Using a new database that isolates the activity of retail investors, new research documents their poor performance.

Using a new database that isolates the activity of retail investors, new research documents their poor performance.

In recent years, a large body of research has demonstrated that many financial anomalies produce stronger results when a greater proportion of participants are relatively uninformed (naive) retail traders. Logically then, stocks with heavier institutional participation should be more efficiently priced and thus produce weaker anomaly results. I provide a summary of the findings and then review new research that takes an innovative approach to measuring investor attention.

Empirical evidence

Hung Nguyen and Mia Pham, authors of the 2021 study, “Does Investor Attention Matter For Market Anomalies,” examined the impact of investor attention on 11 stock market anomalies in U.S. markets. They found that the anomalies were well explained by measures of investor attention, which were associated with the degree of mispricing; anomalies were stronger following high rather than low attention periods. They concluded: “The results are consistent with the conjecture that too much attention allocated to irrelevant information triggers investor overreaction to information. Once the mispricing is corrected, more anomaly returns are realized following high attention periods.”

Jian Chen, Guohao Tang, Jiaquan Yao and Guofu Zhou, authors of the 2020 study, “Investor Attention and Stock Returns,” examined whether an investor attention index based on 12 proxies could predict the stock market risk premium significantly: abnormal trading volume; extreme returns; past returns; nearness to 52-week high and nearness to historical high; analyst coverage; changes in advertising expenses; mutual fund inflow and outflow; media coverage; search traffic on the Electronic Data Gathering, Analysis and Retrieval (EDGAR) system; and Google search volume. They found that investor attention matters at the market level: It can strongly predict the aggregate stock market in and out of sample when individual proxies are used collectively, yielding sizable gains to mean-variance investors. Conversely, individual attention proxies had limited predictability. They concluded: “There are potentially large investment profits in the asset allocation based on aggregate investor attention, suggesting substantial economic values for mean-variance investors. This analysis then emphasizes the important role of investor attention on the aggregate stock market from an asset allocation perspective. … The predictive power of aggregate investor attention for [the] stock market is likely derived from the reversal of temporary price pressure caused by net buying and from the stronger power for high-variance stocks.”

Muhammad Cheema, Yimei Man and Kenneth Szulczyk also examined the impact of investor sentiment in their 2020 study, “ Investor Sentiment: Predicting the Overvalued Stock Market,” and found that the Baker-Wurgler investor sentiment index was a reliable contrarian predictor of subsequent one-month, six-month and 12-month market returns but only during high-sentiment periods. For example, they found that during high-sentiment periods, the return was -0.9% over the subsequent month, -0.8% over the subsequent six months and -0.5% over the subsequent year. Each result was significant at the 1% confidence level. On the other hand, in periods of low sentiment, none of the data was significant.

Malcolm Baker, Jeffrey Wurgler and Yu Yuan, authors of the 2012 study, “Global, Local, and Contagious Investor Sentiment,” investigated the effect of investor sentiment’s global and local components on major stock markets, both at the country-average level and as they affected the time series of the cross-section of stock returns. They found that investor sentiment played a significant role in international market volatility and generated return predictability of a form consistent with the correction of investor overreaction – it was a contrarian indicator of country-level market returns.

Latest research

Vinesh Jha contributes to the literature on anomalies and retail investor attention with his July 2023 study, “Conditioning Anomalies Using Retail Attention Metrics.” He began by noting: “Most traditional datasets do not measure retail attention in an accurate or particularly timely way. For example, determining institutional participation using 13F filings of institutional holdings provides us with a lagged measure, as 13Fs are filed quarterly with a 45-day delay; and furthermore, these metrics are polluted with holdings by passive funds, quant funds with high turnover, and so on.” He added: “A better proxy for retail participation is to measure retail trader attention directly, which we can get from clickstream data. Specifically, we use a dataset that shows, on a daily basis with a one-day delay, the number of investors who are expressing interest in a stock by visiting its ticker page on major financial websites.”

About InvestingChannel

InvestingChannel is a leading online financial marketing and advertisement platform. Its network includes more than 150 financial media publishers including many well-known media properties. The investor audience for these publishers includes about 25 million unique users, primarily retail investors. The platform allows InvestingChannel to collect clickstream traffic data on these sites. ExtractAlpha has processed that data to aggregate all traffic at the individual ticker level each day. The resulting data shows the number of views received by each public firm each day at the specific publisher. The data spans 2017 to the present and covers more than 9,600 public firms in the U.S. alone for 68 unique publishers.

Jha’s database was stocks within ExtractAlpha’s investible universe of U.S. equities only, which requires stocks to have a market capitalization of at least $100 million, an average daily trading volume of at least $1million, and a nominal stock price of at least $4 on the day in question. The resulting universe contained between 2,000 and 4,000 stocks on any given day and covered the period 2017-2022.

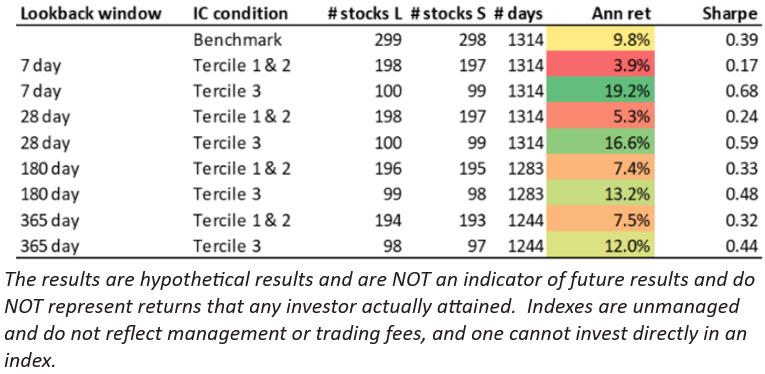

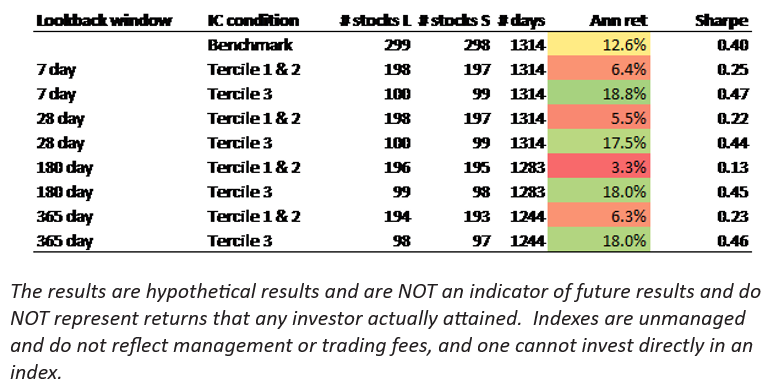

Jha examined the performance of the value and momentum factors conditioned on the level of retail attention, considering the benchmark factor return (the return of the top decile minus the return of the bottom decile) and the returns to the first and second terciles (the stocks with the highest retail attention) versus the returns to the third tercile (the stocks with the lowest retail attention) over various periods (7 days, 28 days, 180 days and 365 days). The table below shows his findings. While the returns to the value long-short benchmark portfolio was 9.8%, the returns to the high-retail-investor-attention stocks were much lower and the returns to the low-retail-investor-attention stocks were dramatically higher, no matter the investment horizon.

The same results were found with the momentum factor.

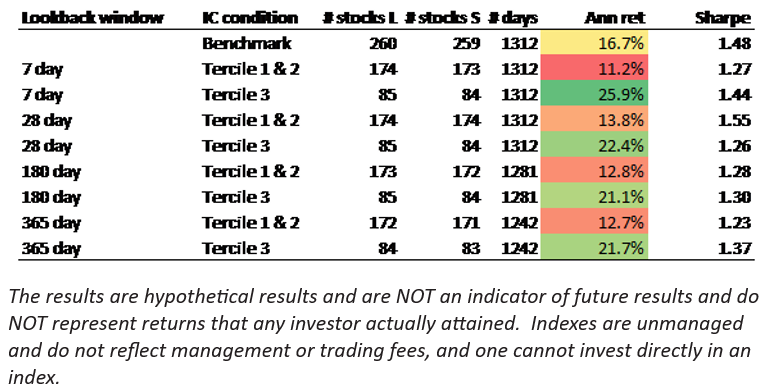

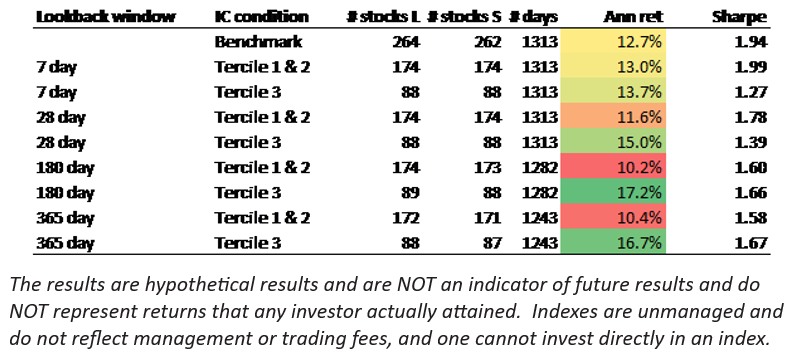

In tests of robustness, Jha replicated his approach with two proprietary ExtractAlpha signals:

- TrueBeats: Forecasts of quarterly earnings surprises based on identifying the top sell-side analysts, trends in earnings surprises and evidence of earnings management.

- Transcripts model: Natural language processing-based sentiment score applied to earnings call transcripts.

As the above charts demonstrate, the results were consistent with those of the value and momentum analyses – the low-retail-investor-attention stocks outperformed the high-retail-investor-attention stocks.

These results are also consistent with those of the 2022 study, “Retail Trading Around Earnings Announcements: Evidence from Robinhood Traders,” which examined the retail trading activities around earnings announcements with data from the U.S. online discount broker Robinhood, “whose clients are known to be mostly young, inexperienced, but tech-savvy investors.” The authors, Qiqi Liang, Mohammad Najand, David Selover and Licheng Sun, found that Robinhood traders swarmed into stocks with pending earnings announcements – earnings announcement dates played a pivotal role in explaining their trading activities. Unfortunately, they also found that Robinhood investors, on average, lost money after the earnings announcements, with negative average returns immediately after the announcements. And the negative returns persisted even after two weeks – casting serious doubts on the premise that Robinhood traders possessed private information, as their bets on a positive post-earnings announcement drift were unfruitful.

Jha also found that his results were robust in that the difference between performance among the high- and low-retail attention names was not isolated to the COVID period – it added value across most periods. In addition, results were also robust across most market-cap slices, though more relevant for small caps (consistent with prior research). The sole exception was value for large caps, where the relationship was reversed. But the value anomaly did not exist over this period anyway.

Jha also ran a horse race with his attention features with a simple metric of percentage of institutional holdings using 13F filings and found that his features were significantly more effective.

Jha concluded: “We believe these findings can motivate any stock selection quant or factor investor to refine their approach to signal implementation using alternative data, even if their horizon is long, and especially if their investment approach is based on traditional investment factors or risk premia.”

Investor takeaways

The evidence demonstrates that the attention-induced behavior of individual investors leads to anomalies (mispricings). That is why retail investors are referred to as “noise traders,” while sophisticated institutional investors are referred to as “informed traders.” Sadly, individual investor trading driven by attention leads to poor returns.

Unfortunately for noise traders, not only do their behaviors tend to negatively impact their returns, but they also pay a price in terms of wasting efforts on nonproductive behaviors. Instead of engaging in attention-driven trading, they could be engaging in far more productive activities and paying attention to the more important things in life (family, friends, activities they enjoy). Helping investors learn this important lesson is one of the greatest value-adds a financial advisor can offer – some would argue it’s priceless.

The takeaway for investors is to avoid being a noise trader. Don’t get caught up in following the herd over the investment cliff. Stop paying attention to prognostications in the financial media. Most of all, have a well-developed, written investment plan. Develop the discipline to stick to it, rebalancing when needed and harvesting losses as opportunities present themselves.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

The opinions expressed here are their own and may not accurately reflect those of Buckingham Wealth Partners, collectively Buckingham Strategic Wealth, LLC and Buckingham Strategic Partners, LLC. For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. This information may be based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. LSR-23-545

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Read more articles by Larry Swedroe

Using a new database that isolates the activity of retail investors, new research documents their poor performance.

Using a new database that isolates the activity of retail investors, new research documents their poor performance.