The Stone Ridge High Yield Reinsurance Fund (SHRIX) was introduced a decade ago to provide pure exposure to catastrophe-reinsurance risk that had historically delivered excess returns. Let’s look at how it performed over that period.

The Stone Ridge High Yield Reinsurance Fund (SHRIX) was introduced a decade ago to provide pure exposure to catastrophe-reinsurance risk that had historically delivered excess returns. Let’s look at how it performed over that period.

Traditionally, portfolios have been dominated by public equities and bonds. The risks associated with the equity portion of those portfolios are typically dominated by exposure to market beta. And because equities are riskier than bonds, beta’s share of the risk in a traditional 60% equity/40% bond portfolio is much greater than 60%. In fact, it can be 85% or more (the shorter the bond duration, the greater the risk share of market beta).

To provide a vehicle that provided further diversification benefits, in February 2013 Stone Ridge launched SHRIX, one of the first 1940 Act funds to invest primarily in catastrophe bonds, a liquid way to access the reinsurance-risk premium. Reinsurers are paid a premium in exchange for providing the valuable service of protecting insurers against rare but catastrophic events that might create enough claims to bankrupt them. The fund’s target allocation is 85%-90% to liquid catastrophe bonds and 10%-15% to illiquid quota shares (risk-sharing contracts with reinsurers). The fund has an expense ratio of 1.74%.

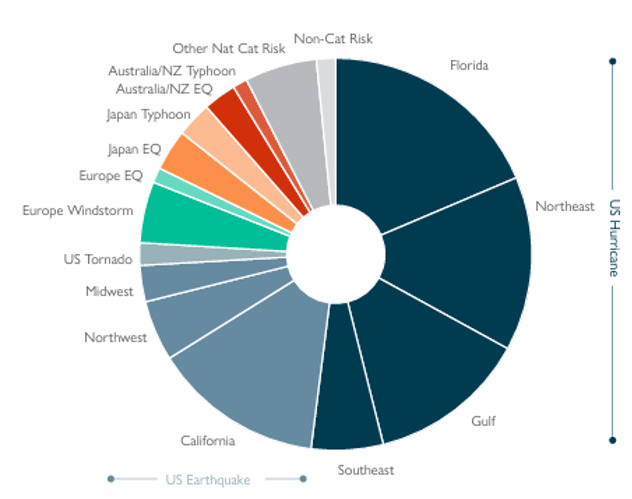

The following table shows SHRIX’s risk allocation and diversification by geographical region and peril as of September 30, 2023.

I will start by reviewing the fund’s performance in isolation.

Performance

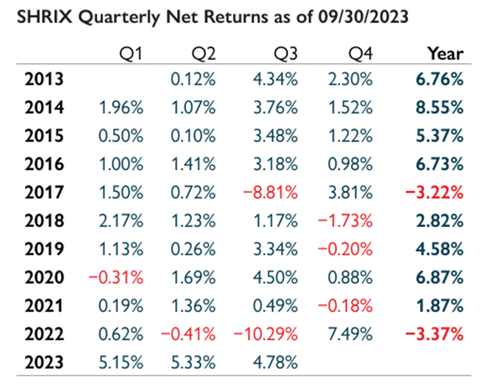

The quarterly performance of the fund over the last 10 years is shown here:

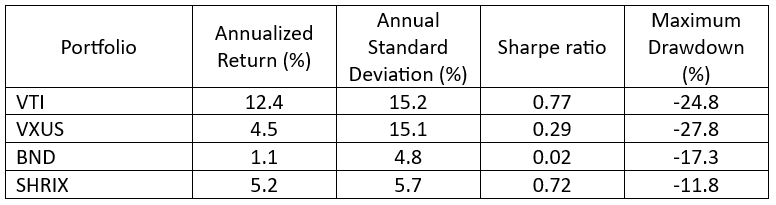

The table below shows the annualized return, volatility (standard deviation), and Sharpe ratio (risk-adjusted return) for SHRIX as well as those of Vanguard’s Total Stock Market ETF (VTI), Vanguard’s Total International ETF (VXUS), and Vanguard’s Total Bond ETF (BND). Data is updated through November 2023.

Every investor should be interested in including in their portfolio a fund with a Sharpe ratio of about 0.7 with very low correlation to both traditional stocks and bonds.

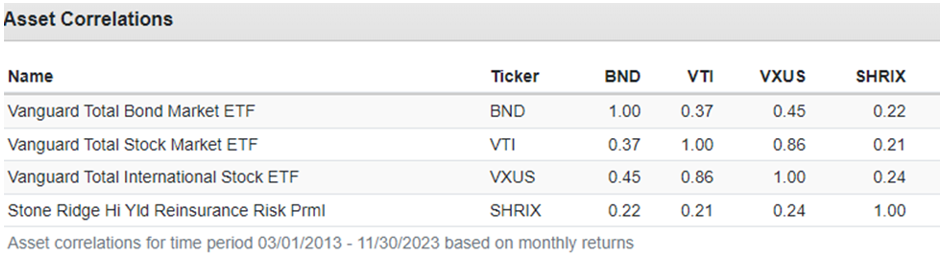

While I reviewed the fund’s performance in isolation, sophisticated investors know the right way to view performance is how the addition of an investment impacts the risk and return of the entire portfolio. A fund can add value beyond its individual return contribution by providing unique risk exposures with low correlations to the other portfolio assets. The table below, from Portfolio Visualizer, shows the annual correlation of the four funds listed above.

SHRIX exhibited very low correlation to each of the three core funds – providing evidence of the diversification benefit of adding SHRIX to a balanced portfolio of stocks and bonds. I cannot provide examples to help with that; the SEC marketing rules have very strict requirements for the presentation of back-tested hypothetical portfolios because they can be abused by cherry picking of data by funds and advisors who are marketing funds versus providing educational information. If you are interested in seeing the benefits, use the back-test tool at Portfolio Visualizer.

Investor takeaways

As the evidence presented demonstrates, investors willing to accept the tracking-variance risk (the risk of underperforming traditional assets) of investing in nontraditional assets that have historically documented risk premiums that have been persistent, pervasive, robust and survive implementation costs, and also have logical explanations for why the premium should persist, can improve the efficiency of their portfolio.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners, collectively Buckingham Strategic Wealth, LLC and Buckingham Strategic Partners, LLC.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Information from sources deemed reliable, but its accuracy and completeness cannot be guaranteed. Investors should carefully consider any fund investment risks and investment objectives. Certain funds may not be appropriate for all investors and are not designed to be a completed investment program. As such, this article does not constitute a recommendation to purchase a specific security and it should not be assumed that the securities referenced herein were or will prove to be profitable. No strategy assures success or protects against loss Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal. Individuals should speak with their qualified financial professional based on their own circumstances to discuss the ideas presented in this article. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth, LLC or any of its affiliates. LSR-23-596

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

More ETF Topics >

The Stone Ridge High Yield Reinsurance Fund (SHRIX) was introduced a decade ago to provide pure exposure to catastrophe-reinsurance risk that had historically delivered excess returns. Let’s look at how it performed over that period.

The Stone Ridge High Yield Reinsurance Fund (SHRIX) was introduced a decade ago to provide pure exposure to catastrophe-reinsurance risk that had historically delivered excess returns. Let’s look at how it performed over that period.