How to Select PE Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Private equity (PE) has become a staple of institutional portfolios, but its performance has often been disappointing. New research shows that the levels of specialization and portfolio diversification should be important considerations when selecting a manager to implement a PE strategy.

Private equity (PE) has become a staple of institutional portfolios, but its performance has often been disappointing. New research shows that the levels of specialization and portfolio diversification should be important considerations when selecting a manager to implement a PE strategy.

Over the past 40 years, the private equity (PE) industry has grown rapidly. Attracted by the glamour and potential for lottery-like returns, global PE assets under management reached $4.2 trillion by 2022, and are typically a significant component of the portfolios of many insurance companies, pension funds, university endowments and sovereign wealth funds. But because of minimum net worth requirements, most individual investors don’t have direct access to the asset class.

Private equity (PE) involves pooling capital to invest in private companies either in the form of venture capital (VC) to startups or by taking over and restructuring mature firms via leveraged buyouts (LBOs). Investors who use PE believe the benefits outweigh the challenges not present in publicly traded assets – such as the complexity of structure, capital calls, illiquidity, higher betas than the market, high volatility of returns (the standard deviation of private equity is in excess of 100%), the extreme skewness in returns (the median return of PE is much lower than the mean [the arithmetic average], lack of transparency and high costs. Other challenges for investors in direct PE investments include performance-reporting data that suffer from self-report bias and biased NAVs, which understate the true variation in the value of PE investments.

Gregory Brown, Celine Yue Fei and David Robinson contribute to the literature on PE investing with their August 2023 study, “Portfolio Management in Private Equity.” They used a deal-level data set of 5,925 global investments from 468 distinct buyout funds with vintage years from 1999-2016 operated by 315 distinct private equity firms to analyze how portfolio considerations are important for understanding fund-level private equity returns. They required the following three conditions: that all the holdings in the fund had deal size information (no missing values); that the fund made at least three but fewer than 50 investments; and that the total deal size was at least 25% and not more than 200% of the total amount of committed capital to the fund. The portfolios were global: 52% of the portfolio companies were located in North America and 34% were in Western Europe. They were also diversified, covering all 11 of MSCI’s GICS sectors.

Their main performance measure was the public market equivalent (PME), a measure of the ratio of the discounted sum of cash flows received to the discounted sum of capital invested. Because it is customary to use the realized returns from a broad market index as the discount rate, the PME is often interpreted as an excess return over what would have been earned if the capital invested in private equity had instead been invested in a public market index. Accordingly, the authors used the Russell 3000 for holdings in North America, the Asia and Pacific MSCI performance index for Asian and Pacific holdings, the Europe MSCI performance index for European holdings, and the MSCI World performance index for other holdings. Here is a summary of their key findings:

- The gross mean (median) PME was 1.63 (1.27).

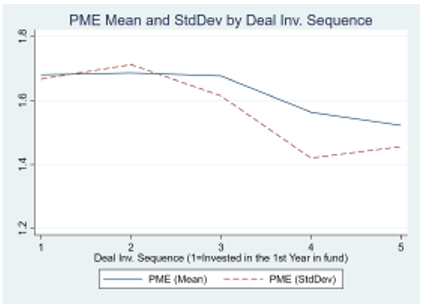

- On average, deal returns in the first few years of a fund’s life had higher returns, with a mean PME of 1.68. Mean (and median) PMEs decreased for later deals. They were also riskier.

Note: This figure plots the mean and standard deviation of deal return in each deal timing sequence category. The horizontal axis is the sequence of the deal (Deal Inv. Sequence). The vertical axis is the mean (Mean, blue solid line) or standard deviation (StdDev, red dashed line) of the deal PME in a given sequence category.

- The largest deal was often exceptionally large, more than 1/7th of total fund value. But concentration fell off quickly, so that the fifth largest deal was generally about 1/12th of total fund value.

- While most buyout funds exhibited fair diversification across industries, the median fund generally focused on a subset of regions.

- Consistent with the idea that general partners (GPs) choose deals to capitalize on their expertise in specific geographies or industries, sector and geographically specialized funds generated higher returns. However, the more specialized funds, being less diversified, had higher overall risk (higher volatility) – a risk-return tradeoff existed between exploiting specialized skills and minimizing downside risk. The findings were statistically significant at the 95% confidence level.

- A fund’s largest deal had the lowest return on average, with a mean PME of 1.26, and as deals became smaller, the mean return increased monotonically until reaching the fifth deal size rank and then stabilized around 1.7. The results were statistically significant at the 99% confidence level. The largest investments were also the least risky.

- The ratios of average deal returns to average risk by size rank of the investments were essentially constant. Both nominal money multiples and using public market equivalents produced similar results.

- Funds started with higher-return deals – the earlier deals in the fund were of higher return and higher risk. The deals made in the later years earned lower returns and were less volatile. The results were statistically significant at the 99% confidence level. But when they examined the ratios of returns to risk (using multiples or PMEs) by year of investment, they were essentially constant across time.

- Funds with stronger early performance did not, in general, have average deal-level performance that exceeded funds without early home runs.

By comparing deal-level to fund-level estimates of the components of return variance attributable to GP skill, timing and idiosyncratic noise, Brown, Fei and Robinson were able to link portfolio formation to overall manager skill. Aggregating across investments within a fund, they found that about 40% of overall variation was attributable to GP skill, and about 48% was attributable to luck. At the individual deal level, however, they found that only 4% was GP skill, and upwards of 90% was luck: “This comparison implies that a significant source of GP skill is the portfolio selection across individual investments.”

Their findings led Brown, Fei, and Robinson to conclude: “Our results show a high degree of interdependence between individual investments in a private equity fund. These results are consistent with the idea that GPs, motivated by career concerns and the incentives of limited partner agreements, approach fund investment through the lens of portfolio formation. … GPs identify good investments of various sizes but are mindful of the risks.” This risk management concern is consistent with the findings of the authors of the 2018 study, “Adverse Selection and the Performance of Private Equity Co-Investments,” who found that large deals (relative to fund size) were significantly more likely to be offered for co-investment.

Brown, Fei and Robinson added: “In sum, in private equity, managers take their biggest bets on their ‘safest ideas’ instead of ‘best ideas.’” Their hypothesis was that the hurdle rate that applies to the carried interest the GP can earn (often 20%) typically applies to the entire fund’s committed capital, incentivizing the GP to play it safe with larger investments and take more risks with smaller ones. They ended with this observation: “The findings in our paper are consistent with a model in which rational, risk-neutral GPs who are interested in maximizing lifetime income arising from fees and carried interest income balance the desire to generate stronger performance in a fund against the potential losses associated with taking greater risk in a fund and potentially sacrificing the going concern value of future funds. The findings are also consistent with behaviorally motivated theories of GP behavior.”

Investor takeaways

Brown, Fei and Robinson demonstrated that there is a trade-off with PE investing. Specialization results in a more focused portfolio that takes bigger bets on a smaller number of investments to earn higher returns; diversification should be expected to earn lower returns on average but with lower volatility. The takeaway for investors is that the levels of specialization and portfolio diversification should be important considerations when selecting a manager to implement a PE strategy.

Another takeaway is that GPs exhibited a deliberate portfolio management process, systematically balancing the risk and return of their portfolios by managing the relative size and timing of investments. Evidence of this should also be an important consideration when selecting a manager.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners, collectively Buckingham Strategic Wealth, LLC and Buckingham Strategic Partners, LLC.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article. The opinions expressed here are their own and may not accurately reflect those of Buckingham Wealth Partners. LSR-23-555

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All