The AQR Style Premia Alternative Fund (QSPIX) was introduced a decade ago to provide pure exposure to four market factors that had historically delivered excess returns. Let’s look at how it performed over that period.

The AQR Style Premia Alternative Fund (QSPIX) was introduced a decade ago to provide pure exposure to four market factors that had historically delivered excess returns. Let’s look at how it performed over that period.

Traditionally, portfolios have been dominated by public equities and bonds. The risks associated with the equity portion of those portfolios are typically dominated by exposure to market beta. And because equities are riskier than bonds, beta’s share of the risk in a traditional 60% equity/40% bond portfolio is much greater than 60%. In fact, it can be 85% or more (the shorter the bond duration, the greater the risk share of market beta). And because long-only mutual funds capture only a portion of the desired premia and leave their portfolios dominated by beta, their diversification benefits can be limited.

To provide a vehicle that provided greater diversification benefits – by increasing exposure to various risk premia with low correlations to not only market beta and bonds but each other – on October 31, 2013, AQR launched QSPIX. Being a long-short fund as opposed to long only, QSPIX can capture more of a factor’s premia. It invests across four styles (or factors), each backed by economic theory and decades of data showing long-term performance across sectors, geographies and asset classes. The key benefit is derived from the fund providing investors greater exposure to factors that have delivered premia without having any net exposure to beta (equity risk). At inception, the four styles, or sources of premia, that QSPIX captured were:

- Value: The tendency, based on historical data, for relatively cheap assets to outperform more expensive ones. It’s implemented across stocks, industries, bonds, interest rates, currencies and commodities.

- Momentum: The tendency, based on historical data, for an asset’s recent relative performance to continue in the near future. It’s implemented across stocks, industries, bonds, interest rates, currencies and commodities.

- Carry: The tendency, based on historical data, for higher-yielding assets to provide higher returns than lower-yielding assets. It’s implemented across bonds, interest rates, currencies and commodities.

- Defensive: The tendency, based on historical data, for lower-risk and higher-quality assets to generate higher risk-adjusted returns. It’s implemented across stocks, industries and bonds.

The fund accesses each style through long-short portfolios across multiple asset groups. The groups were:

- Equity indices.

- Stocks and industries: 2,000 stocks across major markets.

- Country equities: 20 countries from developed and emerging markets.

- Bonds: 10-year futures in six developed markets.

- Interest rate futures: Short-term interest rate futures in five developed markets.

- Currencies: 22 currencies in developed and emerging markets.

- Commodities: Eight commodities futures.

Target allocations

The fund accesses the four style premia across multiple groups, or asset classes. The five groups and their target risk allocations were:

- 30% equities across stocks and industries.

- 20% equity indices.

- 15% currencies.

- 20% bonds.

- 15% commodities.

This resulted in an implied style allocation that was:

- 34% value.

- 34% momentum.

- 18% defensive.

- 14% carry.

Those percentages represented the relative sources of expected return across the four style premia. While the broad strategy and the umbrella concepts have stayed the same through the decade, there have been many R&D-driven refinements over time.

Use of leverage

The fund uses leverage in targeting an annual volatility of 10%. The use of leverage is adjusted over time, adapting to market conditions. The expectation is that the fund will produce equity-like returns but with less volatility (10%) than the market. Over the long term, the average use of leverage is expected to provide investors with $3 to $4 of both long and short positions for each dollar invested.

Shortly after its introduction, the investment policy committee of Buckingham Strategic Wealth approved the use of QSPIX in client portfolios, with each client making their own decision about whether to include (and how much of) an allocation.

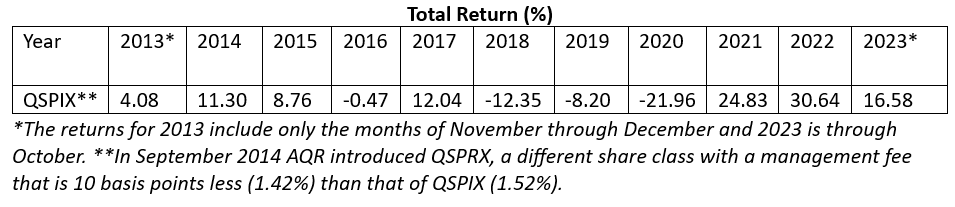

The fund was launched on October 31, September 2013. Having reached its 10th anniversary, I thought it a good time to review its performance. The table below shows the year-by-year returns.

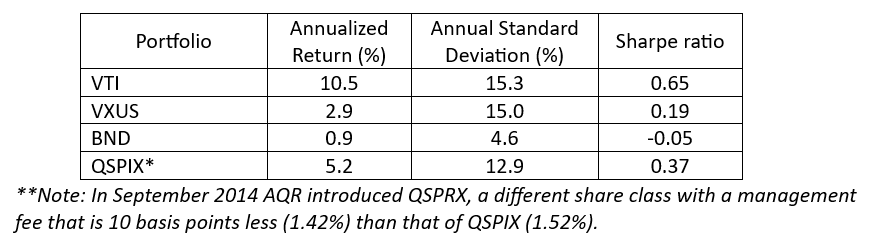

For illustrative purposes, the table below shows the 10 year annualized returns, volatility, and Sharpe ratio for QSPIX, as well as those of Vanguard’s Total Stock Market ETF (VTI), Vanguard’s Total International ETF (VXUS), and Vanguard’s Total Bond ETF (BND).

While QSPIX produced lower returns and a lower Sharpe ratio than VTI, it produced higher returns and a higher Sharpe ratio than either VXUS or BND. It also produced an annualized (compound) risk premium of 4.1% over the riskless benchmark of one-month Treasury bills. Note that the 0.37 Sharpe ratio of QSPIX over this period was virtually identical to the Sharpe ratio of the CRSP 1-10 Index (U.S. total market) of 0.36. Every investor should be interested in including in their portfolio a fund with a Sharpe ratio of about 0.4 with negative correlation to both traditional stocks and bonds.

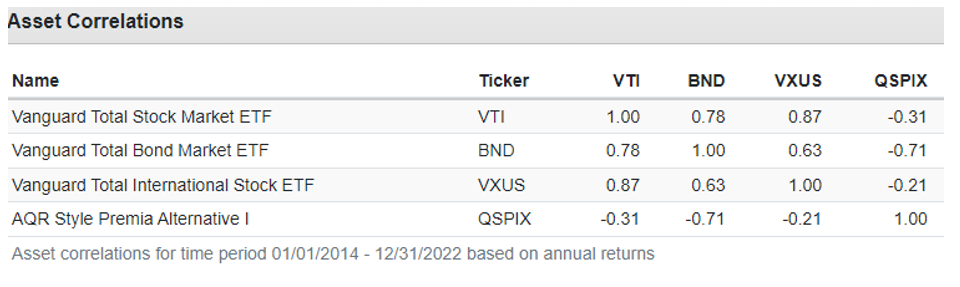

While we reviewed the fund’s performance in isolation, sophisticated investors know the only right way to view performance is how the addition of an investment impacts the risk and return of the entire portfolio. A fund can add value beyond its individual return contribution by providing unique risk exposures with low correlations to the other portfolio assets. The table below, from Portfolio Visualizer, shows the annual correlation of the four funds listed above.

The annual correlation of QSPIX to all three funds was negative—providing evidence of the diversification benefit of adding QSPIX to a balanced portfolio of stocks and bonds. I would provide examples to help with that; however, the SEC marketing rules have very strict requirements for the presentation of hypothetical back-tested portfolios because they can be abused by cherry picking of data by funds and advisors who are marketing funds versus providing educational information. If you who are interested in seeing the benefits you can use the backtest tool at Portfolio Visualizer.

Doing so will allow you to see how adding various allocations (for example, 5% or 10%) of QSPIX would have impacted the risk and return of your entire portfolio. Doing so will show you why it’s critical to avoid the mistake of judging a strategy based solely on its performance as you will likely observe an improvement in the portfolio’s Sharpe ratio and its downside risk as well. And depending on where you take the allocation to QSPIX from, its addition may also have increased the portfolio’s return.

Tracking variance risk

While back tests are likely to show that adding an allocation to QSPIX would have produced more efficient portfolios, investing in QSPIX would have come with having to bear the pain of three years of very poor performance. Its performance was negatively impacted by the largest historical drawdown for the value premium in stocks: In 2018 the fund returned -12.3%, in 2019 it returned -8.1%, and in 2020 it returned -21.9%. Only investors with the discipline to stay the course benefited from the 25.0% return in 2021, the 30.8% return in 2022, and the 15.6% return through October 2023.

Investor takeaways

The academic research, including such studies as “The Death of Diversification Has Been Greatly Exaggerated” by Antti Ilmanen and my colleague Jared Kizer, published in the Spring 2012 edition of the Journal of Portfolio Management (the study won the prestigious Bernstein Fabozzi/Jacobs Levy Award for the best article of the year) and the 2014 study by Niels Pedersen, Sebastien Page and Fei He, “Asset Allocation: Risk Models for Alternative Investments,” published in the May/June 2014 issue of the Financial Analysts Journal, has found that factor diversification has been much more effective at reducing portfolio volatility and market directionality than asset class diversification. The to-date performance of QSPIX supports that finding.

Another important takeaway is that all strategies that entail investing in risk assets (including QSPIX) are virtually guaranteed to experience long periods of underperformance. If you doubt that, consider that the S&P 500 Index (which is basically exposure to market beta and nothing else) has experienced three periods of at least 13 years when it underperformed riskless one-month Treasury bills (1929-43, 1966-82 and 2000-12). That means that to gain the benefits of diversifying away from traditional 60/40 portfolios, you must have the discipline to stay the course (and even rebalance) during periods of negative performance.

Sadly, it’s my experience that when it comes to judging investment performance, investors think three years is a long time, five years is a very long time, and 10 years is an eternity. Financial economists know that when it comes to risk assets, 10 years is likely nothing more than noise – or the risks show up for which you are compensated with an expected, but not guaranteed, premium. If the premium were guaranteed, there would be no risk (and no premium). Investors who lack this understanding tend to abandon even well-thought-out strategies after a few years of underperformance. They fail to understand that underperformance typically results in much more favorable valuations, and, thus, higher future expected returns.

The research on investor behavior has found that retail investors tend to underperform the very funds they invest in because they buy after periods of strong performance (when valuations tend to be high and expected returns low) and sell after periods of poor performance (when valuations tend to be low and expected returns high). In their 2023 study, “Mind the Gap,” Morningstar found that over the 10-year period ending in 2022, the average investor underperformed the funds they invested in by 1.7 percentage points per annum, losing about 20% of the available returns. The behavioral challenges to maintaining exposure to those premia are one reason they are likely to persist.

To gain the diversification and risk-reduction benefits of investing in uncorrelated assets such as QSPIX, you must be willing to have a portfolio that will perform very differently than that of the traditional market portfolio. It will be easy to stay the course when the strategy outperforms, as it did in 2021 and 2022 and through October 2023, but it will be much harder to do so when it underperforms. Sophisticated investors, such as the Yale and Harvard endowments, understand this, allocating as much as 40% or more to alternatives, including illiquid ones (QSPIX is liquid).

On a final note, the spread between valuations of growth and value stocks is back to only the mid to high 80th percentiles, while equity markets are still quite expensive. Thus, the recent strong performance of QSPIX seems likely to be a partial (relative and absolute) recovery, with more likely to come.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners, collectively Buckingham Strategic Wealth, LLC and Buckingham Strategic Partners, LLC.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Information from sources deemed reliable, but its accuracy and completeness cannot be guaranteed. Investors should carefully consider any fund investment risks and investment objectives. Certain funds may not be appropriate for all investors and are not designed to be a completed investment program. As such, this article does not constitute a recommendation to purchase a specific security and it should not be assumed that the securities referenced herein were or will prove to be profitable. No strategy assures success or protects against loss Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal. Individuals should speak with their qualified financial professional based on their own circumstances to discuss the ideas presented in this article. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth, LLC or any of its affiliates.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more articles by Larry Swedroe

The AQR Style Premia Alternative Fund (QSPIX) was introduced a decade ago to provide pure exposure to four market factors that had historically delivered excess returns. Let’s look at how it performed over that period.

The AQR Style Premia Alternative Fund (QSPIX) was introduced a decade ago to provide pure exposure to four market factors that had historically delivered excess returns. Let’s look at how it performed over that period.