The Fed meeting last week led to higher asset price volatility across asset classes. A handful of economic indicators suggests that the US economy may be on the verge of slowing down over the next quarters. If the US government does not approve the planned infrastructure package or increase welfare spending the Fed would likely soon revert to a dovish stance for a longer period. On the other hand, if the Biden Administration succeeds in keeping the economy running hot by passing the ambitious infrastructure investment programme and/or boosting welfare policies inflation could remain a problem. Either way, we believe the Dollar’s sharp move higher last week represents an opportunity for Emerging Markets (EM) local currency assets. Alongside progress on vaccinations across most EM countries, stronger GDP growth would allow EM local assets to outperform, even in an environment of higher nominal US interest rates. EM central bank policies have already turned more hawkish, which provides further carry support at a time when EM real interest rates are already higher than real rates in the US and other developed economies.

The Fed’s reaction function

The Fed’s reaction function as far as inflation is concerned has not changed, in our view. The Federal Open Market Committee (FOMC) deliberated about the possibility of reviewing its policy on bond purchases (‘talking about talking about tapering’), which suggests that tapering will likely be discussed in July or August, but the Fed may not necessarily announce a change in policy at those meetings. Hardly hawkish, in our view. The so-called dot-plot, which illustrates FOMC members’ rate hike expectations, posted a surprise as seven out of the sixteen members of the FOMC foresaw the need for a rate hike already in 2022 and most members now expect two hikes by 2023. Although this was not far from what the US Treasury market (UST) was already pricing in, the FOMC was not expected to signal rate increases so soon. In effect, the FOMC acknowledged that it was behind the curve in terms of its expectations about nominal GDP growth (both inflation and real GDP) and has now adjusted its position in recognition of the recent improvement in data. Still, in our view, the Fed is likely to remain focused on keeping real interest rates at extremely depressed levels for a long time by actively pursuing higher inflation. This should keep real rates very low and the Dollar (USD) on the back foot.1

Market reaction

The initial UST reaction following the FOMC was to push yields higher with 5-year and 10-year yields rising about 10bps to 0.90% and 1.59%, respectively, while the yield on the 30-year bond rose 5bps to 2.21%. Over the next two days, the curve bear flattened as 2-year yields kept on increasing to 0.25%, but the rest of the curve declined with 5-year, 10-year and 30-year bond yields closing the week at 0.87%, 1.44%, and 2.01%, respectively. The yield on the 10-year and 30-year bonds closed 1bp and 13bps lower than at the start of the week. Other markets also moved. Commodity prices declined 3.0% with lumber prices down 15.2%, copper prices 8.5% lower, soy beans down -7.5%, gold off by 6.0%, and iron ore prices 5.5% lower. Equities also sold off as the S&P 500 closed the week down 1.9%, while the S&P 500 materials and financials components were down more than 6.0%, and energy and industrials were down 5.2% and -3.8%, respectively.

These moves may betray a sense of vulnerability about the US economy in the context of policy tightening. Notably, MSCI EM outperformed, declining 1.1% overall with MSCI Latin America up 1.8%, while Asia and Europe declined 1.3% and 1.2%, respectively. The distinct flattening of the US yield curve was also due to positioning. A fund manager survey from Bank of America Merrill Lynch showed investors’ largest short positions were concentrated in UST bonds with long positions concentrated in commodities, materials, and banks, all of which were hurt post-FOMC. Hence, the Fed’s dot plot may have been a mere trigger to position squaring. The rise in yield at the front end of the curve drove the USD sharply higher, a move exaggerated by the unwinding of short Dollar positions. EUR declined 2% over the week as the broad dollar index rose 1.8%, while EM currencies declined 2.1% versus the Dollar. Positioning also influenced these sudden Dollar moves, in our view, which means they are likely to be short-lived. Further Dollar strength is not impossible, but the Greenback does not have enough wind in its sail to rise much more, in our view. The return to Dollar depreciation is just a matter of time, since the Fed remains committed to staying behind the curve in controlling inflation. This means that real interest rates are likely to remain negative for the foreseeable future. Market participants will look to the evolution of the US economy for clues as to the Fed’s next steps.

The state of the US economy

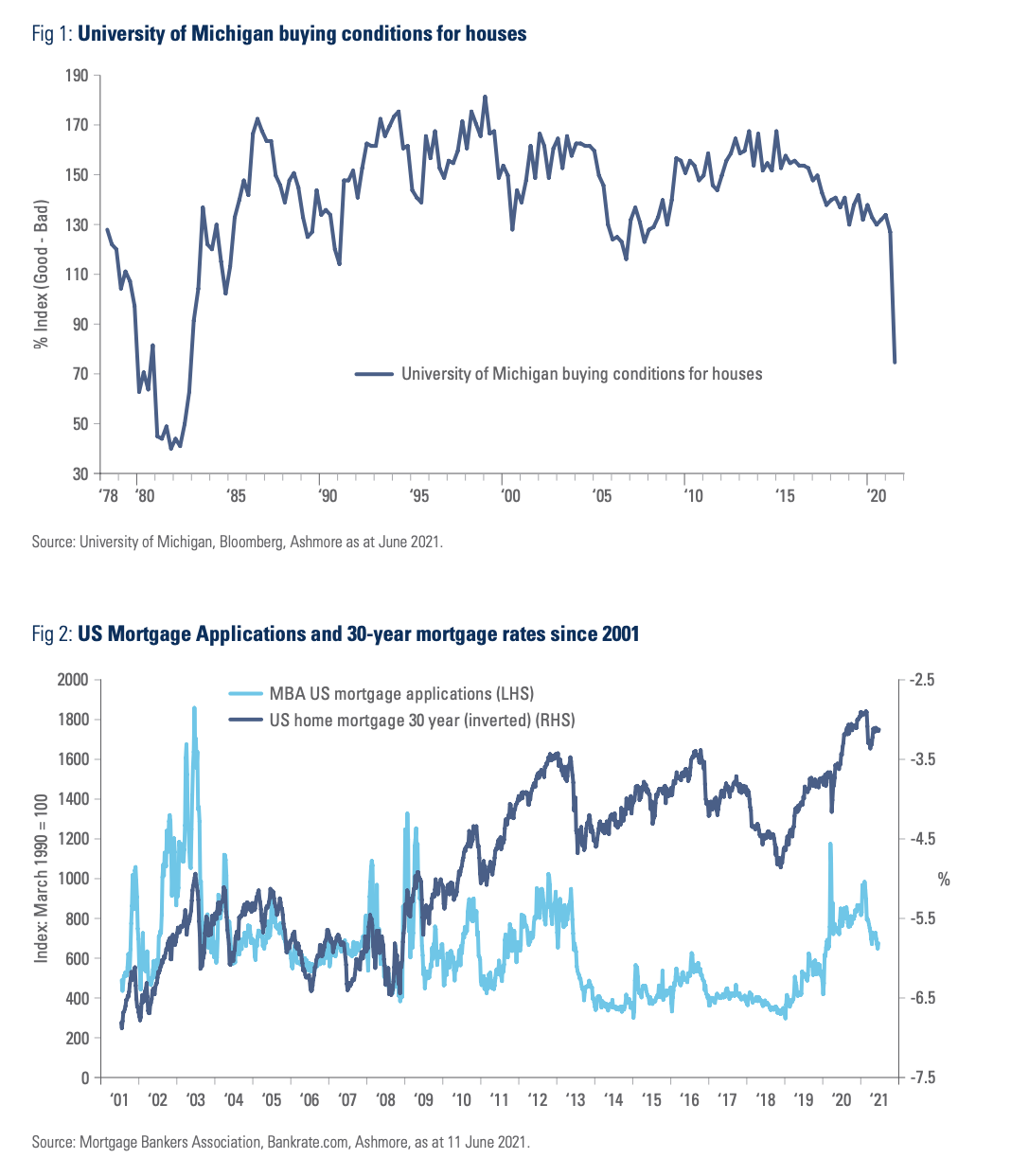

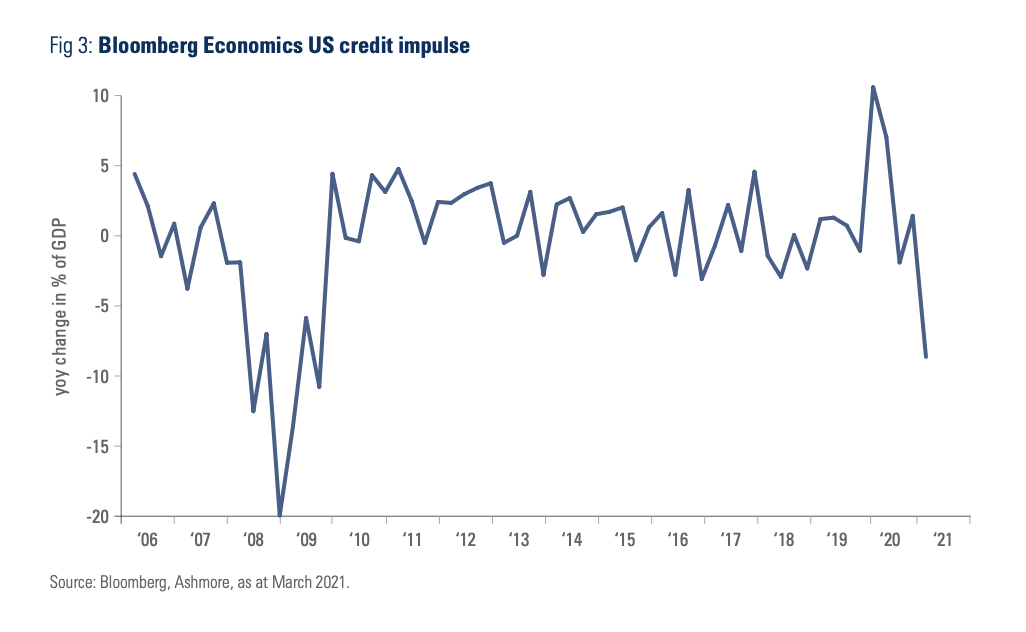

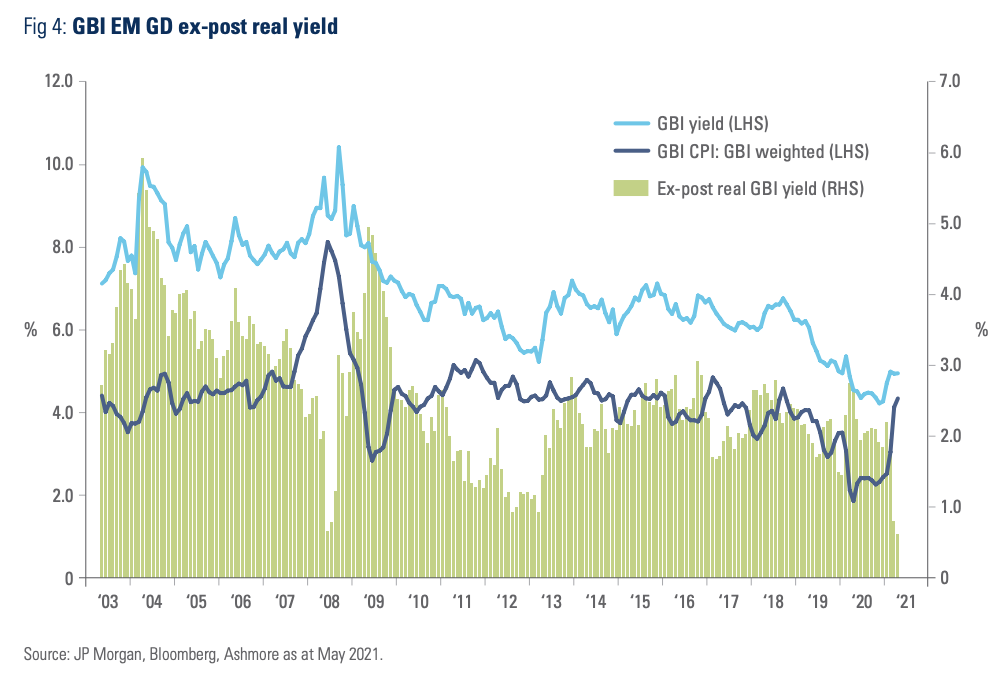

The central question for the second half of 2021 is whether current elevated levels of consumer and producer prices inflation will translate into higher wage inflation. The increase in inflation this year was unsurprising given (a) the Fed’s shift to average inflation targeting; (b) faster monetary and fiscal expansions; © the arrival of vaccines that allow economies to reopen; and, (d) pent-up demand for services and travel after 18-months of mobility restrictions.2 Large base effects relative to the depressed prices of many commodities last year around this time have also contributed to very high inflation rates in yoy terms this year. As the economy moves closer to full employment, wage inflation may become an issue. If wages increase in response to the rise in consumer and producer prices then the Fed faces a far more serious inflation problem. On the other hand, if wage inflation does not increase then the economy should soon start to slow again. In fact, consumer demand could be running into problems with the expiration of government pay checks in September, or even sooner as a result of the sharp recent increases in the prices of both assets (houses) and goods (consumer price inflation is running at a 5% yoy pace). Figure 1 shows the University of Michigan survey and illustrates that conditions for new buyers of houses are the worst since 1982. High house prices should be leading to exuberant consumption as house owner’s monetise their houses via mortgage borrowing to increase spending elsewhere. Alas, high saving rates and low marginal propensity to spend by existing asset-rich individuals are not leading to the usual wealth-positive effects from higher house prices. Figure 2 shows that mortgage applications are down 34% from the peak in January, in spite of extremely favourable interest rates. Other leading activity indicators such as smartphone shipments from Asia – a good indicator of household durable spending – are also in decline. Finally, as Figure 3 shows, the US credit impulse is at its weakest level since 2009. These indicators do not point to very strong economic activity in the post normalisation period ahead. Furthermore, the latest update of the New York Fed’s dynamic stochastic general equilibrium (DSGE) model shows that US real GDP growth is likely to slow sharply in 2022 and 2023.3,4 According to the model, real US GDP growth will be 2.6% in 2022 and 1.7% in 2023. These latest estimates are substantially lower than the 4.7% and 3.5% projections from March 2021. Real GDP growth for 2021 was increased to 5.4% (from 4.7% in March), but is much lower than the 6.6% market’s median consensus expectation.

Given the emerging mid-cycle symptoms discussed in the previous section, the continuation of strong economic growth and avoidance of disinflation next year is likely to require yet more fiscal policy stimulus, including a much discussed infrastructure investment plan as well as increases in welfare payments. Both will require either further large increases in debt or higher levels of taxation. Higher taxation and more investment would support the real economy and wages, if deployed thoughtfully in sectors that boost potential GDP growth. However, higher taxation and wages would most likely be negative for US equities. The outlook for the Biden Administration’s infrastructure plan is uncertain, as Democrats appear to require support from Republicans. While Democrats can approve their own version of the plan via the budget reconciliation process, there have so far been big difficulties in bringing conservative Democrats on board, including Representative Joe Manchin.

In our view, the Biden Administration is likely, eventually, to get a large part of the infrastructure plan through Congress, resulting in another large fiscal deficit in 2022. If that is the case then inflation fears could return after a period of consolidation in the coming months. The alternative scenario of no additional fiscal expansion would lead to a slowdown in the US economy, which would increase volatility in the short term and the Fed would be justified in keeping interest rates low for a longer period than suggested in the latest dot plot projections.

The EM opportunity

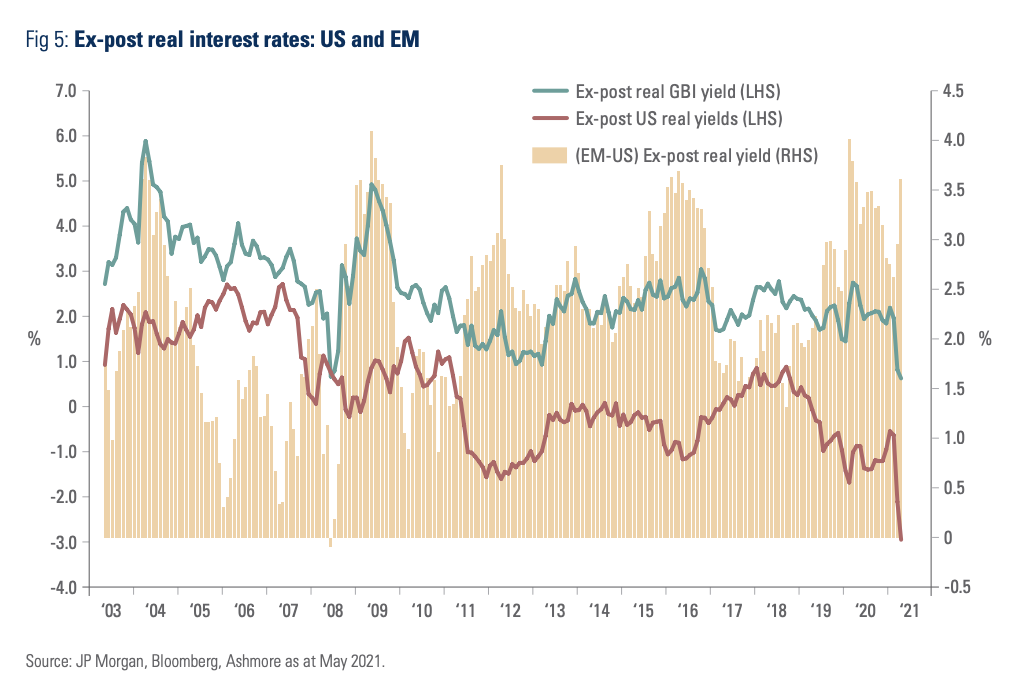

The sell-off in response to last week’s FOMC meeting presents a good opportunity for long-term investors to buy EM local currency assets. A number of EM central banks, including Brazil, Russia, Chile, Hungary, Poland, and the Czech Republic have turned hawkish, which is supportive for carry, boosting the attractiveness of holding local currency bonds. Higher policy rates also anchor inflation expectations, which is likely to boost the real interest rates in EM. Figure 4 shows that EM local currency bonds offer positive real interest rates. In absolute terms, the outright level of ex-post real yield in EM may seem small at first, at 0.6%, but the premium of EM real rates over US real rates is close to the widest levels in 20 years as shown in Figure 5. Furthermore, the real 2-year UST yield remains extremely depressed even after the hawkish tilt from the Fed. Currently, the real yield is close to -2.4% compared to -2.8% in mid-May.

Fundamentals are also likely to favour EM bonds. Economic growth in EM is likely to keep surprising to the upside thanks to the now fast pace of vaccinations.5 EM is on track to vaccinate about 2/3 of its adult population by year-end. The main laggards are in South East Asia, but Eastern Europe, China and now India are all accelerating. South America is on average two months behind the US vaccination levels and catching up. Faster vaccination is coinciding with better economic growth. The Organisation for Economic Co-operation and Development (OECD) revised its 2021 EM GDP year-end forecast 3% higher a few weeks ago. Brazil median GDP growth expectation was close to 3% in mid-April and today is closer to 5%. Hawkish EM central banks and fiscal conservatism also mean that inflation is likely soon to moderate in EM, pushing real rates even higher.

China, India and Latin America

China is in a good position to take advantage of the US economic situation. China did not need to adopt fiscal or monetary policy stimulus to the same magnitude in order to see its economy bounce as a strict focus on controlling Covid-19 allowed for their economy to reopen ahead of most countries. Instead of providing fiscal stimulus, China has been busy fighting excesses in housing, commodity and even the stock market (including regulating tech). The macro prudential focus explains why Chinese stocks have been lagging since Q4 2020, which is holding back EM equities. Now China has plenty of ammunition while the world is ‘bullet-less’. We expect them to ease both fiscal and monetary policy until the end of the year. Furthermore, China will end up vaccinating its adult population faster than the US and may be able to open up international travel before anyone else thanks to their state-of-the-art track and trace system.

India will accelerate their vaccinations as well and the economy is at the early stages of a cyclical recovery. Faster vaccinations will allow for a rebound in business confidence, which will grease the wheels of the monetary transmission channel, so the RBI stimulus can flow to the economy. Finally, the recent bouts of political noise in Latin America are receding. The presidential elections in Ecuador and Peru as well as the mid-term election in Mexico are behind us, thus removing a great deal of uncertainty in EM as a whole.

The combination of higher carry, better growth momentum, attractive valuations, and fewer uncertainties presents a favourable backdrop for EM assets, in our view.

No part of this article may be reproduced in any form, or referred to in any other publication, without the written permission of Ashmore Investment Management Limited © 2021.Important information: This document is issued by Ashmore Investment Management Limited (‘Ashmore’) which is authorised and regulated by the UK Financial Conduct Authority and which is also, registered under the U.S. Investment Advisors Act. The information and any opinions contained in this document have been compiled in good faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Save to the extent (if any) that exclusion of liability is prohibited by any applicable law or regulation, Ashmore and its respective officers, employees, representatives and agents expressly advise that they shall not be liable in any respect whatsoever for any loss or damage, whether direct, indirect, consequential or otherwise however arising (whether in negligence or otherwise) out of or in connection with the contents of or any omissions from this document. This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any Fund referred to in this document. The value of any investment in any such Fund may fall as well as rise and investors may not get back the amount originally invested. Past performance is not a reliable indicator of future results. All prospective investors must obtain a copy of the final Scheme Particulars or (if applicable) other offering document relating to the relevant Fund prior to making any decision to invest in any such Fund. This document does not constitute and may not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment in any such Fund. Funds are distributed in the United States by Ashmore Investment Management (US) Corporation, a registered broker-dealer and member of FINRA and SIPC.