Buffett was Right About Sentiment and the VIX as Predictors of Returns

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits In his 2004 letter to Berkshire shareholders, Warren Buffett advised investors: “If they insist on trying to time their participation in equities, they should try to be fearful when others are greedy and greedy only when others are fearful.” New research confirms Buffett’s admonition.

In his 2004 letter to Berkshire shareholders, Warren Buffett advised investors: “If they insist on trying to time their participation in equities, they should try to be fearful when others are greedy and greedy only when others are fearful.” New research confirms Buffett’s admonition.

Academic research on the role of investor sentiment in stock returns, including the 2006 study, “Investor Sentiment and the Cross-Section of Stock Returns,” the 2012 studies, “Global, Local, and Contagious Investor Sentiment” and “The Short of It: Investor Sentiment and Anomalies,” the 2020 study, “Investor Sentiment: Predicting the Overvalued Stock Market,” and the September 2022 study, “A New Firm-level Investor Sentiment,” has found that investor sentiment plays a significant role in market volatility, generating predictability consistent with the correction of investor overreaction. Research also has found that total sentiment is a contrarian predictor of market returns – high investor sentiment predicts low future returns and vice versa. The effect of sentiment is greater on hard-to-arbitrage stocks (due to greater costs and greater risks) and hard-to-value stocks (small-cap, high return volatility, growth and distressed stocks) – stocks that exhibit high “sentiment beta.”

Other research, including the 1987 study, “Expected Stock Returns and Volatility,” by Kenneth French, William Schwert and Robert Stambaugh, has found that stock market returns are negatively related to the unexpected change in the volatility of stock returns. This relationship results in the tendency to produce negative equity returns in times of high volatility – greater-than-expected volatility leads to negative stock returns because investors demand a higher risk premium to compensate them for the greater risk. The result is that the discount rate used to value future cash flows increases, lowering prices. Thus, there is a negative relationship between future returns (as the equity risk premium investors demand increases) and unexpected increases in volatility.

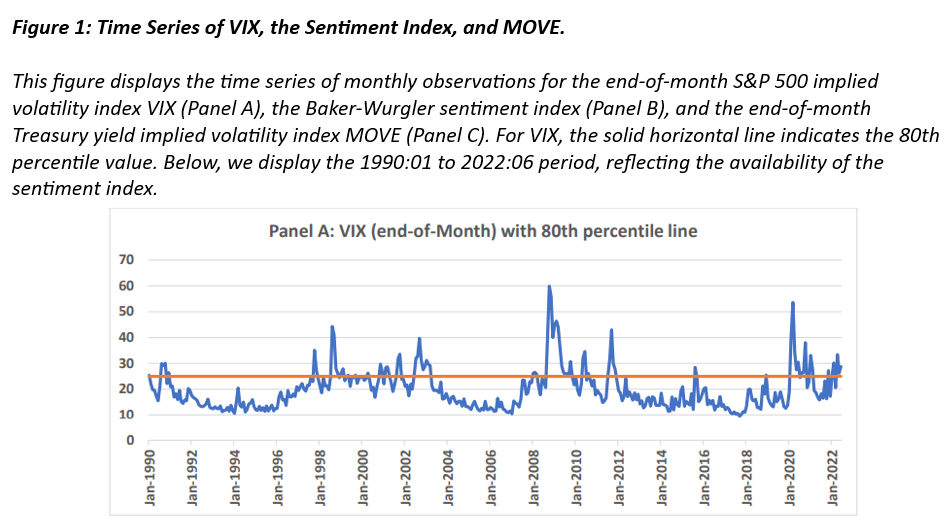

The research has also found that the expected market risk premium (the expected return on a stock portfolio minus the Treasury bill yield) is positively related to the predictable volatility of stock returns – high variance risk premiums predict high future equity returns. Researchers use the VIX as the measure of expected volatility. For example, Naresh Bansal, Robert Connolly and Chris Stivers, authors of the 2022 study, “Beta and Size Equity Premia Following a High-VIX Threshold,” found that the premia from the market beta and size factors were largely earned when expected stock-market volatility breached a high threshold at about the 80th percentile – sizable positive average returns from beta (and size) exposure were persistently evident over months t + 1 to t + 6.

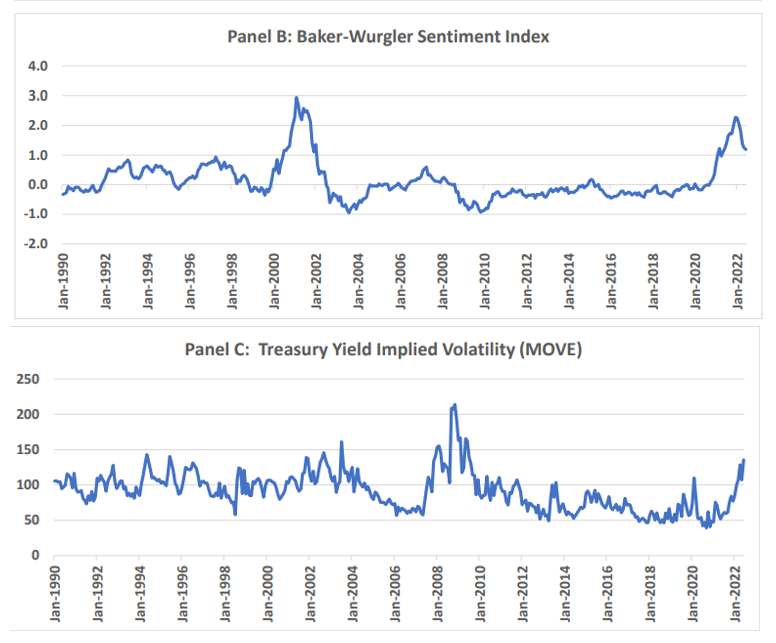

Naresh Bansal and Chris Stivers, authors of the June 2023 study, “Time-Varying Equity Premia with a High-VIX Threshold and Sentiment,” argued: “VIX and sentiment intuitively measure complementary aspects of market risk; in the sense of the level of risk (VIX) and the price of risk or risk appetite (sentiment). Hence, it is important to account for both effects when studying the predictive power of these variables for stock returns.” Due to VIX data availability, their sample covered the period 1990-2022. They estimated an optimal high-VIX threshold indicator variable, at around the 80-85th VIX percentile, as an explanatory term for the subsequent excess equity market returns. They then combined this high-VIX threshold predictive term with sentiment using Baker and Wurgler’s sentiment index. Their specifications skipped a month between the explanatory terms and subsequent excess market returns: “This temporal gap allows some separation between the negative price impact of increasing risk (a largely contemporaneous influence) and the higher premia suggested by elevated risk (a predictive or intertemporal relation).” Following is a summary of their key findings:

- The time variation in the returns earned from equity market exposure was explained well with a simple two-parameter risk-return specification – there was a sizable and reliable negative coefficient on sentiment and a sizable and reliable positive coefficient on the VIX threshold.

- Each explanatory variable had statistically significant incremental predictive power even after controlling for the other variable.

- The model performed strongly at one-, three-, six- and 12-month horizons. The average excess market return was 2.2%, 6.1%, 14.0% and 23.4%, respectively, for periods following a high-VIX threshold breach, but was only 0.30%, 1.3%, 3.3% and 7.4% otherwise.

- A linear sentiment specification dominated a threshold sentiment specification.

- The coefficients on sentiment were negative and highly statistically significant for each of the four return horizons. The explanatory power for the longer-horizon returns was particularly striking, with adjusted R-squared values of 11.6% and 19.5% for the six-month and 12-month return horizons, respectively.

- For all four return horizons and in full-sample and one-half subsample evaluations, the fitted expected returns were always appreciably and reliably higher following a high-VIX threshold and declined with sentiment, especially around peak sentiment times – at 2.93 in February 2001 and 2.28 in December 2021.

- For 12-month (six-month) returns, their specification explained 28.7% (19.2%) of the equity premium variation (in an R-squared sense) over the full sample, with similar predictive power over separate stand-alone estimations over one-half subperiod analysis.

- Holding sentiment constant, the fitted 12-month (six- month) equity premium was 15.6% higher (9.4% higher) following a high-VIX threshold for the 12-month (six-month) return horizon.

- The VIX threshold outperformed other risk explanatory terms suggested by the literature, including the recent high-frequency realized volatility, the equity volatility risk premium, a risk-aversion index measure, stock-market illiquidity and macroeconomic uncertainty.

- Their findings remained strongly evident when controlling for the default yield spread and term yield spread.

The authors noted that the VIX is a highly responsive measure of market-level risk, which can spike dramatically during periods of high market stress. On the other hand, “sentiment is a slower-moving measure of market conditions that can continue to increase during highly optimistic or exuberant times (unlike VIX which seems somewhat constrained to lows of around 10%, even in high good economic times with high sentiment).” They added: “These contrasting features between VIX and sentiment are reflected in their near-zero correlation of 0.038 in our sample.” The one-half subperiod correlations were also modest, at 0.150 over January 1990-June 2006 and -0.027 over July 2006-June 2022. “Thus, high-sentiment episodes might be associated with relatively high current stock prices and then predict lower future returns (with mean-reversion in sentiment). Further, the high-sentiment episode might, perhaps, appear to indicate stock overvaluation in hindsight.” Therefore, the two measures may have different predictive powers for subsequent stock returns. That explains their finding of a sizable and reliable negative coefficient on sentiment and a sizable and reliable positive coefficient on the VIX threshold.

Their findings led them to conclude: “As compared to a typical risk-return specification where the excess returns are linearly related to the lagged VIX, we find strong evidence that our high-VIX-threshold approach appreciably and consistently outperforms a linear VIX approach. This threshold-versus-linear comparative results is also evident both in our full sample and each one-half subperiods.” They added: “The evidence indicates that, as long as a period has sufficient length to include substantial variation in sentiment (including times with substantial peaks) and sufficient VIX-variability episodes, then our findings are likely to be evident over that period.”

Bansal and Stivers then evaluated an extended version of their predictive specification that included the lagged Treasury yield implied volatility index (MOVE) – similar to the VIX, it measures the implied volatility of U.S. Treasury options across various maturities – as an additional explanatory term. A high MOVE index value signifies increased volatility in the Treasury market, a sign of heightened market uncertainty or risk, while a low MOVE index value indicates lower volatility and suggests that market participants expect a more stable interest rate environment. The authors explained: “Then, times with unusually high MOVE (relative to VIX) would indicate less of a risk differential between stocks and longer term bonds (less than usual), with bonds being less of a safe haven then. If so, this implies that investors would reallocate risky assets more into stocks (more than typical), implying a relatively lower equity premium to hold stocks.” They found that while VIX and sentiment retained their strong predictive power, the addition of the MOVE explanatory term adds appreciable explanatory power in the post-1997 period: “MOVE has a strong and statistically significant negative relation with excess equity returns when combined either with the high-VIX threshold explanatory term or with both the high-VIX threshold and sentiment explanatory terms, with t-statistics ranging from -2.44 to -3.63. Moreover, addition of the MOVE term substantially increases the predictive power of the model in terms of R-squared values. For example, the full specification with the VIX-threshold, sentiment, and MOVE explanatory terms have R-squared values of 35.3% and 54.1% for the 6-month and 12-month horizons, respectively.”

Summarizing, Bansal and Stivers concluded: “Our findings suggest that the implied volatility of Treasury yields can also assist in explaining the risk-return relation in the equity market, particularly in the post-1997 period. However, our two-parameter ‘high-VIX-sentiment and sentiment’ model remains robust to controlling for MOVE, indicating that VIX and sentiment jointly capture complementary aspects of the market’s risk and risk appetite.” They added: “Our results are consistent with a common, intuitive 20/80 thumb rule: most of the excess returns earned from market-level exposure are realized in the 20% of times following the highest VIX values.”

Investor takeaways

The empirical evidence demonstrates that when equity markets are under stress, investors perceive markets to be highly risky, and the variance risk premium rises such that the VIX is above the 80th percentile. That is when investors have earned the highest equity returns. That is consistent with Buffett’s warning cited at the beginning of this article.

Investors’ equity allocations shouldn’t take more risk than they have the ability, willingness and need to take because doing so might cause them to panic and sell just when expected returns are highest (as compensation for the high degree of perceived risk). They should also avoid becoming too optimistic when markets are calm (and investor sentiment is high), as the historical evidence demonstrates that is when equity returns have been relatively poor. Bansal and Stivers noted that the VIX value is almost always in the low-VIX state during the high-sentiment episodes, which effectively allows for a lower risk premium in times of higher sentiment (presumably associated with a lower price of risk) and a lower level of risk.

Investors are best served by having a well-thought-out plan that anticipates both types of periods (high sentiment combined with below-threshold VIX, and high-threshold VIX), and they should stay the course, rebalancing along the way.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. LSR-23-523

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All