New research shows that the tightening of bank lending standards – as is the case now – has led to stock-market underperformance. But with banks playing a smaller role in corporate finance, that finding has lost some relevance.

New research shows that the tightening of bank lending standards – as is the case now – has led to stock-market underperformance. But with banks playing a smaller role in corporate finance, that finding has lost some relevance.

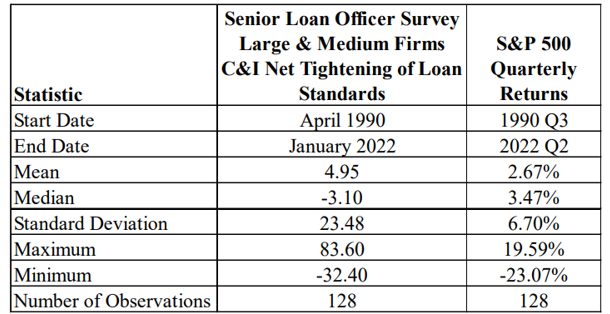

In April 1990, the Senior Loan Officer Opinion Survey on Bank Lending Practices added the following survey item: “Net Percentage of Domestic Banks Tightening Standards for Commercial and Industrial Loans to Large and Middle-Market Firms, Percent, Quarterly, Not Seasonally Adjusted.” It is often called the “loan standards” question. A positive reading means that credit conditions are tightening for large and middle-market firms; a negative reading means credit conditions are lowering for those firms. Typically, the Senior Loan Officer Survey is released a month or two prior to the start of the next quarter.

A 2006 Federal Reserve Bank of Atlanta study found that credit-standard tightening shocks were associated with substantial declines in output and in the capacity of businesses and households to borrow from the banking sector, as well as a sharp widening of credit spreads. The result was that GDP growth declined significantly within two quarters. For example, there was a sharp and sudden reduction in the availability of credit at the time of the Long-Term Capital Management (LTCM) crisis in the early autumn of 1998. A similar pullback in the supply of bank loans occurred immediately before the economic downturn in 2001 and before and during the early phases of the great recession.

The 2012 study, “Changes in Bank Lending Standards and the Macroeconomy,” found that “an adverse loan supply shock of one standard deviation is associated with a decline in the level of real GDP of about 0.75 percent two years after the shock, while the capacity of businesses and households to borrow from the banking sector falls almost 4 percent over the same period. This shock also leads to a substantial rise in private credit spreads.” Eventually, the economic effects of the deterioration in the supply of credit elicit a significant easing of monetary policy.

The empirical research demonstrates that changes in bank lending standards informed future economic growth. An interesting question is whether the changes also informed future stock returns. Linus Wilson sought the answer to that question in his January 2023 paper, “Profitable Timing of the Stock Market with the Senior Loan Officer Survey,” in which he analyzed if the release of the survey was predictive of S&P 500 stock returns over the following quarter. This was a particularly timely question, as the April 2023 survey found that over the first quarter:

- Significant net shares of banks reported having tightened standards on commercial and industrial loans to firms of all sizes.

- Major net shares of banks reported tightening standards for all types of commercial real estate loans.

- Lending standards tightened for most residential real estate loan categories and for home equity loans.

- Significant net shares of banks reported having tightened lending standards for credit card, auto and other consumer loans.

As to why banks were tightening credit standards, they frequently cited concerns regarding their liquidity positions, deposit outflows, funding costs, concern for the economic outlook, deterioration of collateral values and deterioration in credit quality of their loan portfolio.

Wilson’s data sample spanned the period April 1990-January 2022 for the survey and July 1990-June 2022 for the S&P 500.

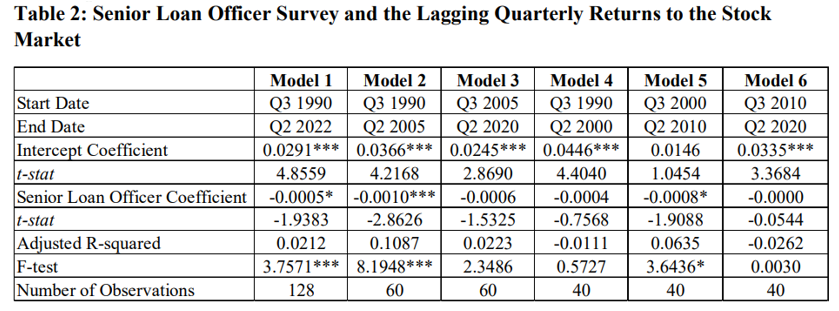

Wilson then tested six different time periods: the full sample of 128 quarters, the first 60 quarters (15 years), the second 60 quarters, the first 40 quarters (10 years), the second 40 quarters, and the third 40 quarters in models 1, 2, 3, 4, 5 and 6 respectively. Following is a summary of his key findings:

- In all models, tightening loan standards was associated with lower stock returns.

- The data was negative and significant only in models 1 (full sample), 2 (first 60 quarters), and 5 (second 40 quarters).

- In models 1 and 5, the full sample and 10-year period 2000-2010, the data was only significant with 90% confidence.

Having only 40 data points is a small sample size. Thus, it is not surprising that the data was not significant in two out of three of the 40-quarter subsamples. With that said, Wilson’s findings are a clear violation of the efficient market hypothesis – even the semi-strong version (security prices have factored in publicly available market data, and price changes to new equilibrium levels are reflections of that information). But it’s also possible that the lack of significance of the standards coefficient in the last 10-year period reflected market participants learning and considering the information from the survey.

Wilson then built a simple model that attempted to benefit from the signals from the loan officer survey:

- R1 was the expected return of the S&P 500 next quarter taken from the alpha model.

- R1 = a + b SLOt-1 = 0.0366 – 0.0010 SLOt-1 where the coefficients were taken from model 2 in Table 1, and SLOt-1 was the most recent reading of the Senior Loan Officer survey.

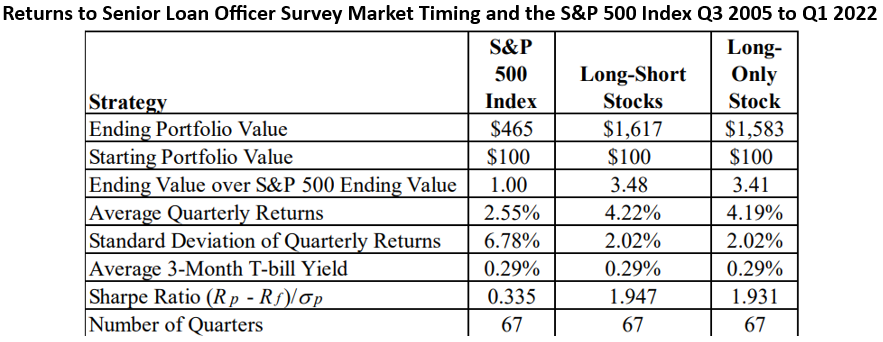

Wilson then tested the model, designed to have the same variance as the S&P 500, over the period Q3 2005-Q1 2022. The model moved its equity allocation depending on the strength of the signal. He found:

- Over the period Q3 2005-Q1 2022, the Sharpe ratios of the out-of-sample market timing long-only and long-short portfolios were more than 1.9, over five times better than a passive investment in the S&P 500, with a Sharpe ratio of 0.335.

- Despite the risk-model ex ante limiting the standard deviation of the portfolio to that of the stock market, the realized quarterly volatility was just 2.02% compared to the quarterly volatility of 6.78% for the S&P 500 indexing strategy.

Wilson’s findings led him to conclude that the loan standards question in the Fed’s Senior Loan Officer Survey was a significant predictor of the S&P 500’s quarterly stock returns and that an asset manager could put on stock trades a month or two after the survey is released and earn abnormal returns with reduced volatility.

Investor takeaways

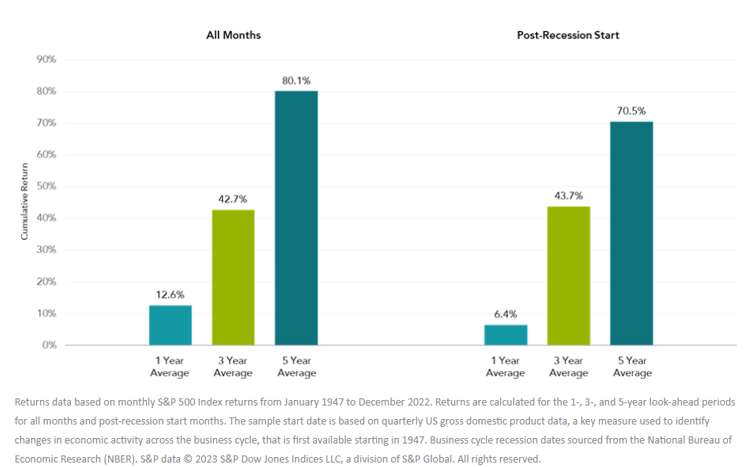

Economists have long known that tightening of credit conditions foreshadows weaker economic growth, increasing the likelihood of a recession. But the empirical evidence, as seen in the table below, shows that average U.S. equity returns have been positive after the onset of a recession.

That returns have been positive and similar in both sets of data is consistent with the theory that markets are forward looking. Even with the benefit of hindsight, and ignoring expenses and taxes, there isn’t much evidence to support a timing strategy based on a recession forecast. With that said, Wilson showed that tightening conditions also had predictive value for future stock returns.

Investors already concerned about the high valuations of broad market indices (such as the S&P 500) and the increasing risks of recession (as signaled by the yield curve inversion and the Conference Board Leading Economic Index® for the U.S. declining 0.6% in April 2023 for the 13th consecutive month) might be considering lowering their equity allocation or getting out of stocks altogether based on Wilson’s findings.

Before jumping to that conclusion, consider that the literature shows that publication of research on future stock returns led to a decline in premium returns, or even elimination (if there is no risk-based explanation for the abnormal returns). Wilson’s findings are now public, bringing into question their future value.

Since the great recession, there has been a dramatic shift in the credit markets, with private credit stepping in and taking significant market share, replacing banks as lenders to smaller and midsize businesses. Private credit has grown quickly, hitting $1.4 trillion of assets under management globally at the end of 2022, up from about $500 billion in 2015, putting it on par with the U.S. junk bond market. Thus, the fact that banks are tightening credit standards might not have the same effect on the economy going forward as it has in the past. Investors are best served by having a well-thought-out plan that includes not taking more risk than they have the ability, willingness and need to take and then staying the course. On the other hand, if an investor has been overly aggressive in their equity allocation, or if the fear of missing out (FOMO) causes them to consider raising it, Wilson’s findings might provide enough “ammunition” to convince them to reconsider, if it is appropriate to their unique situation.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed adequacy of this article. LSR-23-523

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

More Real Estate Topics >

New research shows that the tightening of bank lending standards – as is the case now – has led to stock-market underperformance. But with banks playing a smaller role in corporate finance, that finding has lost some relevance.

New research shows that the tightening of bank lending standards – as is the case now – has led to stock-market underperformance. But with banks playing a smaller role in corporate finance, that finding has lost some relevance.

Wilson’s findings led him to conclude that the loan standards question in the Fed’s Senior Loan Officer Survey was a significant predictor of the S&P 500’s quarterly stock returns and that an asset manager could put on stock trades a month or two after the survey is released and earn abnormal returns with reduced volatility.

Wilson’s findings led him to conclude that the loan standards question in the Fed’s Senior Loan Officer Survey was a significant predictor of the S&P 500’s quarterly stock returns and that an asset manager could put on stock trades a month or two after the survey is released and earn abnormal returns with reduced volatility.