I’ve written previously about how positive (“green”) environmental, social and governance (ESG) metrics have increased the prices of stocks, reducing their expected returns. New research examines a similar effect in bonds, where a “greenium” (lower yield on green bonds versus non-green equivalents) lowers returns for investors.

I’ve written previously about how positive (“green”) environmental, social and governance (ESG) metrics have increased the prices of stocks, reducing their expected returns. New research examines a similar effect in bonds, where a “greenium” (lower yield on green bonds versus non-green equivalents) lowers returns for investors.

There has been explosive growth in interest in sustainable investment strategies. A 2021 analysis by Bloomberg forecasted that assets are on track to exceed $53 trillion by 2025, more than one-third of the estimated global assets under management. The growth of investor demand has been accompanied by heightened interest from academic researchers analyzing its impact on asset prices and expected returns to sustainable investment strategies. While most of the attention has been on equities, researchers have also looked at bonds.

Research, including the 2019 study, “ESG Investing and Fixed Income: It’s Time to Cross the Rubicon,” the 2020 study, “Primary Corporate Bond Markets and Social Responsibility,” and the 2021 study, “Does a Company’s Environmental Performance Influence Its Price of Debt Capital? Evidence from the Bond Market,” has found:

- Environmental performance is negatively associated with the cost of debt – the lower (worse) the corporate environmental performance, the higher the cost of debt, while good environmental, social and governance performance is rewarded by lower credit spreads.

- The integration of environmental factors into investment processes and decision-making exists along each debt maturity, and the longer the maturity, the greater the impact.

- The impact of ESG scores is greater in sectors with greater environmental materiality.

- The explanatory power of ESG scores has decreased in recent years. The likely explanation is that in late 2015 Moody’s and S&P announced they would take ESG dimensions more explicitly into consideration when determining credit ratings, thereby reducing the information content in the respective ESG scores. In 2017 Fitch followed suit.

New research

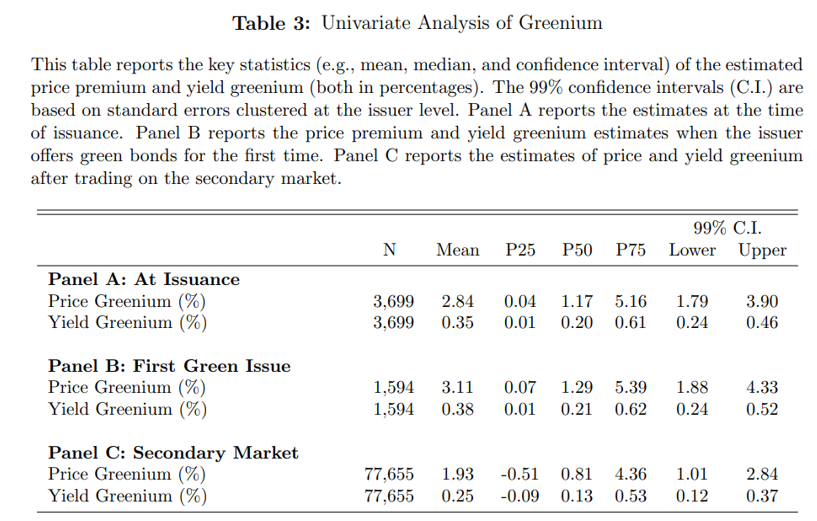

Rex Wang Renjie and Shuo Xia contribute to the sustainable investing literature with their January 2023 study, “ESG Investing Beyond Risk and Return,” in which they compared green bonds (bonds specifically earmarked to raise money for climate and environmental projects) with equivalent non-green bonds. Their data sample covered 3,699 U.S. municipal green bonds issued between June 2013 and December 2020. Here is a summary of their key findings:

- There was a “greenium” that was statistically and economically significant.

- On average, there was an offering-price greenium of 2.8% (statistically highly significant with a 99% confidence interval ranging from 1.8% to 3.9%), corresponding to a yield greenium of 35 basis points (a significant yield premium with an average of 35 basis points [bps] and a 99% confidence interval ranging from 24 to 46 bps).

- Offering greenium estimates were the highest when green bonds were issued for the first time – the average price greenium was 3.1%, and the average yield greenium was 38 bps – and were lower when issued repeatedly.

- The greenium estimates of first-time issues dropped by nearly half in the first two years after trading on the secondary market, when the average price greenium decreased to 1.9% but remained significant, corresponding to a yield greenium of 25 bps.

- The greenium decreased with the number of times a municipality had already issued green bonds prior to the current issue.

- The greenium estimates could not be explained by other bond characteristics or commonly known pricing and trading frictions in the municipal market.

- The greenium was driven by the demand from green investors – the greenium was greater when investors were less concerned about greenwashing because of third-party certifications (among green municipal bonds, the Climate Bonds Initiative [CBI] and the International Capital Market Association [ICMA] are the two primary certification providers) or better credit ratings. First green bond issues with either certification (CBI or ICMA) earned a higher offering greenium. When an issue was certified by both CBI and ICMA, its greenium was about 80 bps, more than twice as large as that of other issues (35 bps).

- The greenium was also higher when local investors became more aware of climate change and had more trust in issuers’ environmental commitment due to local environmental regulation and enforcement.

- The greenium was higher as the credit rating improved – the offering greenium was significantly positive for bonds with AAA to A ratings, but insignificant or even negative for BBB or lower ratings. The authors noted: “This pattern is consistent with our conjecture that demand from green investors is higher when investors are less concerned about greenwashing.”

Renjie and Xia hypothesized that the patterns they found “are consistent with the green halo effect, which predicts that green bond issuance signals the issuer’s environmental commitment to investors and thereby also reduces the yield of conventional bonds from the same issuer. Indeed, we find that the yield of conventional bonds from the same issuer declines by approximately 23 bps over the three years following the first green bond issuance, which explains the lower offering greenium of the repeated issues and the lower traded greenium on the secondary market. Prior research that ignores the green halo effects would therefore underestimate the greenium, especially when the green bond is a repeated issue.” They added that prior research had found: “The main incentives to issue green bonds may not be financial but rather reputation signaling. As engagement on ESG issues helps reduce issuers’ downside risk and bond yields, the signal of climate commitment from green bond issuance may also lower the yields of other outstanding conventional bonds from the same issuer. Therefore, the green halo effects predict that the yield differential between green and conventional bonds decreases over time, especially after the first green bond issues.” And finally, they noted that their findings of a significant greenium “is direct evidence that investors prefer green assets when expected risk and return are constant.”

Investor takeaways

High ESG scores have been found to lead to both higher equity valuations and lower corporate bond spreads. Thus, a focus on sustainable investment principles leads to lower costs of capital, providing companies with a competitive advantage. It also provides companies with the incentive to improve their ESG scores. In other words, through their focus on sustainable investment principles, investors are causing companies to change behavior in a positive manner. In addition, the lower cost of capital provides incentive for firms to “go green” in terms of new products and services. Also, the ESG research, including the 2020 study “Corporate Sustainability and Stock Returns: Evidence from Employee Satisfaction,” has found that improving ESG scores also improves employee satisfaction. And that too can improve corporate profitability.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article. LSR-22-453

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 am ET. Click here to register.

Read more articles by Larry Swedroe

I’ve written previously about how positive (“green”) environmental, social and governance (ESG) metrics have increased the prices of stocks, reducing their expected returns. New research examines a similar effect in bonds, where a “greenium” (lower yield on green bonds versus non-green equivalents) lowers returns for investors.

I’ve written previously about how positive (“green”) environmental, social and governance (ESG) metrics have increased the prices of stocks, reducing their expected returns. New research examines a similar effect in bonds, where a “greenium” (lower yield on green bonds versus non-green equivalents) lowers returns for investors.