Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

"Recency bias" is giving undue weight to the most recent information. In financial planning, it often stems from headlines reporting the most recent volatility in the market and, by implication, investment returns. Recency bias is one of over 50 different types of cognitive biases listed in Wikipedia, which are defined as "…systematic patterns of deviation from norm and/or rationality in judgment."

Unfortunately, regardless of the evidence, recency bias can never be eliminated for several reasons. It is instinctual. When we were all living in caves thousands of years ago, we needed to be aware of our immediate surroundings for survival (avoiding sabretooth tigers, searching for food, etc.). Driving a car today is similar – drivers must be aware of what is going on immediately around them.

A more obvious reason is the headline or "breaking" news item that constantly bombards us about the Dow Jones or S&P 500. The inference is that the most recent news must be the most relevant.

For personal financial planning, it is not.

As finance professionals, we all have enough training to know that short-term fluctuations are best perceived as random noise around long-term trends, and lifetime financial plans should be based on those long-term trends. Even the journalists (this publication excepted) who report the latest fluctuations and know this don’t care – their job is to capture readers or listeners to sell ads. And they must be doing that job well because advisors in a 2021 survey ranked recency bias as the number one cognitive or behavioral bias they experienced with clients.

How can advisors fight – or at least mitigate – recency bias?

According to the survey, explaining (or re-explaining) the long-term view ranked as the most effective technique for quelling the stress caused by recency bias. One way to take the long-term view is to present facts. Does the historical record suggest that current returns accurately predict future returns? That is, just how strongly is today's return correlated with tomorrow's? Or the next few days? How about this week’s return with the following week or the next few weeks? How about for longer periods? What exactly do the statistical correlations say?

Correlations for the short-term: Days, weeks, months, and quarters

As expected, crunching the numbers leads to very low correlations for daily through quarterly time spans. The details of the tedious calculations are explained below for daily correlations. Similar explanations apply to the weekly, monthly, and quarterly correlations; for brevity, only the daily results are shown here.

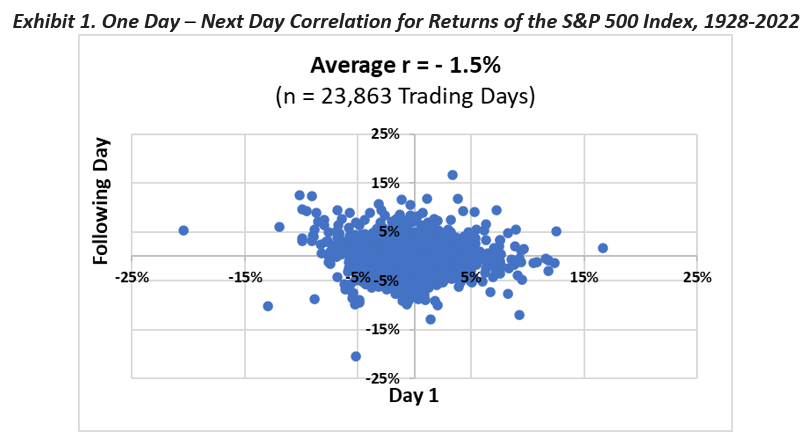

Exhibit 1 displays an actual plot for 23,863 actual trading days’ returns back to 1928 with the following day's return.

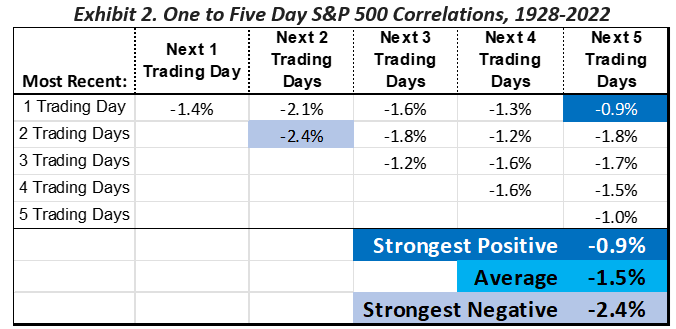

Exhibit 2 shows the correlation coefficients not only for one day versus the next, but also one day versus the next 2, 3, 4 and 5 days. It extends this analysis showing the same results for 2-5 days. Recall that interpreting a correlation coefficient ("r") requires observing both the direction (positive or negative – that is, moving in the same or opposite directions) and strength (+100% is the strongest possible positive correlation, -100% the strongest possible negative, and 0% is the weakest possible correlation). In this case, all correlations were very weak (near zero), suggesting independent behavior from one day or days to the next. The strongest negative correlation was for the average return for two trading days with the following two trading days, -2.4%. The average correlation was -1.5%, and the strongest positive turned out to be least negative, -0.9%.

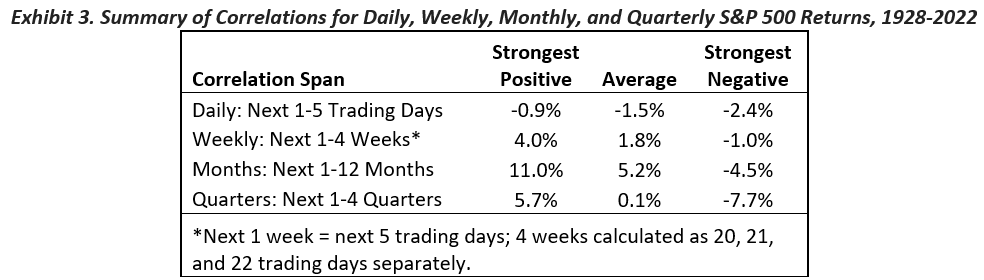

Exhibit 3 summarizes the results equivalent to Exhibit 2 for all short-term time periods – days, weeks, months, and quarters. The primary conclusion from Exhibit 3 is that all are very weak. These are the facts that back up what every financial professional should be telling their clients: "There is no predictive power in short-term market action. It is like trying to predict the outcome of the next flip of a coin when you know the last flip was heads – that information doesn't help predict the outcome of the next flip. They are independent."

Correlations for longer terms: Years and decades

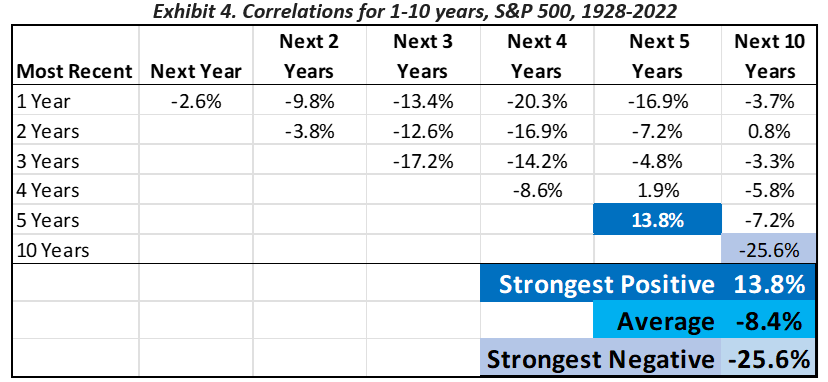

Exhibit 4 presents the correlations for annual returns. Most mutual fund and ETF managers provide data on their last 1, 3, 5 and since inception annual returns. Morningstar presents data back 10 years. Exhibit 4 displays the correlations for annual returns over the spans shown – all weak but a bit stronger than the very short-term spans. The strongest correlation is for this decade's returns and the following decade, -25.6%. Though it is still weak, it is statistically significant at about the .01 level.

This fact confirms that the long-term view is best – longer time spans beget stronger correlations. It suggests looking at even longer spans to see if they produce even stronger correlations. It also gives credence to momentum theory. Momentum is not very strong here for the S&P 500 (13.8% for these 5 years compared to the next 5 years), but it may be present for other individual sectors or securities.

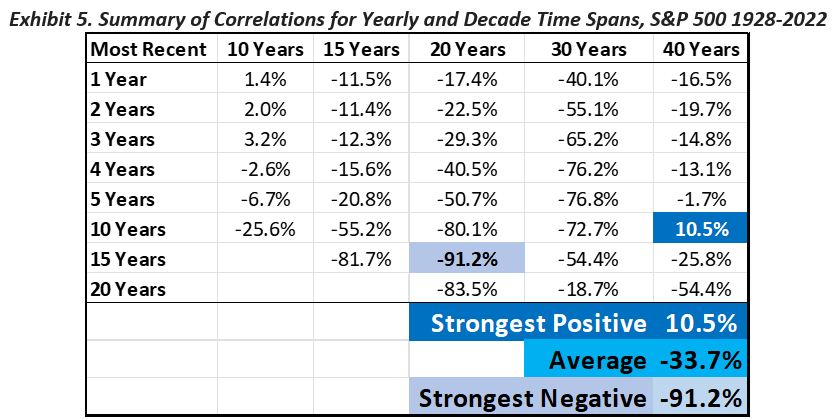

Exhibit 5 presents the correlations for decades, the longest terms examined. The strongest here is for 15 years versus 20 years – a correlation of -91.2%, which is statistically significant at well below the .001 level. (In the computations, the correlations gradually increased with each additional year and the very strongest was for 15 years versus 19 years at 91.5%, but the difference between 91.2% and 91.5% is not statistically significant).

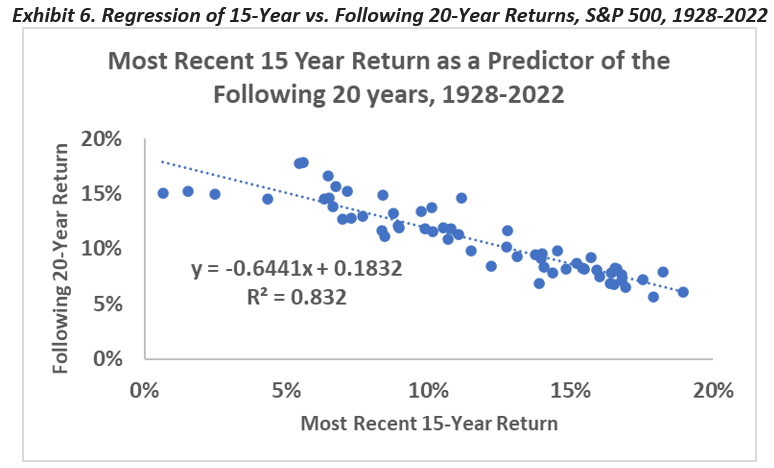

Exhibit 6 provides a scatter diagram of this long-term relationship. The regression yields an unadjusted r-squared value of 0.832 (.912*.912 = .832).

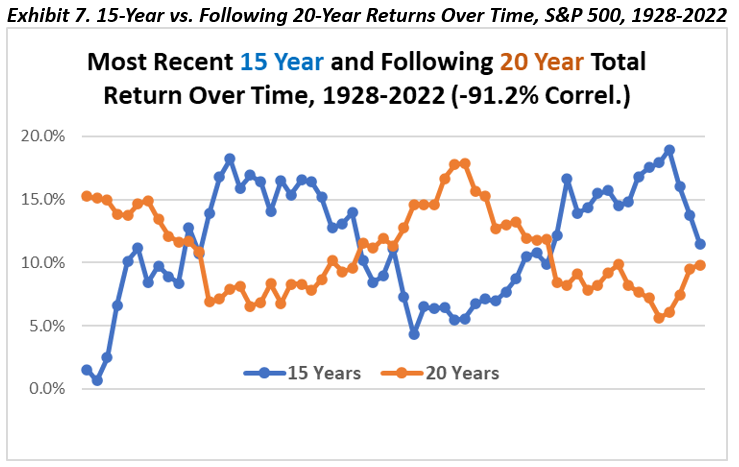

Exhibit 7 provides a further visualization of the 15- to 20-year relationship. It clearly shows that when 15-year returns go up, the following 20-year returns tend to go down.

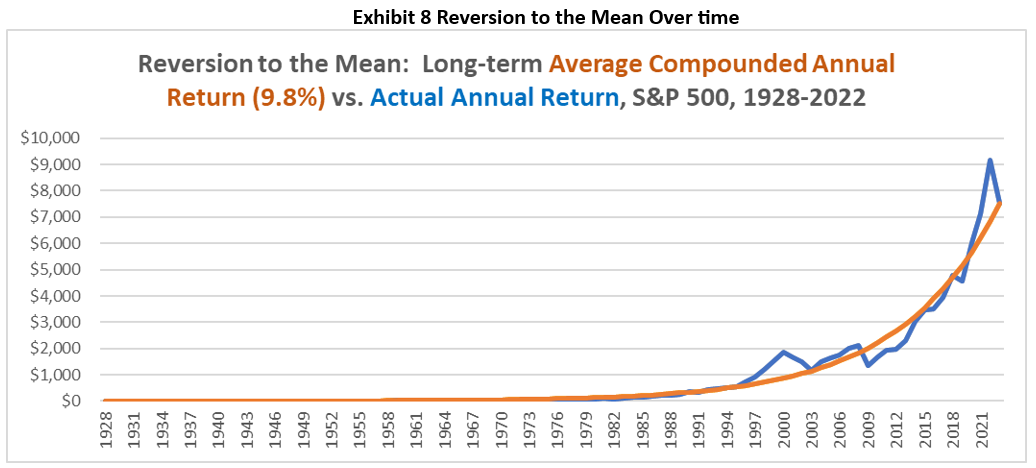

Exhibit 8 displays yet another visual of the data over time. It illustrates what statisticians call “reversion to the mean.” The smooth line shows the average long-term compounded annual return of 9.8% per year. The choppy blue line shows the actual return. It is obvious that it sometimes rises above the long-term average, then falls below in repeating cycles. Hence, the negative correlation.

What do all these correlations tell us?

The only statistically significant correlations in returns involve decades, at least for the S&P 500. For any time period shorter than decades, there simply are no useful correlations, regardless of what journalists imply every day.

This does not mean that the use of other variables would reach the same conclusion, of course. The CAPE may provide some predictive capabilities (see Michael Finke and Larry Swedroe). A study by Vanguard (2012) looked at a number of other factors and concluded none provided very good predictions of the S&P 500. Future research could perform the same correlation analysis for short time spans on other investment indexes to see if the same conclusion holds true.

But even if it is true only for the S&P 500 (which has a correlation of about 95% with the overall market), these charts and tables will help a little by presenting some facts that refute recency bias. That is, what happens in the market in the short run has little bearing on what happens later until you get into decades. But would most clients regard the past 15 years as "recent" when they are reacting to today's market news?

Probably not. Such facts are, unfortunately, unlikely to make much of a dent in recency bias. It is simply too ingrained within us as human beings to ever go away regardless of the evidence. As advisors, we must learn to manage it.

Brent Burns is president and co-founder of Asset Dedication (a turnkey investment platform for financial planners) and a frequent speaker and author on retirement income, investments, and technology. As an adjunct professor, Brent periodically teaches Personal Financial Planning, Data Analytics, and Introduction to Finance. He co-authored Asset Dedication (McGraw-Hill, 2005) with Stephen Huxley. Reach him at [email protected].

Jeremy Fletcher, MBA, CFA (since 2000), is managing director of investments and has been in fixed income management since 1991. Previously, Jeremy co-managed the $3.5 billion fixed income assets at the City and County of San Francisco and managed $2 billion at American Century Investments, launching a top-performing U.S. fixed income fund. Reach him at [email protected].

Stephen J. Huxley, PhD, is director of research and co-founder of Asset Dedication, a professor of Business Analytics, and former Associate Dean, University of San Francisco. He is a recipient of teaching, research, and service awards at USF and in international competitions with numerous publications. Stephen co-authored Asset Dedication (McGraw-Hill, 2005) with Brent Burns. Reach him at [email protected].

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

More ETF Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.