Like Samuel Beckett’s titular character Godot, we are still waiting the all-but-certain U.S. recession. It may yet happen, but it’s wise to understand why forecasters were so grossly incorrect.

Like Samuel Beckett’s titular character Godot, we are still waiting the all-but-certain U.S. recession. It may yet happen, but it’s wise to understand why forecasters were so grossly incorrect.

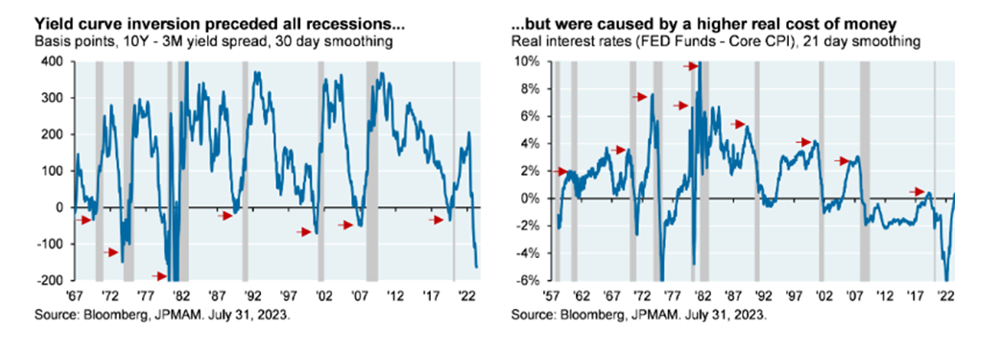

With the Fed raising interest rates above 5%, many have been predicting a recession for a long time. The reasons for the forecast include the fact that the yield curve (10-year Treasury yield minus one-month Treasury yield) turned negative in November 2022 and the index of leading economic indicators fell in July (-0.4%) for the 16th consecutive month. Why has there not yet been a recession? First and foremost is that Fed policy has not been sufficiently tight, as the Fed funds rate has been below the nominal growth of GDP and until recently was not even below the rate of inflation (see chart below at right).

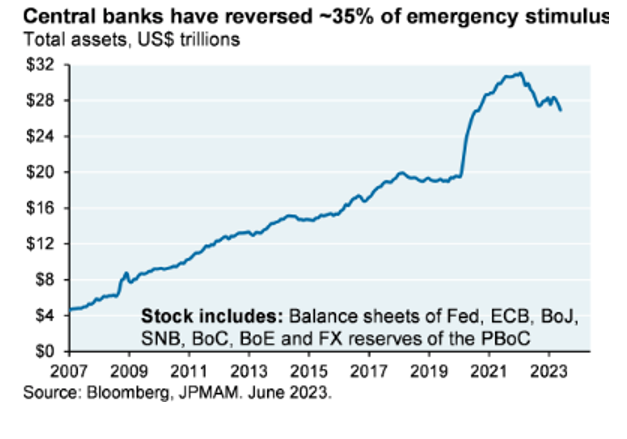

Another explanation is that central banks have removed only around one-third of the $11 trillion in global liquidity they created in 2020-2021 – there is still ample liquidity in the system, and the cost of money is not prohibitive in real terms.

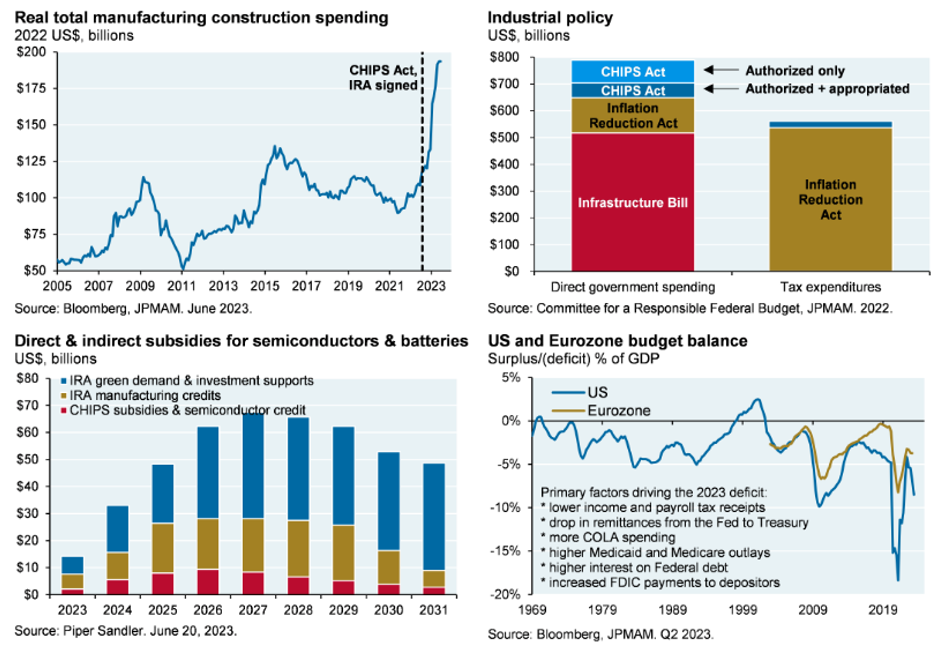

A third explanation is that the administration’s stimulative industrial and fiscal policies have offset part of the drag from higher interest rates. Fitch recently forecasted the 2023 deficit to be 6.3% of GDP. With unemployment at historic lows, we should be running large surpluses, not large deficits that add stimulus to the economy. The charts below show the construction bounce in the manufacturing sector and the direct government spending and tax incentives associated with semiconductor, infrastructure and energy bills.

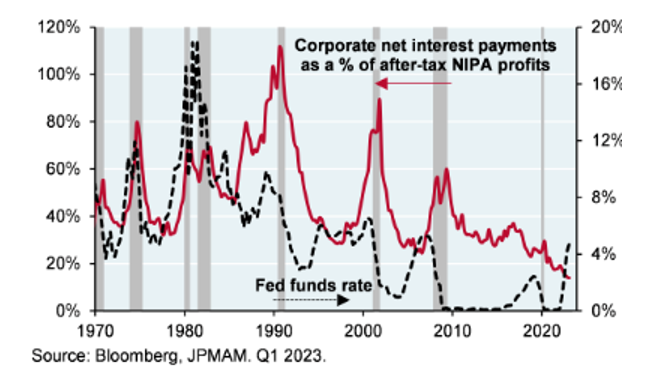

Yet another explanation for the absence of recession is that many U.S. corporations and individuals took advantage of the historically low rates and refinanced, extending maturities and limiting the impact of the Fed’s raising short-term rates. In fact, despite the sharp rise in interest rates, U.S. non-financial interest costs as a percentage of profits is at a 60-year low.

Unfortunately, making an epic error in judgment, the U.S. Treasury failed to take advantage of the historically low long-term rates to extend the maturity of its debt. Thus, U.S. interest costs are now rising sharply, exacerbating the fiscal problem we are facing. On the other hand, U.S. homeowners were a lot smarter. At the end of the June, about 39 million U.S. homes had a mortgage rate below 4.375%. That was more than 73% of the outstanding mortgages in the U.S.

The extremely tight labor market, with unemployment at 3.5%, is another reason why a recession has not yet occurred; employers are reluctant to reduce staff that might be difficult to replace. As of the end of June, there were 9.6 million job openings versus 6.4 million unemployed.

The fact that we have not yet had a recession doesn’t mean we won’t. The third quarter 2023 Survey of Professional Forecasters, released on August 11, projects real GDP to grow 2.1% in 2023, with 1.9% growth in the third quarter and 1.2% growth in the fourth – not a single quarter of negative economic growth, let alone a recession, just a “soft landing.” It also forecasts that economic growth will remain weak in 2024 (growth of just 1.3%). The forecasters have also slashed their estimate of the risk of a downturn in real GDP in the third quarter to 21.7% compared with the estimate of 45.2% in the prior survey. Their estimates of the odds of a recession occurring in the following four quarters are 34.4%, 37.6%, 35.4% and 34.4%, respectively. The takeaway is to treat the mean forecast of 1.3% real growth in 2024 in a probabilistic, not deterministic, way.

Monetary policy, which works with long lags, has not yet been sufficiently tight to cause a recession, and fiscal policy has been extremely loose, creating more demand for goods and services. Thus, the risk is that the Fed will have to tighten monetary policy further to achieve its goal, keeping rates higher and for longer than the market expects.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article. The opinions expressed here are their own and may not accurately reflect those of Buckingham Wealth Partners, collectively Buckingham Strategic Wealth, LLC and Buckingham Strategic Partners, LLC. LSR-23-549

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more articles by Larry Swedroe

Like Samuel Beckett’s titular character Godot, we are still waiting the all-but-certain U.S. recession. It may yet happen, but it’s wise to understand why forecasters were so grossly incorrect.

Like Samuel Beckett’s titular character Godot, we are still waiting the all-but-certain U.S. recession. It may yet happen, but it’s wise to understand why forecasters were so grossly incorrect.