known but meaningful dynamics working to reinforce deflation.

Technology & Productivity

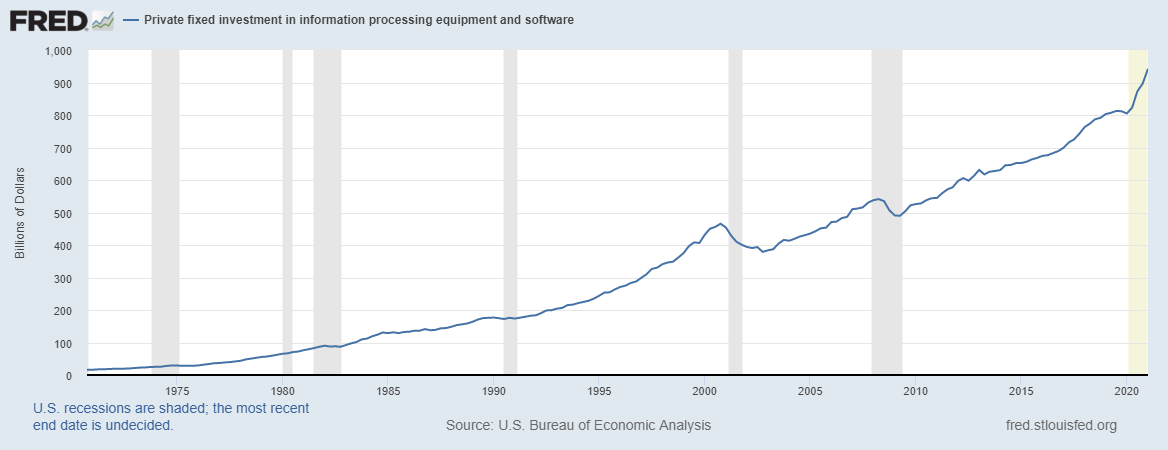

Technological advancement and increasing productivity are inherently deflationary. Technology creates efficiency, which increases productivity which reduce costs. Technological innovation is not a trend that will plateau or reverse, technology is exponential.

The trend of investment in information technology hardware and software continues to rise.

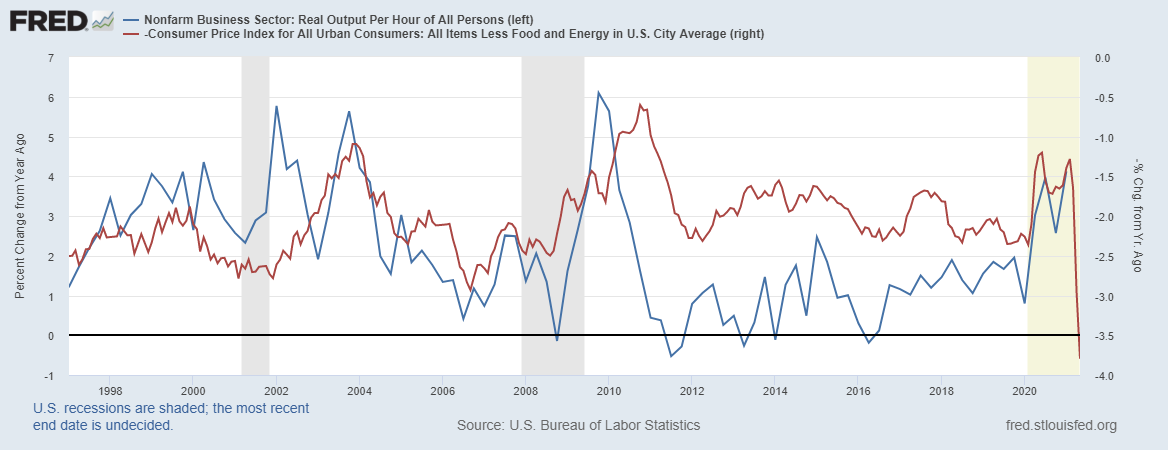

Likewise, productivity on a year over year basis is at its highest point in a decade. Growth in productivity is an inflation killer (core-CPI inverted below).

Technology will only further allow for the transformation of labor to capital through automation and efficiency. Going forward, the continued shift to a digitalized economy and growth in decentralized finance should only exacerbate this trend. Technology is an inflationary headwind unlikely to subside any time soon.

Money Creation, Quantitative Easing, Banking Lending & Interest Rates

There are two ways broad money supply is created; commercial banking lending and directly monetized government spending. I discussed the dynamics of money creation within my article on inflation in detail, and have again detailed this process as follows.

Historically, it has been the commercial banks that have been able to claim sole responsibility for the growth in the broad money supply. The notion that quantitative easing (QE) conducted by itself is money creation is false. The Federal Reserve and other central banks have the ability to influence the base money supply (M0), but not the broad money supply (M2). They can lend, but they cannot spend. Commercial banks create money via fractional reserve banking when lending occurs between said banks and consumers and businesses. QE is a means of capitalizing the banks, allowing them further scope to be able to lend against these freshly printed reserves with the central banks, whilst also pushing down interest rates in the hope this will spur an increase in lending. QE is effectively just a swap of government bonds for central bank reserves; unless lent against the two are negligible. Getting banks to lend is what increases the broad money supply.

Unlike the Fed, the Federal government does have the power to spend. If the central banks and governments work together, they are able to rapidly increase the base money supply and the broad money supply. If the central banks are directly funding government spending and outright guaranteeing loans made by banks, then this is money creation and has no doubt played a role in the expansion of the broad money supply we have seen of late.

Indeed, the shift of using monetary policy in isolation to monetary stimulus combined with fiscal stimulus will likely lead to a continued increase in the broad money supply. However, the misunderstood aspect of this dynamic is that ultra low interest rates and QE are in fact more likely to be deflationary, not inflationary. What’s more, whilst the government is spending central bank financed money, the traditional means of broad money creation in the form of commercial bank lending is still non-existent.

Focusing in on QE and interest rates, the primary goal of quantitative easing has been to lower interest rates to spur lending, create economic growth, increase asset prices and create a wealth effect. QE has succeeded in only two of these aspects; increasing asset prices and lowering interest rates. It is no secret QE has been by and large a failure.

The first problem associated with QE is suppressing interest rates to artificially low levels. Artificially low interest rates are not stimulative. In fact, there is evidence to suggest artificially low interest rates are only stimulative to a certain level, once they reach the ultra-low levels of today, these positive effects disappear to the point whereby they could be argued as being entirely deflationary. The below chart illustrates this dynamic well.

Source: Visual Capitalist

By artificially suppressing interest rates, this works to reduce the interest costs associated with existing debt. Reducing interest costs allow debtors more flexibility to repay the associated principal in addition to the interest payments, and, if these low interest rates are not spurring additional lending and creation of money to offset the repayment of principal, then this process is in fact the outright destruction of money. Likewise, those who live off fixed-income interest payments receive less interest, which leads to less income and thus less consumption.

To solve this problem, banks need to lend. The problem here is demand for credit is still largely contracting. Outside of fiscal stimulus, there is little growth in the broad money supply from commercial bank lending.

Despite ultra low interest rates, highly capitalized bank balance sheets and lending standards near decade lows, this lack of growth in consumer credit creates a headwind for continued structural inflation.

Broad money is created when consumers borrow and is destroyed when they repay principal. When you have interest rates artificially pinned near the zero-bound, money is destroyed as loans are repaid. It becomes unprofitable for banks to lend and as a result, there is less money moving around the system. This all leads to the suppression of money velocity.

Unless banks are willing or able to lend against the increase in their QE funded bank reserves, the liquidity provided by QE gets stuck inside the banking system. Ultra low interest rates and QE do not create money over the long-term unless they are accompanied by a commensurate increase in commercial bank lending, and a productive use of this debt. Whilst the direct financing of government spending is one avenue to solve this problem, the traditional means of fractional reserve banking needs to follow suit if sustained inflation is possible.

Wealth Concentration

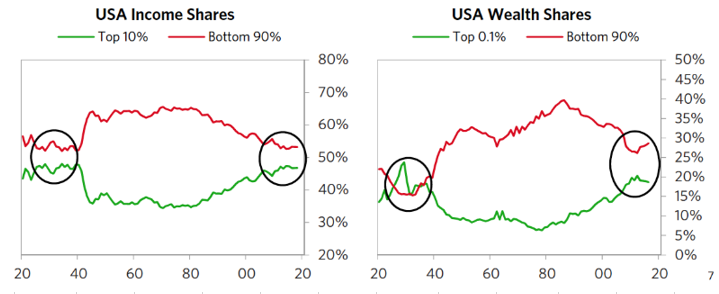

A deflationary force not commonly cited is wealth concentration. As is common knowledge these days, wealth concentration in the top percentiles currently stands at the largest discrepancy since World War 2.

Source: Ray Dalio, Bridgewater Associates

Put simply, those who have amassed more wealth have a far lower marginal propensity to consume. An additional dollar of income for those who are wealthy is far less likely to be spent on the consumption of goods and services than those who are less wealthy. This pushes down the velocity of money, reducing the flow of money throughout the economy.

Capitalism & Free Markets

Capitalism and free markets are not necessarily inherently deflationary. However, a capitalist regime promotes and encourages progress and innovation, which today primarily occurs through technological innovation. As I have discussed above, technology is inherently deflationary. Whilst markets may not necessary be “free” today, so long as we remain a capitalist economy for the most part the result will be continued innovation and progress.

Challenging The Inflation Narrative

Commodities & Supply Driven Inflation

Many people believe commodities and inflation are one and the same, this is simply not the case. Whilst commodity prices and inflation are certainly intertwined, using broad commodity prices as a measure of inflation is inaccurate. On the whole, the impact commodity prices has on core-CPI is less than you might think.

The US economy is largely a service economy, as the growth in globalization has resulted in the US offshoring its labor and supply chains. As such, strong movements in commodity prices generally will only have a small impact on core-CPI. We have had a number of commodity cycles over the past few decades, and as we can see below, the correlation between commodity prices and inflation is not significant.

Sustained inflation requires a permanent increase in demand relative to supply. Demand driven inflation occurs as a result an increase in demand that is unable to be met by a sustained increase in supply. For example, the 2002-2010 commodity bull market resulted from a sustained increase in demand led by China and the broad adoption of commodities as an asset class by institutional investors and pension funds. Likewise, during the inflationary 1970s and 1980s, the inflationary pressures were a function of an increase in demand as the largest generation in history, the baby-boomers, entered the workforce and significantly increased the labor force participation rate. I have discussed these demographic forces above. Today, we have a contracting labor force and an aging population, which will see a continued contraction in demand.

The commodity and price increases we are witnessing at present appear to be largely a result of supply side constraints, as opposed to a sustained increase in demand. The COVID-19 induced shutdowns interrupted supply chains and the transportation and availability of raw materials. Supply will come back to meet this demand for most commodities, if it hasn’t already.

Supply is almost always less elastic than demand. A result of inelastic supply constraints are short-term disruptions as aggregate supply cannot meet aggregate demand, pushing up prices and lowering corporate profits as less supply results in less revenue. Unless the price increases are demand driven and sustainable (like we saw in the 1970s/80s and 2000s), supply driven price increases are likely to be temporary. The solution to higher commodity prices is higher commodity prices.

However, it is worth noting there will be exceptions to this dynamic. I would argue copper and electrification metals will have a sustained increase in demand due to the electrification of the worlds economies. Longer-term inflationary pressures may indeed result from such trends.

Short-Term Inflation Expectations

Due to this belief held by many that commodities equal inflation, it is unsurprising to see that short-term inflation expectation measures are simply based off commodity prices, the most notable being the price of gasoline and oil.

The issue here is commodities may be more so driven by inflation expectations, or inflation expectations driven by commodities, than any actual increase in aggregate demand capable of sustaining inflation. Commodities are only a part of the inflation story.

Where Are We Now?

The June core-CPI reading of 3.8% is the highest year over year number in nearly 30 years. Whilst this is meaningful, it is important to consider how base effects exacerbate such data. During 2020, the economy basically shut down. Year-over-year economic data for 2021 must be taken with a grain of salt, especially considering core-CPI bottomed in the May to July period of 2020. The pandemic caused a global shock to the worlds economies. The fall in demand more than offset the fall in supply, creating the conditions of severe disinflation. Now, as the worlds economies are beginning to function closer to full capacity once more, this dynamic is working in reverse. Demand has roared back, spurred on by fiscal stimulus, whilst supply is yet to follow suit. As I have mentioned above, supply will eventually come back to meet demand. This will likely be sooner rather than later.

Indeed, when we look at longer-term inflation expectations, there is still a lack of any significant concerns of structural inflation. The Cleveland Fed’s 10-year inflation expectations measurement is not signaling any long-term inflation.

Meanwhile, the 10-year breakeven inflation rate and 5-year, 5-year forward inflation rate may be sitting at roughly five year highs respectively, but both remain well below the highs seen post GFC, and below the 2.5% mark. These long-term readings are not meaningfully high.

It’s not just the long-term inflation expectations sending us this message, but it appears as though the reflation trade and global growth may be nearing a peak. Chinese credit impulse, which measures the creation of new credit and has been an excellent leading indicator of global growth, has rolled over significantly these past months. China is the largest manufacturer in the world and is a key driver of the worlds business cycles.

Source: Julien Bittel

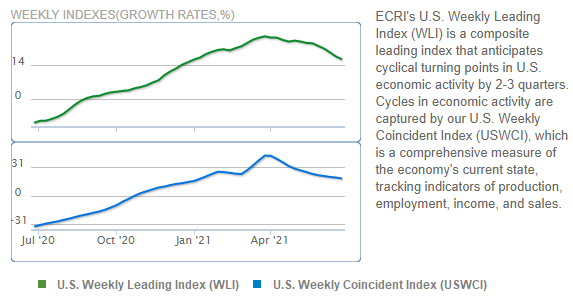

Likewise, the ECRI leading indicator appears to be confirming this message, the business cycle looks to be topping

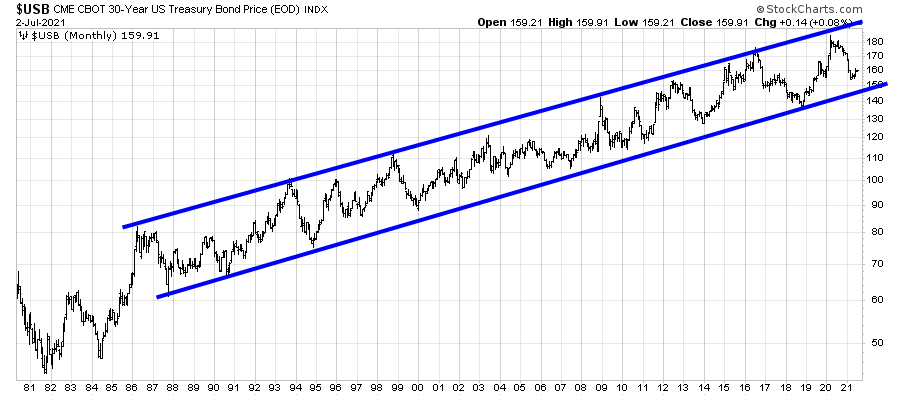

A slowdown in global growth looks to be the potential story for the second half of 2021. This is what the bond market has been telling us. Despite the continued inflationary pressures through the first half of 2021, long-term yields topped back in March and have been falling ever since. Whether or not the 30-year falls below 2% or holds the line will be telling.

In every recession over the past 50 years, we have seen a temporary spike in bond yields due to rising inflationary pressures. In almost every instance, the spike in yields were temporary and reversed to the downside as the natural deflationary forces once again took hold. Historical precedence tells us this time will likely not be different.

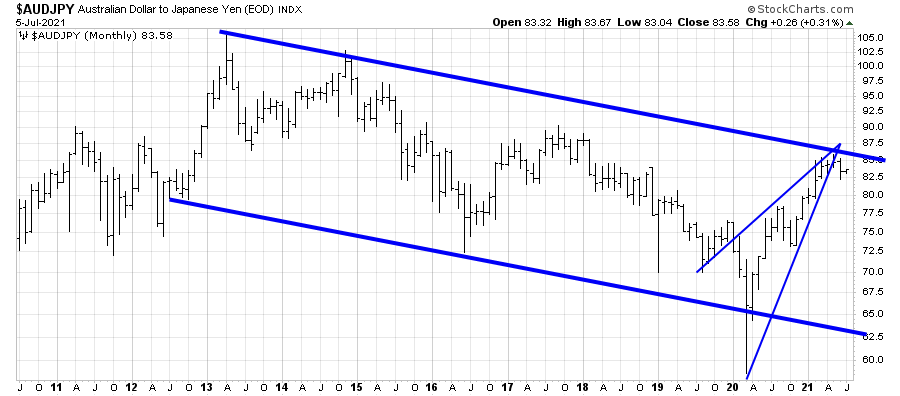

Looking at the reflation trade itself and using the AUD/JPY as a proxy, this looks a lot like a broken rising wedge pattern at the top of a long-term trading range. A continued pullback in the AUD/JPY would likely signal a further correction in the various reflation trades is imminent.

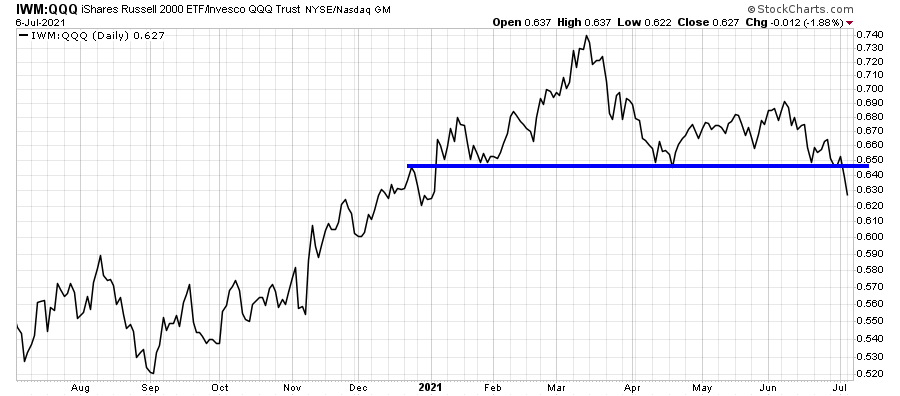

Likewise, if we look at tech relative to small-caps, the former appear to be reasserting their dominance.

However, as I detailed in my article arguing for inflation, there is potentially a path toward sustained inflation laid out in front of us. The move to MMT-style sustained central bank financed fiscal dominance, combined with labor onshoring and de-globalization are both inflationary tailwinds whose forces are only likely to grow over time. For now, despite fiscal stimulus putting money directly in the hands of those with a higher propensity to consume, much of this direct stimulus thus far have not been necessary contributing to economic growth. According to the New York Fed, roughly one-third of all stimulus payments received have been used to pay down debt, which as we know is the destruction of money, whilst only one-quarter is being spent on consumption, with the remainder being saved.

Source: Federal Reserve Bank of New York

Going forward, it is a matter of whether these forces are enough to overcome deflation, history suggests otherwise. However, should such measures as central bank digital currencies be introduced, or laws passed to allow the Fed the ability to spend, not just lend, both would certainly be game changers and would likely spur inflation.

Investment Implications

If it is true these deflationary forces will continue to suppress inflation over time, then for us investors it is important to consider how this might effect our investment decisions.

Unsurprisingly to most of you, the best performing asset classes and equity sectors over the long-term during a deflationary or disinflationary regime are those of a defensive, long-duration nature. Basically everything that has underperformed over the past 12 or so months.

Source: Incrementum

As boring as it is for investors, in a low growth world of little inflation, we are likely to see continued outperformance of the growth darling FAANG stocks on the whole, despite where valuations sit. We would likely see a continued bull market in bonds, as hard as that is to believe. Until the long-term trend for bonds tells us otherwise, the years ahead may just see more of the same.

Whether you reside in the deflation camp or the inflation camp, it is important investors assess both sides of the debate and come to their own conclusions. Whether we get inflation or deflation, investors should be prepared for either outcome. It may be we just end up somewhere in the middle.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All