The Opportunity in CLO Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Collateralized loan obligations (CLOs) were abandoned after the global financial crisis (GFC) of 2007-2009. Since then, CLOs have made a comeback due to their strong performance during the GFC and beyond. CLO notes issued before the GFC did not have material defaults, and many CLO equity securities issued then ended up with annualized returns above 20%.

Collateralized loan obligations (CLOs) were abandoned after the global financial crisis (GFC) of 2007-2009. Since then, CLOs have made a comeback due to their strong performance during the GFC and beyond. CLO notes issued before the GFC did not have material defaults, and many CLO equity securities issued then ended up with annualized returns above 20%.

By 2021, the CLO market had surpassed $1 trillion in assets under management and had replaced banks as the largest lender to private-equity-backed companies.

In its 2020 second quarter report on CLOs, Standard & Poor’s reported that two-thirds, or $2.1 trillion, of leveraged-loan issuance since the GFC had been funded by CLOs. Among the broad range of financial institutions that invest in CLOs are banks, insurers, pension funds, mutual funds and hedge funds. Ratings-based capital regulation incentivizes banks and insurance companies to purchase highly rated debt instruments that reduce capital charges. Specifically, CLO debt tranches appeal to this incentive because they have higher credit ratings than the underlying collateral. There are a few other reasons why investors find leveraged loans attractive:

- They offer attractive income, currently around 3.5% over a floating rate of the secured overnight funding rate (SOFR).

- They default rarely, and if they do, the leveraged loan owners recoup about two-thirds of their money.

The historical recovery rates are shown in the table below:

- Lenders will extend favorable terms to finance diversified pools of leveraged loans, as they are overcollateralized by the CLO equity.

- In all but three of the last 20 years, leveraged loans have provided positive returns.

Many CLOs issued today have expected lives of eight or more years. Tranches are the different portions of the CLO’s financing that have ratings from AAA down to equity. The CLO’s cost of debt is locked in for its life. But the CLO’s equity investors have the option to refinance specific CLO tranches at more favorable rates after the end of a non-call period, typically two years. The equity tranche is the most subordinated one (and thus the riskiest) and is not rated.

CLO equity offers the potential for mid-teens returns with a low correlation to other asset classes such as stocks or high-yield bonds. In contrast to other alternative investments, there is no J Curve in CLO equity, which is a benefit – investors can start recouping their initial investment quickly. That’s because CLOs pay quarterly distributions, and the initial distributions can be in the mid-teens or higher. The high initial cash flows mitigate the investment risk and make it harder, though not impossible, to have a negative lifetime internal rate of return (IRR).

Until recently, individuals could invest in CLOs only through private vehicles. However, in 2018 Flat Rock Global launched the Flat Rock Opportunity Fund (FROPX), an interval fund investing in CLO equity, and this year launched the Flat Rock Enhanced Income Fund (FRBBX), which invests in BB-rated CLO notes. They each provide a limited minimum liquidity of 5% per quarter.

Their findings led the authors to conclude that the resilience (with respect to market volatility) of CLOs was attributable to several structural features:

- CLOs are closed-end vehicles in which capital inflows and outflows are limited.

- Coverage tests are based on loan par values and credit ratings instead of market prices. Consequently, market volatility did not cause the diversion of cash flows to pay down debt tranches unless the volatility coincided with rating downgrades and defaults.

- Embedded options to reinvest collateral and reissue debt after a non-call period enabled opportunistic trading and refinancing by CLO managers.

- CLOs employed a long-term funding structure known as “term leverage” that insulated the vehicle from rollover risk. Unlike most levered investment vehicles that used short-term debt (e.g., hedge funds), CLOs issued long-term debt with maturities in excess of seven years and fixed credit spreads.

Cordell, Roberts and Schwert concluded: “Taken together, our results suggest that equity investors earn economic rents for providing risk-bearing capital that supports lending to risky borrowers and the issuance of highly rated tranches. These rents derive from borrowers willing to pay high risk-adjusted spreads for loans due to an inadequate supply of intermediated credit, intermediaries willing to earn low risk-adjusted spreads on CLO tranches to satisfy their demand for safe assets that reduce capital charges, or both.”

Further evidence

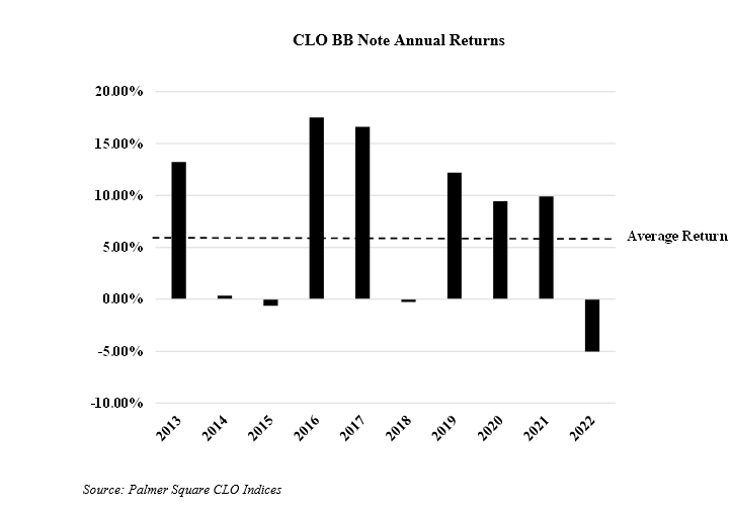

In his soon-to-be-released book, CLO Equity and BB Investing, author Shiloh Bates presented the following chart on the returns to the equity tranches of CLOs:

Bates also presented evidence for the returns to the BB portion of CLOs. From 2012 through 2022, CLO BB notes returned 7.1% annually, 6.3% above the return on one-month Treasury bills. Future BB note returns were expected (not guaranteed) to be higher, as SOFR increased substantially in 2022, spreads widened, and most CLO BB notes were also trading below par value.

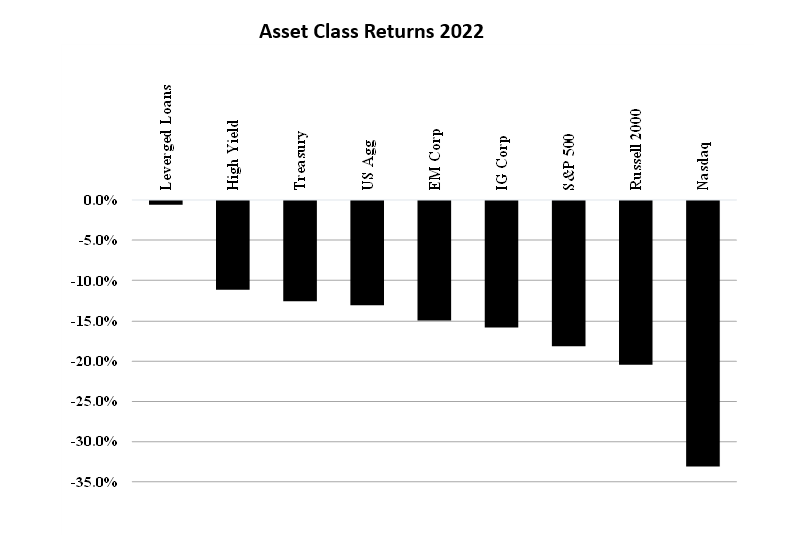

The following chart showing the 2022 returns to various asset classes, both stocks and bonds, highlights the value of being floating rate and first lien during economic headwinds:

Using the backtest tool at Portfolio Visualizer, we can also examine the returns of four public CLO equity funds: the internal fund, Flat Rock Opportunity Fund (FROPX); and three closed-end funds, Eagle Point Credit Co LLC (ECC), OFS Credit Company Inc (OCCI), and Oxford Lane Capital Corp (OXLC). The period is May 2018 (the inception of FROPX) to May 2023. The superior performance of FROPX is in part explained by its lower expenses.

Investor takeaways

Cordell, Roberts and Schwert demonstrated that CLO equity had earned abnormal positive returns by exploiting risk-adjusted price differentials between the markets for leveraged loans and CLO debt securities. This surplus did not come from managerial skill in selecting leveraged loans, though there was heterogeneity in performance across managers. They also found that CLO equity exhibited a great deal of resilience to market volatility even during the GFC and the first year of the COVID-19 crisis. That resilience was due to the long-term, closed-end financing structure of CLOs, which provides equity investors with a levered position insulated from capital outflows and rollover risk.

Investors willing and able to accept the illiquidity risk of CLOs should consider them as alternatives with attractive risk/reward characteristics. A potential downside to CLO equity is volatility, which can be equity-like in some market environments. While investment banks will make a market in CLO equity, the bid-ask spread could be wide. As a result, think of CLO equity as a long-term investment.

Based on the evidence from Shiloh Bates’ CLO Equity and BB Investing (which I highly recommend for those interested in this asset class): “An investor in CLO BB Notes may target a low double-digit return, while taking less risk than the CLO equity investors. The BB Note investors have a secured interest in the leveraged loans in the CLO, but they sit behind more senior noteholders in payment priority. The CLO BB Note investor benefits from the initial equity contributed to the CLO, which takes the first loss on the underlying leveraged loans. Additionally, if loans owned by the CLO deteriorate in credit quality, it’s possible to redirect the CLO's profitability from the equity tranche to benefit the CLO's noteholders.”

For those investors not familiar with CLOs, the following appendix provides a brief description of their attributes.

Appendix

Types of CLOs

There are 2 types of CLOs that differ in the type of loans they acquire: broadly syndicated loans (BSLs) and middle market (MM) transactions. BSL CLOs invest in loans to large firms (i.e., earnings before interest, taxes, depreciation, and amortization [EBITDA] in excess of $100 million) that are originated by banks and syndicated widely to bank and nonbank investors. In MM deals (about 10% of the market), the CLO manager plays a dual role, originating loans to small- and medium-size companies often in cooperation with a small “club” of related lenders, and then including the loans in the CLO collateral pool they manage.

The CLO’s collateral manager not only picks the initial loans for the CLO but keeps it fully invested through the reinvestment period. Additionally, the collateral manager will work to keep the CLO in compliance tests. CLO managers usually charge a fee of between 30 bps and 50 bps on total assets annually to perform this function. Additionally, there is typically an incentive fee of 20% of equity cash flows after realized returns exceed a 12% hurdle.

Assets of CLOs

The collateral of CLOs consists primarily of floating-rate, senior secured term loans with maturities between 5 and 7 years. The typical CLO holds loans issued by 150 to 250 distinct borrowers. To ensure diversification, standard contract terms limit exposure to any industry at 15% of the loan pool and to any company at 2%. Contracts also limit the portfolio share of loans paying fixed or semiannual (as opposed to quarterly) coupons, loans rated CCC+ or below and loans that mature after CLO debt securities.

The liabilities consist of a combination of debt and equity tranches. Debt tranches are floating-rate claims secured by the loans in the collateral pool. The floating-rate nature of these claims matches that of the collateral, thereby insulating investors from interest rate risk. Debt tranches are differentiated by their priority in the CLO capital structure and consequently the interest rate spread they are promised. Equity investors receive unsecured, unrated claims.

The following chart shows the typical CLO structure in the post-GFC era:

CLO life cycle

Before the CLO is created, a warehouse facility (bank line of credit) is formed to acquire leveraged loans that will comprise the collateral pool. On the CLO’s pricing date, its financing is arranged; it is typically a month before the financing closes. That gives the CLO additional time to add to the leveraged loan portfolio. When it is mostly done investing its portfolio, the CLO becomes effective. That’s when the rating agencies confirm their ratings and the CLO’s tests begin being measured. CLOs make their distributions quarterly, but usually the first payment will lag, as the CLO is likely not fully invested at closing. Two years into the CLO’s life, the non-call period on its debt ends, and equity investors can begin making equity-accretive changes to the CLO’s financing. At the end of the five-year reinvestment period, the CLO will begin deleveraging as prepayments are received from the leveraged loans. The deleveraging process ends when the equity investors decide to call the CLO.

Distributions to debt tranches

Cash flows from the collateral pool are distributed to investors according to a “waterfall,” or priority structure, set forth in the CLO indenture. Interest received from the collateral pool is first used to pay administrative expenses and senior management fees. The remainder is used to pay interest on the secured notes, beginning with the senior tranches, followed by the mezzanine tranches, and then the junior tranches. Principal payments received during the reinvestment period are used to invest in new loans. After the reinvestment period, during the amortization phase, principal payments follow a waterfall similar to that used for interest payments. An exception to this distribution scheme occurs when a coverage test is failed. Failure occurs when the quality of the collateral pool deteriorates because of defaults or a large fraction of downgrades to CCC+ or lower. The consequence of failure is the repurposing of loan interest payments to pay down the principal of senior noteholders until the coverage test is passed. Any remaining interest is then used to pay interest according to the priority structure. Thus, coverage tests act as automatic stabilizers that deleverage the capital structure of the CLO and protect senior investors against the loss of principal in the event of credit deterioration.

Distributions to equity tranches

Distributions to equity come from excess interest and principal payments generated by the collateral pool. This excess cash flow arises from two credit enhancements present in all CLOs: overcollateralization and excess spread. Overcollateralization refers to the aggregate par amount of the collateral pool being greater than that of the debt tranches. This excess collateral is purchased with the proceeds from the equity investors, though they have no contractual claim to it (i.e., equity is unsecured). As with interest payments, this excess collateral can be distributed to equity investors only after all the debt tranches have been made whole. The average CLO has $1.12 of collateral for each dollar of debt issued.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. The securities mentioned should not be construed as a recommendation. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth or its affiliates. LSR-23-515

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All