Be wary of claims that indexing and passive investing have huge hidden costs. In my view, passive investing involves owning, as close as is economically feasible, every stock weighted to market capitalization. So this means total stock index funds.

A visit to the annual Bogleheads conference got Elm Wealth's Victor Haghani thinking about static vs. dynamic asset allocation.

Here are the key things advisors don’t always know about exchange funds.

Our profession is being transformed by powerful, AI-based technologies that will replace human-based financial advice. They will drive down costs, reduce valuations, and deflate the multiples paid in M&A transactions.

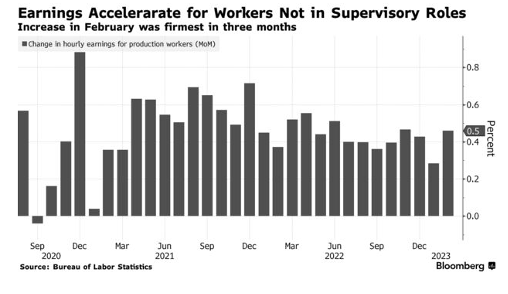

The conventional wisdom is that lower interest rates stimulate economic activity, and higher rates dampen it. But new research casts doubt on this hypothesis.

It has been my tradition to informally rate the investment-related books I read in the past year. Here is my list of winners and losers.

Great articles don’t always get the readership they deserve. We’ve posted the 10 most-widely read investment and planning articles for the past year here and the top practice management articles here. Below are another 10 that you might have missed, but I believe merit reading.

As is our custom, we conclude the year by reflecting on the 10 most-read investment and planning articles over the past 12 months. Tomorrow, we will highlight the 10 most-read practice management articles.

Trying to outperform the market by timing exits (just before the bear awakens from its hibernation) and entries (as the bull enters the arena) is a fool’s errand.

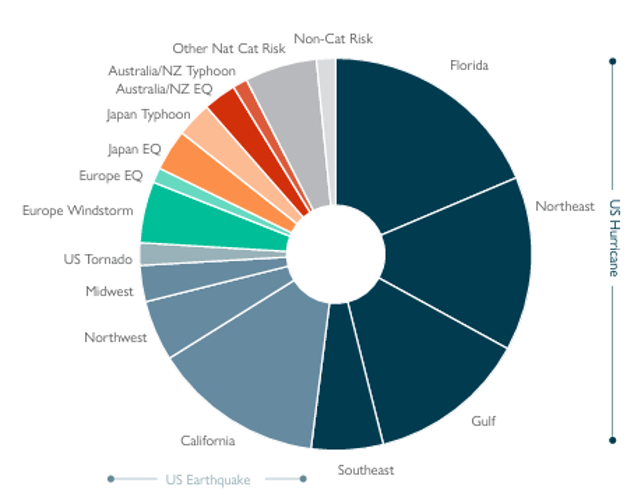

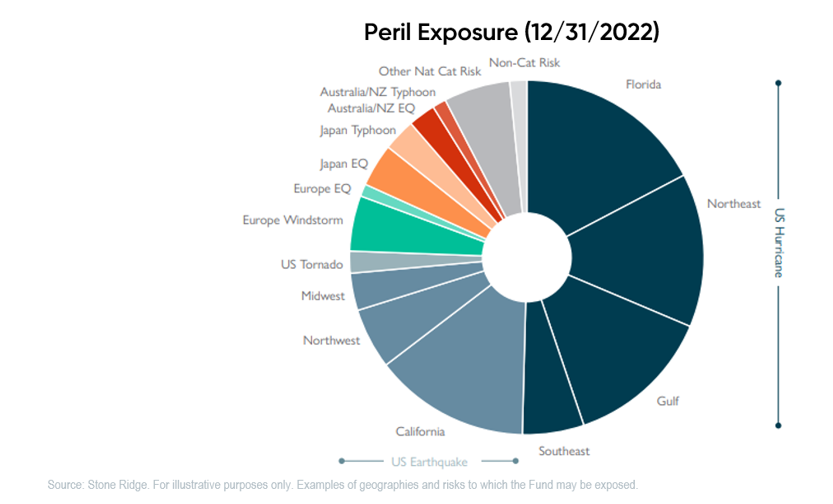

The Stone Ridge High Yield Reinsurance Fund (SHRIX) was introduced a decade ago to provide pure exposure to catastrophe-reinsurance risk that had historically delivered excess returns. Let’s look at how it performed over that period.

Recency bias is too ingrained within us as human beings to ever go away regardless of the evidence. As advisors, we must learn to manage it.

The AQR Style Premia Alternative Fund (QSPIX) was introduced a decade ago to provide pure exposure to four market factors that had historically delivered excess returns. Let’s look at how it performed over that period.

The growth of the federal deficit in the post-COVID era, coupled with the political unwillingness to increase taxes, foretells higher-than-historical inflation rates, according to new research.

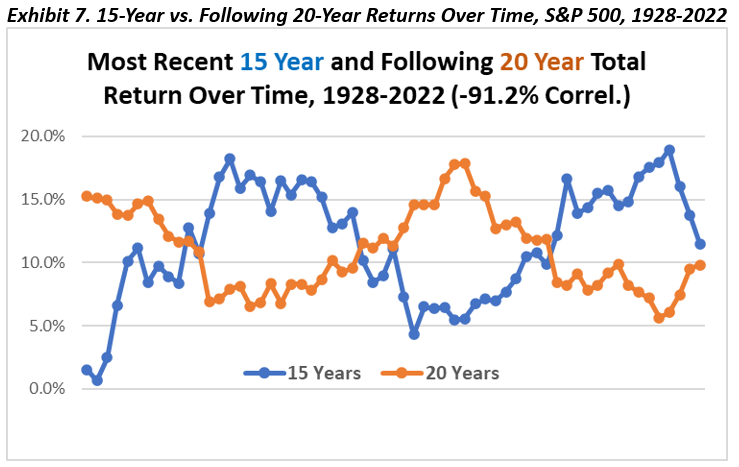

Investors should embrace a genuine long-term perspective, extending their time horizons to at least 20 to 30 years. The traditional notion of long-term investing (five to 10 years) may fall short of realizing the full benefits of long-term strategies.

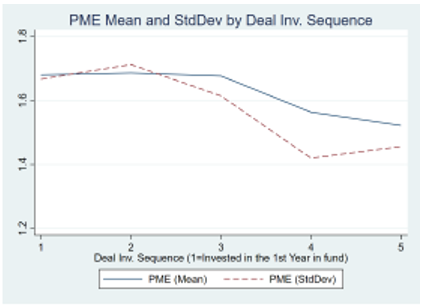

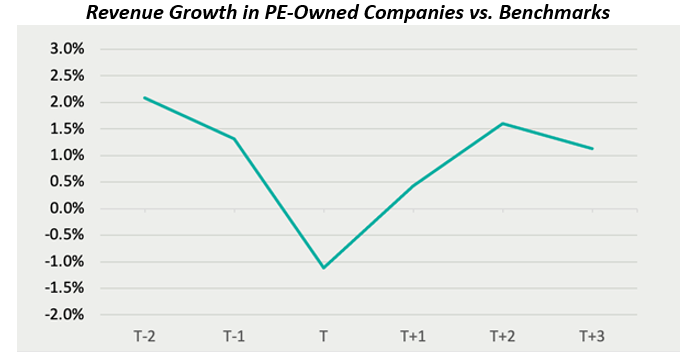

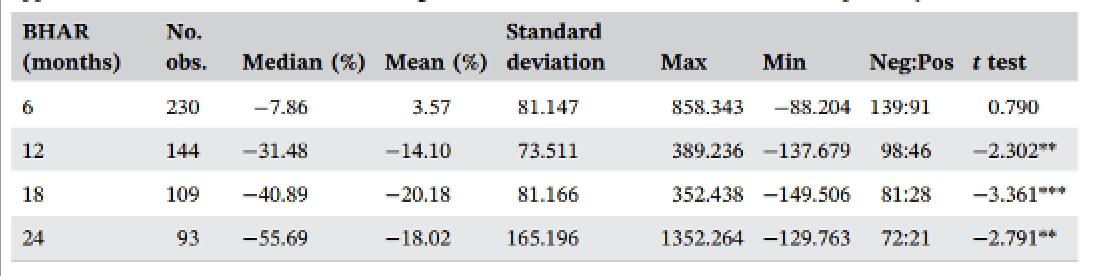

Private equity (PE) has become a staple of institutional portfolios, but its performance has often been disappointing. New research shows that the levels of specialization and portfolio diversification should be important considerations when selecting a manager to implement a PE strategy.

The so-called dividend aristocrats have an impressive track record. But much of that outperformance can be attributed to its exposure to certain factors.

New research found that the stocks of companies that have invested heavily – especially if that was not financed through organic growth – underperformed an appropriate benchmark.

Using a new database that isolates the activity of retail investors, new research documents their poor performance

New research shows that the tightening of bank lending standards – as is the case now – has led to stock-market underperformance. But with banks playing a smaller role in corporate finance, that finding has lost some relevance.

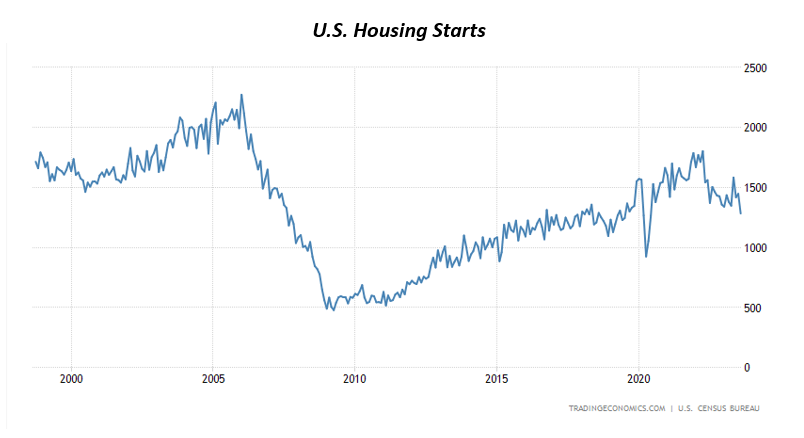

It is unlikely housing prices are set to crash unless there is an unexpected shock (a “black swan” event).

The yield on the benchmark 10-year Treasury is up 70 basis points this year, leading many to question the future direction of interest rates. Let’s look at the underlying causes of this and whether those conditions are likely to persist.

By applying artificial intelligence and Chat GPT to statements made by active fund managers, researchers have found that their underperformance can be partly explained by overconfidence that led to, among other things, excessive risk taking.

Warren Buffett has advised investors to be fearful when others are greedy and greedy only when others are fearful. New research confirms Buffett’s admonition.

New research shows that stocks have historically been a poor hedge against inflation over anything but very long horizons.

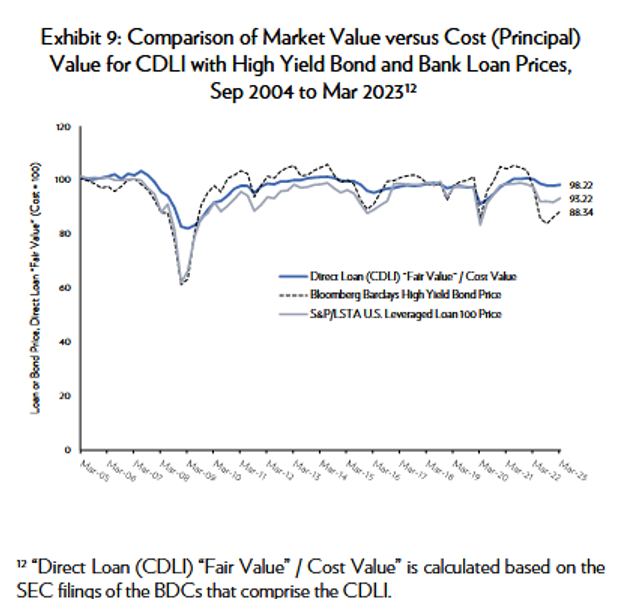

Investors seeking higher yields and relatively low risk, and are willing to sacrifice liquidity, will find attractive opportunities in interval funds that invest in senior-secured, sponsored middle-market loans.

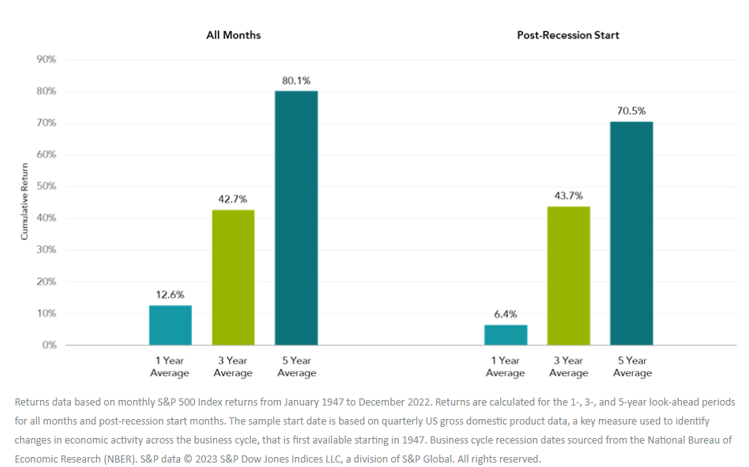

Like Samuel Beckett’s titular character Godot, we are still waiting the all-but-certain U.S. recession. It may yet happen, but it’s wise to understand why forecasters were so grossly incorrect.

The performance of PE funds has been disappointing. New research explains why this happened: Instead of driving operational efficiencies (as PE investors typically claim they do), those funds relied heavily on increasing the debt burden for the companies they bought.

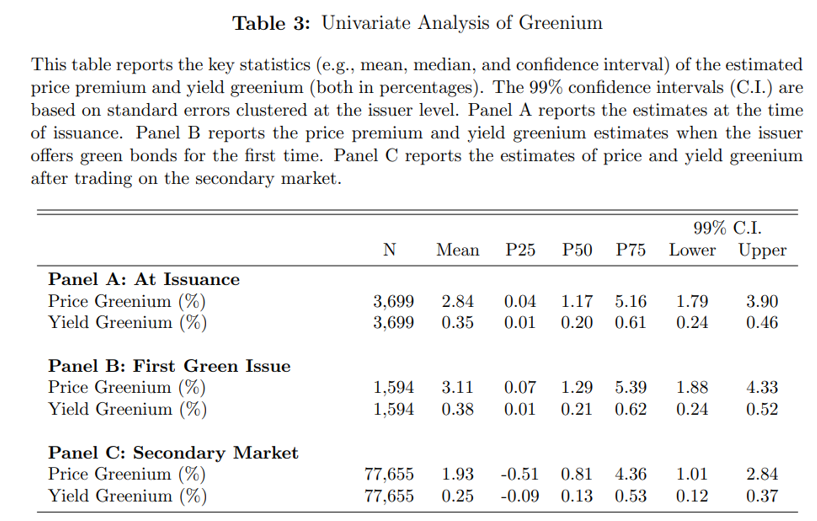

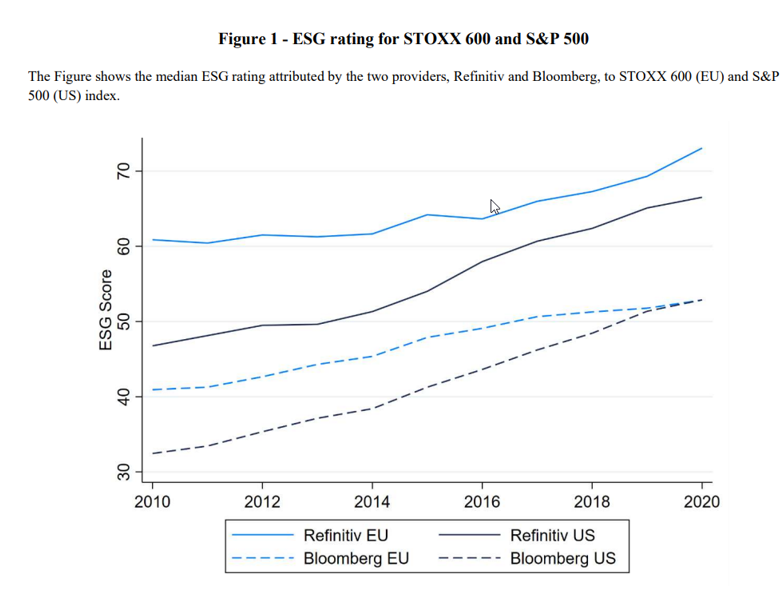

I’ve written previously about how positive (“green”) ESG metrics have increased the prices of stocks, reducing their expected returns. New research examines a similar effect in bonds, where a “greenium” (lower yield on green bonds versus non-green equivalents) reduces returns for investors.

Investors planning for retirement are facing seven significant challenges.

Starting valuations are the most reliable predictor of equity returns. But they are far from reliable, and investors must use those forecasts cautiously.

As we enter the hurricane season, there are signs of three financial calamities merging to form the perfect storm. The nexus is in commercial real estate, but it extends to banking and the broader economy.

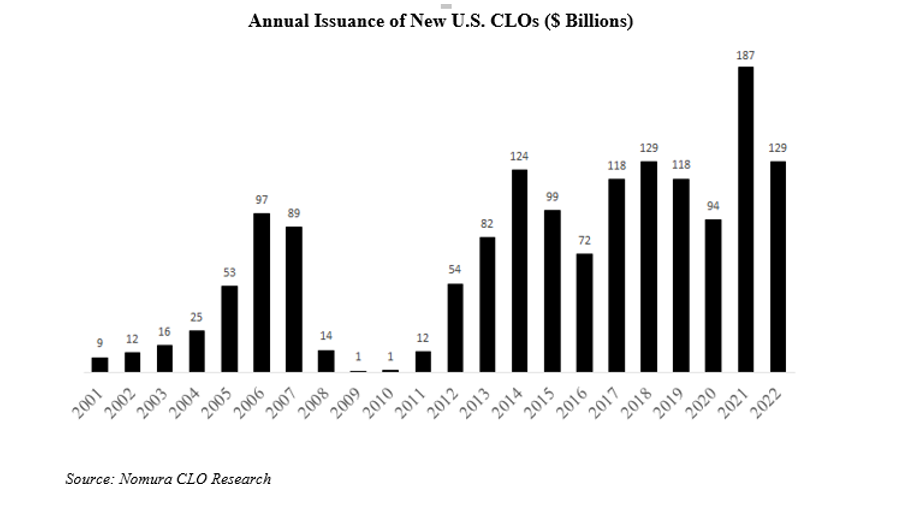

Investors willing and able to accept the illiquidity risk of CLOs should consider them as alternatives with attractive risk/reward characteristics.

New research has documented the persistent failure of investing based on artificial intelligence (AI). This is unsurprising, given the challenges of active management and the widespread inadequacy of humans to outperform an index fund.

New research shows that those who invest in stocks with positive environmental, social and governance (ESG) scores have improved the behavior of those companies.

Many economists have been forecasting a recession for 2023 due to tightening monetary policy. But that recession has not arrived yet.

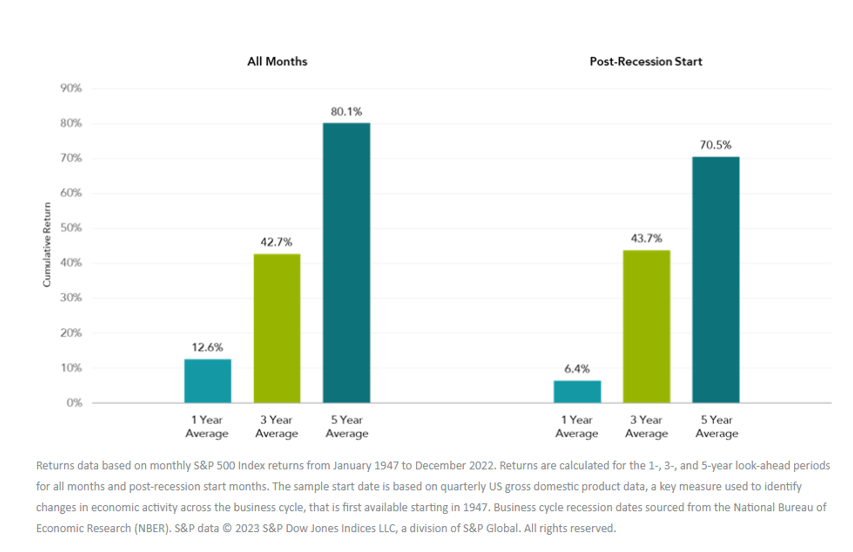

Ignore the “noise” of the market and adhere to your well-thought-out asset-allocation strategy that acknowledges both the virtual certainty of recessions and bear markets while also recognizing that trying to time the market based on economic forecasts is likely to prove counterproductive.

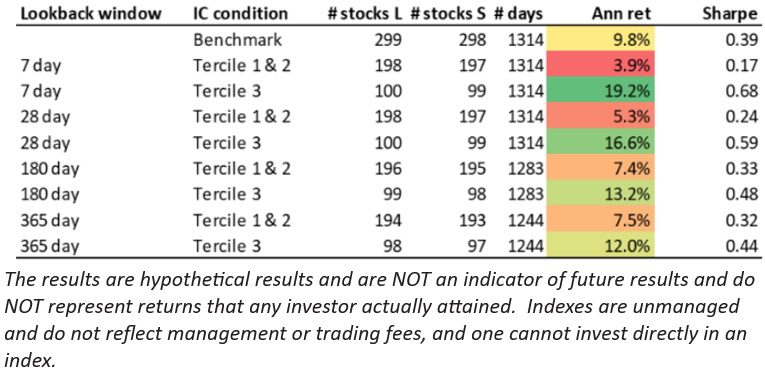

Short sellers are informed investors who play a valuable role in keeping market prices efficient – short selling leads to faster price discovery. Fund families that invest systematically have found ways to incorporate the research findings to improve returns.

I will analyze the pros and cons of three funds to access the reinsurance market.

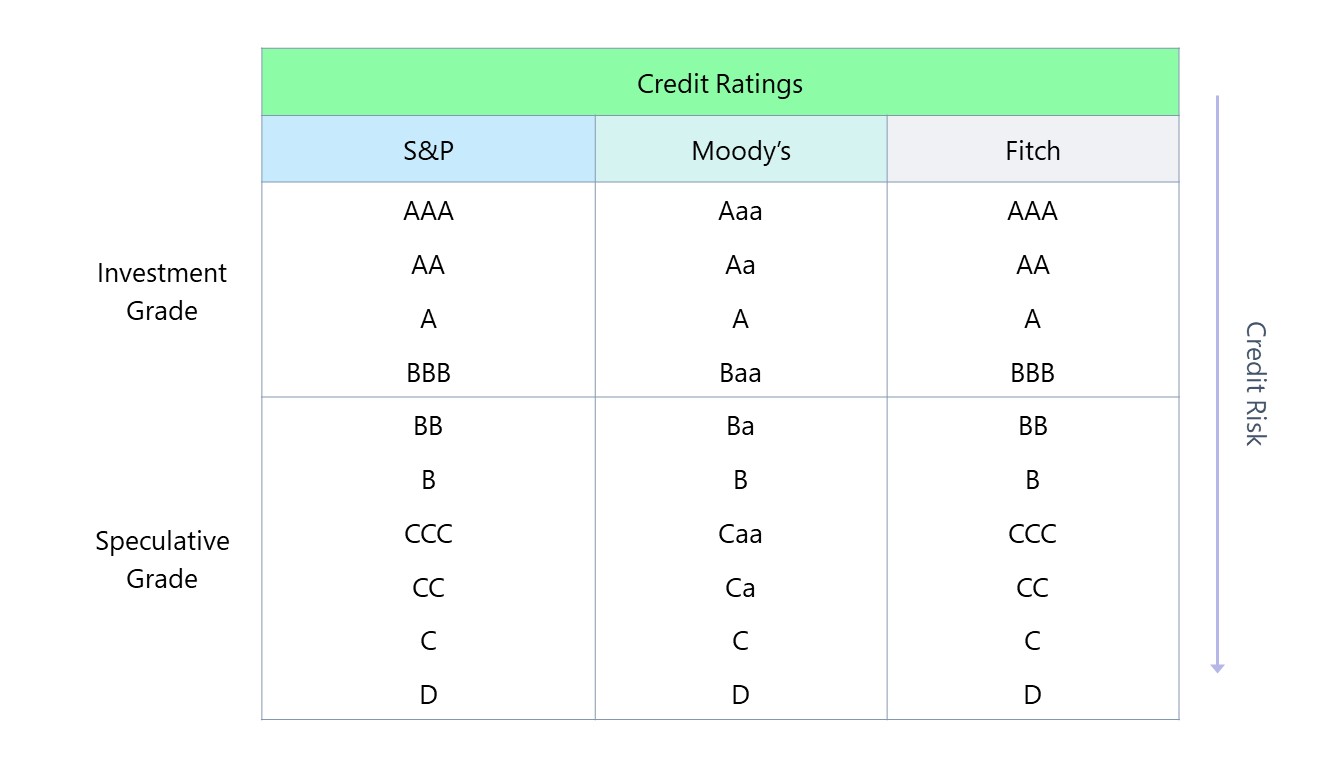

Investors should rely on the wisdom of crowds as expressed through bond yields, not credit rating agencies, to judge fixed-income credit risk.

Risk-averse investors seeking defensive systematic strategies to reduce left-tail risk should broaden their search beyond low volatility/low beta.

New research shows that investors can profit by exploiting “momentum” – the notion that stocks or factors that experienced good performance will continue to do so, and vice versa.

Research has shown that investing in IPOs has been a bad deal – you lose money compared to a comparable index fund. But a new paper shows that certain VC-backed IPOs deliver alpha for investors.

Do broker dealers put customer interests first? Don’t count on it if you are buying or selling municipal bonds.

Despite the overwhelming academic evidence demonstrating the superior, long-term performance of index funds, investors may want to invest in actively managed products. New research shows the importance of choosing low-cost funds.

Resisting recency bias is the key to earning the premiums available from all risky assets, as this example illustrates.

Special purpose acquisition companies (SPACs) impose costs that are subtle, opaque and poorly understood. New research shows just how much SPAC investors stand to lose.

Sustainable investing continues to gain in popularity, with investors worldwide frequently attracted not only by ethical concerns but also by the lure of superior returns. Unfortunately, new research focused on global stocks showed that they did not get what they were sold.

The failure of SVB led to a broader concern over the stability of the financial sector. That has led to fears about client assets held at Charles Schwab, But those concerns are overblown.

The economic signals and a host of geopolitical risks confronting investors suggest that 2023 could be as challenging as 20022 for both stocks and bonds.