Special purpose acquisition companies (SPACs) impose costs that are subtle, opaque and poorly understood. New research shows just how much SPAC investors stand to lose.

Special purpose acquisition companies (SPACs) impose costs that are subtle, opaque and poorly understood. New research shows just how much SPAC investors stand to lose.

SPACs are companies without commercial operations yet raise funds through initial public offerings (IPOs) for the sole purpose of merging with a private target company within a limited period of time. In 2020, SPACs set a record of 248 IPOs and $83.4 billion raised in the U.S., only to be eclipsed in 2021 with 613 IPOs raising $162.5 billion, according to SPAC Research.

As was shown in this article, SPACs are created because they are lucrative for their sponsors and for investors who buy units in SPAC IPOs and sell or redeem their shares prior to SPACs completing their mergers. Nearly 100% of investors (dominated by a group of hedge funds called the “SPAC Mafia”) who buy into SPAC IPOs pursue such a strategy. Unfortunately, those gains come at the expense of non-redeeming SPAC shareholders (typically retail investors) and those who buy SPAC shares in the secondary market.

The findings from empirical research, such as the 2021 studies SPACS, A Sober Look at SPACs and JPMorgan’s examination of SPAC returns, have found that costs built into the SPAC structure are subtle, opaque and far higher than has been generally recognized, leading to poor returns to investors. In contrast, the sponsors reap huge returns due to the incentives built into the structure (the equity and warrants received for putting the SPAC together).

In fact, there has never been a year in which SPAC mergers outperformed the Russell 2000.

New research

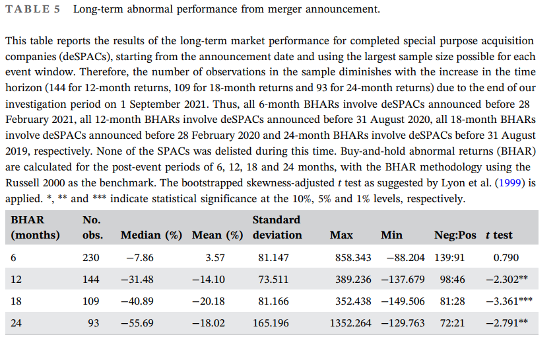

Florian Kiesel, Nico Klingelhöfer, Dirk Schiereck and Silvio Vismara, authors of the study, SPAC Merger Announcement Returns and Subsequent Performance, published in the March 2023 issue of European Financial Management, constructed a dataset of 236 de-SPACs (those SPACs that had undergone a merger) announced in the U.S. between January 2012 and June 2021 for which a merger was consummated by July 1, 2021. They first investigated post‐merger announcement performance in the short term, using the period around the day a SPAC announced a business combination target to gauge stock market response. They then calculated the buy‐and‐hold abnormal returns (BHARs) of these SPACs over six to 24 months from the announcement day and from the de-SPAC date to examine long‐term performance. Following is a summary of their key findings:

- SPACs averaged 284 trading days to announce a target (the announcement of a withdrawal was 382 trading days on average) and an additional 104 trading days to complete the business combination.

- Abnormal returns (including announcements that resulted in the SPAC liquidating without consummating a merger) were, on average, 6.4% in the five days around the announcement of the target. However, the results were short lived.

- Post-merger announcement average abnormal performance was -14.1% after 12 months, -20.2% after 18 months and -18.0% after 24 months.

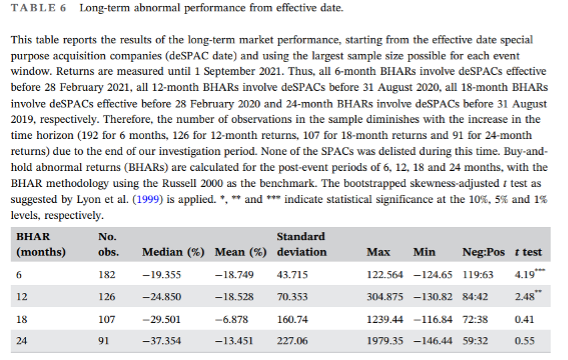

The following table shows the abnormal performance post the effective date of the merger:

Kiesel, Klingelhöfer, Schiereck and Vismara also examined the long-term performance dependent on whether a “top bank” was the SPAC sponsor. They found that even the SPACs sponsored by leading banks produced average negative abnormal returns of -16.1% 24 months post-merger, though they did outperform the others, which produced abnormal returns of -19.6%.

Investor takeaways

In recognition of the problems, on March 30, 2022, the Securities and Exchange Commission proposed a bevy of new requirements for SPACs and their takeover targets amid widespread concern that the vehicles skirt important investor protections. If implemented, the rules will make it harder for SPACs to raise money from investors and execute mergers. The SEC’s goal is to force the vehicles to meet similar regulatory standards as for IPOs. In particular, the proposal would impose additional disclosure requirements regarding SPAC sponsors, conflicts of interest, dilution and financial statements, among other things; standards around marketing practices, such as the use of financial projections; and gatekeeper and issuer obligations, including expanded potential underwriter liability and potential liability by the target company and its signing persons for a de-SPAC registration statement. Under the proposal, the safe harbor for forward-looking statements under the Private Securities Litigation Reform Act would not be available to SPACs. The proposal also includes a new safe harbor from the obligation to register under the Investment Company Act of 1940 for SPACs that meet the safe harbor’s requirements. April 2023 is the target date for final action.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth, LLC or any of its affiliates. LSR-23-467

Special purpose acquisition companies (SPACs) impose costs that are subtle, opaque and poorly understood. New research shows just how much SPAC investors stand to lose.

Special purpose acquisition companies (SPACs) impose costs that are subtle, opaque and poorly understood. New research shows just how much SPAC investors stand to lose.