On July 21, 2020, this article was corrected to attribute the term "animal spirits" to John Maynard Keynes instead of Adam Smith.

On July 21, 2020, this article was corrected to attribute the term "animal spirits" to John Maynard Keynes instead of Adam Smith.

What return can I expect from my stock investments over the next 10 years?

The most common answer is to use the historical average. The geometric average historical return on the S&P 500 is about 10%.

Is it reasonable, then, to project 10% stock returns?

Another method is to consider the valuation of stocks. If stocks are at a higher price than their historical average as a multiple of recent earnings, can we then expect a lower return than we have in the past?

Can valuations predict future earnings?

There have been a number of recent criticisms of Robert Shiller’s measure of stock valuation – the cyclically-adjusted price to earnings ratio (CAPE) – as a predictor of future stock returns. A 2017 Advisor Perspectives article pointed out that the ratio wasn’t a realistic measure of future stock returns because 10-year earnings included the global financial crisis. Others have argued that changes in accounting rules mean that you can’t compare today’s CAPE to historical CAPE. An analysis by Vanguard found that the R-squared, or predictive ability, of the Shiller CAPE and 10-year returns between 1926 and 2011 was 0.43. Although 0.43 is high for an asset whose returns are assumed to be random, it gives CAPE critics a reason to dismiss its value.

Care to guess how well the monthly CAPE predicted future 10-year returns between January 1995 and May 2020?

In a period where accounting rules changed and the 2008 global financial crisis decimated profits, CAPE explained 90% of the variation in 10-year returns. Here’s what it looks like when I model 10-year nominal, annualized, geometric returns starting every month from January 1995 through June 2010 (185 blue dots) as a function of their CAPE value during this period:

The standard deviation of the error (how far off the prediction was from the actual value) is 1.37%. This is the difference between the predicted annual return (the yellow dot) and the actual return (the blue dot) at each initial Shiller PE ratio. In other words, 67% of the time the return was plus or minus 1.37% from the CAPE model prediction; and 95% of the time the actual return was within 2.74% of the future 10-year predicted returns. CAPE’s ability to predict 10-year future returns during the last 25 years has been remarkable.

As I write this, the S&P CAPE is 29.28. The 10-year return we can expect using the 1995-2020 model is 5.89%, with a 67% probability that it will be between 4.52% and 7.26%. This is about 1% per year lower than Blackrock’s 10-year capital market expectations for large-cap U.S. stocks, but still in the ballpark.

Over the next 10 years, a hypothetical equity return of 10% is exactly three standard deviations above what the CAPE model would predict (5.89%). If returns are normally distributed, a 10% S&P return has about a 0.3% chance of occurring (or a 99.7% chance of not happening).

Was the 1995-2020 period different than historical periods? As the Vanguard study notes, CAPE predicted only 43% of the variation in 10-year S&P returns between 1926 and 2011. You might expect that the recent predictability of CAPE is an anomaly.

It’s not.

Since 1975, the Shiller CAPE has explained 85% of variation in future stock returns. In fact, CAPE’s ability to predict 10-year returns was remarkably strong until just before the Great Depression. The R-squared starting at 1940 is 0.7. It’s hard to dismiss the value of an indicator that can predict 70% of the variation in future stock returns.

The figure below shows CAPE’s ability to predict 10-year returns beginning in 1920. I started with the Jan 1995-May 2020 time period and went back in time to estimate how the R-squared changed within various periods. The predictability of the CAPE model has remained consistent in the post-WW2 era, but the lower predictive power prior to 1975 may mean that the expected future 10-year return of stocks starting from a CAPE of 20 using the 1940 model may differ from the predicted return on stocks using the 1975 or 1995 models. Again, it’s not much different.

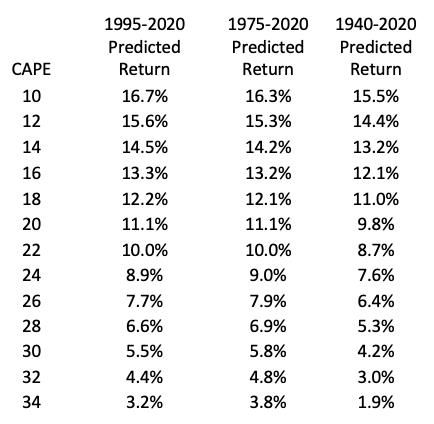

The marginal effect of investing in a higher CAPE stock market today is remarkably similar to investing in high-CAPE periods through the latter half of the 20th century. For each point increase in CAPE, investors should expect a 10-year stock return that is just over half a percent lower. Higher stock returns after 1975 pushed the predicted value up slightly compared to the 1940 model, but not by a huge amount. For example, the predicted S&P return from investing when CAPE values are 20 is 11.1% in both the 1975-2020 and 1995-2020 periods, and 9.8% in the 1940-2020 period.

An investor can grab the current CAPE ratio online and refer to the table below to estimate (with a surprising degree of confidence) the expected return on an equity portfolio over the next 10 years. For a one standard deviation range, add plus or minus 2% to the predicted values for the earlier time periods.

What is CAPE measuring?

How can stock returns be this predictable? In 1981, economist Robert Shiller rocked the efficient market world when he asked a simple question: If stock prices are rational, why are they so much more volatile than dividends? Historical dividends don’t bounce around all that much, while stock prices exhibit wild swings in value that don’t reflect future volatility in cash flows. Something must be amiss.

Shiller’s article heralded a new stream of literature on the impact of market sentiment, or what John Maynard Keynes referred to as “animal spirits,” on stock prices. Sometimes people are more excited about the idea of investing in stocks, and other times they lose their nerve. This results in valuation swings that are higher during periods of economic expansion and positive sentiment, and fall during recessions when investors are pessimistic.

In my own research, I have found that measured risk tolerance of retirement plan participants rises and falls with periods of high and low market sentiment. During the global financial crisis, risk tolerance, measured using a popular financial planning instrument, had a 0.9 correlation with the S&P 500 and a high correlation with other measures of consumer sentiment. Investors’ appetite for investment risk is not constant.

What is a stock return? According to the capital asset pricing model, a stock returns consist of a risk-free return and a risk premium. The risk premium is the amount of extra expected return that is needed to incent risk-averse investors into buying a stock instead of a bond. The Sharpe Ratio of the market portfolio is positive because investors are generally risk averse, but sentiment can drive the reward for risk up or down. What if the price of risk is driven predictably by market sentiment?

A risk premium that rises and falls with changes in investor risk tolerance has enormous implications for portfolio construction. When investors are risk averse, the market Sharpe Ratio rises and investors receive a greater reward for taking investment risk. When investors are risk tolerant, the Sharpe Ratio falls and investors don’t get as much juice from buying stocks instead of bonds.

The predictability of CAPE presents a problem for those who use historical mean returns to project future returns. Although often considered heresy, return predictability also challenges the investment policy approach of maintaining a constant asset allocation.

Why? Let’s assume two investors – one is a Vulcan and the other a behavioral human whose risk preferences depend on market sentiment. The Vulcan will simply look at current valuations and adjust asset allocations based on the expected return being offered by the market. If the CAPE is 34, the expected stock return is between 2% and 4% over the next 10 years. This paltry compensation for taking investment risk means that the Vulcan will select an optimal portfolio with a lower percentage of stocks. Conversely, the Vulcan will go all-in on stocks when CAPE ratios revert to the teens.

The behavioral investor is willing to accept low-return stocks during an economic expansion because they are highly risk tolerant. During a bear market, they suddenly become risk averse and avoid investing in stocks. A constant equity allocation can help the behavioral investor rebalance toward risk when markets fall and away from risk when markets rise in value. Maintaining a constant allocation is better than the alternative, and automatic rebalancing is one of the reasons target-date fund participants outperform other fund investors.

Constant equity allocations are still not optimal.

Rebalancing toward a desired equity allocation is not optimal because the Vulcan can do better by responding to what markets are willing to pay for risk. Building valuation-based portfolios is hard because portfolio managers and individual investors aren’t Vulcans. They don’t want to take more risk after markets fall. They don’t want to reduce risk when markets rise.

But investors would be wise to think of CAPE as the price of risk. An investor is a price-taker walking through the aisle of the investment store. When risk is on sale, investors should buy more risk. When risk is expensive, they should buy less. And they shouldn’t expect to eat as well when, like today, nothing in the investment store is on sale.

Michael Finke, PhD, is a professor of wealth management and the Frank M. Engle Distinguished Chair in Economic Security at The American College of Financial Services.

More Global Markets Topics >

On July 21, 2020, this article was corrected to attribute the term "animal spirits" to John Maynard Keynes instead of Adam Smith.

On July 21, 2020, this article was corrected to attribute the term "animal spirits" to John Maynard Keynes instead of Adam Smith.