A Case Study of How Recency Bias Destroyed Investor Wealth

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits The investor’s chief problem – and even his worst enemy – is likely to be himself.

The investor’s chief problem – and even his worst enemy – is likely to be himself.

- Benjamin Graham

Many investors are performance chasers, tending to buy (high) a fund after a period of good performance and tending to sell (low) after a period of poor performance. This results from the behavioral error known as recency bias – one of the 77 errors discussed in my book, Investment Mistakes Even Smart Investors Make and How to Avoid Them. Recency bias is the tendency to overweight recent events/trends, projecting them into the future, while ignoring long-term evidence.

Buying after periods of strong performance (when valuations are higher and expected returns are now lower) and selling after periods of poor performance (when valuations are lower and expected returns are now higher) is not a prescription for successful investing. Yet, because of recency bias, it is the way many individuals invest. What disciplined investors do is the opposite – rebalance to maintain their well-thought-out allocation to risky assets.

Sadly, while most investors consider three years a long time to judge performance, five years a very long time and 10 years an eternity, wise investors know that all risk assets go through even much longer periods of underperformance. Consider that the S&P 500 Index underperformed riskless one-month Treasury bills over the 13-year period ending 2012, the 15-year period ending 1943 and the 17-year period ending 1982. Of course, over the succeeding periods, stocks went on to produce spectacular returns – those that were earned only by staying the course.

The Stone Ridge Reinsurance Risk Premium Interval Fund (SRRIX) – one of the first ’40 Act funds providing access to the asset class of catastrophe reinsurance – provides a good case study. As an asset that is totally uncorrelated to the risks of traditional stocks and bonds, and with more than 150 years of providing a significant risk premium to investors, catastrophe reinsurance is an attractive asset class. The fund’s inception was December 9, 2013. In the first month, it lost 0.10%. Over the first three years, the fund returned 11.0% (2014), 7.90% (2015) and 6.38% (2016). Given that T-bill yields were virtually zero, the fund provided investors with a large risk premium. As you would expect given those returns, cash flows into the fund were strong – assets under management at SRRIX had grown from about $600 million at the end of 2013 to more than $4.2 billion at the end of 2016 and $5.7 billion at the end of 2017.

Stone Ridge made this fund available only to registered investment advisors (RIAs) who agreed to attend a two-hour training session about the fund. Central to the training was ensuring that each RIA would advise their clients to maintain their allocation to the asset class even after losses from catastrophic events. Stone Ridge told the RIAs: “If you think your clients are going to redeem after losses, then this is not the right asset class for them.” Every RIA that invested affirmed that they understood this and that their clients would stay the course.

Then came a string of losses starting in 2017. SRRIX lost -11.35% in 2017, -6.14% in 2018 and -4.47% in 2019 due to more-than-expected hurricanes, wildfires and typhoons. And despite the RIAs’ assurances that their clients would stay the course, cash outflows followed those losses – recall that many, if not most, investors consider three years a long time to judge performance.

As an interval fund, SRRIX is required to redeem a minimum of 5% of assets each quarter – 20% a year. The fund’s management made efforts to return substantially more than the minimum, allowing some of its reinsurance trades to expire. However, because of the limitations, many investors were unable to redeem all their shares for a period of time (although they often got back about 90% within a year). And while 2020 was a better year, as SRRIX returned 6.79%, the fund continued to experience net redemptions. The redemption trend continued when SRRIX returned -6.47% in 2021. And it continued in 2022 despite the fund returning 5.10% while the S&P 500 was down -18.13%, the Nasdaq was down -32.51% and the S&P Aggregate Bond Index was down -12.03%. At that point, SRRIX had produced positive returns in two of the last three years. And despite the fund returning 8.07% in the first quarter of 2023, the redemption trend continued. The result was that the fund’s assets under management had fallen about 80% from its $5 billion peak to less than $1 billion by the end of 2022. The RIAs that remained invested in SRRIX through these losses were able to help their clients maintain investing discipline through the psychological tough times.

Like all asset classes, reinsurance has experienced some periods of poor performance, as it did in 2004-2005 when there were seven major (category 3 or stronger) hurricanes that made landfall in the U.S. Those years led to reinsurance premiums rising dramatically, and reinsurance produced some of its strongest returns ever over the next 11 years because not a single major hurricane made landfall in the U.S. Armed with the historical evidence, investors should have been well prepared for reinsurance eventually experiencing another period of poor returns and been able to “weather the storm” and stay disciplined, rebalancing their portfolio and thus selling after years of strong performance and buying after years of poor performance. However, that is not the way most retail investors act – their behavior is fueled by recency bias.

Sadly, recency bias causes investors to lose sight of some simple facts. Consider that when stocks experience severe bear markets, it is mostly because the equity-risk premium demanded by investors rises dramatically. That causes valuations to fall sharply. And valuations are the best predictor we have of future real returns. Thus, lower valuations predict higher future returns.

Valuations matter

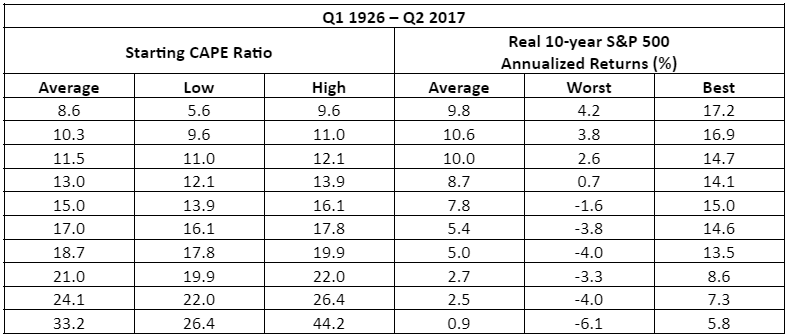

In their 2017 paper, “The Many Colours of CAPE,” Robert Shiller and Farouk Jivraj found that the CAPE 10 was a better predictor than any of the alternatives considered, and it provided valuable information. As seen in the table below, they found that 10-year-forward average real returns dropped nearly monotonically as starting Shiller P/Es increased. They also found that as the starting Shiller CAPE 10 ratio increased, worst cases became worse and best cases became weaker. Additionally, they found that while the metric provided valuable insights, there were still very wide dispersions of returns. In other words, there are no guarantees. While low valuations forecast high expected returns, investors can still experience the left tail of the distribution that results in losses. And while high valuations forecast low expected returns, investors can still experience the right tail of the distribution that results in strong returns.

Reinsurance provides a similar type of signal about potential future returns. When reinsurers experience losses, they not only demand greater risk premiums but typically seek greater protections in the form of tougher underwriting standards. For example, a home might be required to meet stronger construction standards to obtain wind insurance, and trees might need to be cleared from the home by at least 30 feet to get fire insurance. Further, reinsurance companies might insist on higher deductibles for the same premium, reducing risk. This is exactly what has happened.

At its inception, the net of expenses “no loss return” (a yield equivalent of the fund if there were no natural catastrophes in a year, which is unrealistic) was about 13% and the more realistic modeled (50th percentile) return to investors was about 7%. As capital fled, the no-loss and the modeled returns have been persistently rising. As of February 2023, the no-loss return for SRRIX was in excess of 30%, and the 50th percentile modeled return was over 20%. Given this elevated risk premium, SRRIX has already produced a higher return (8.67%) this year (through April 6, 2023) than in any other full year of the fund except 2014. Of course, just as low equity valuations don’t eliminate the risk of losses, the worst 1-in-25-year models to a loss of about -20%, and worse losses are possible. In other words, there is no risk premium without risk.

Investor behavior

With knowledge of the history of the reinsurance industry and how premiums and thus expected returns react to periods of losses, investors should have had the discipline to stay the course instead of allowing recency bias to cause them to sell. Instead, they withdrew billions of dollars from the fund. How did that affect their returns? Thanks to Stone Ridge, we know the answer. From inception through March 31, 2023, while the time-weighted return earned by SRRIX was 1.49%, the dollar-weighted return to investors in the fund was -1.50% – recency bias resulted in a gap between the returns earned by the fund and the returns investors earned of -2.99%. And that figure has grown, through April 6, the fund had returned almost 9% in 2023.

Investor takeaways

Resisting recency bias is the key to earning the premiums available from all risky assets, including reinsurance. Wise investing, as Warren Buffett noted, is simple but not easy. That’s because of all the behavioral biases investors must overcome, with recency among the most powerful. It’s tempting to sell out of an investment that has suffered losses because it’s easy to think losses will keep happening. It’s even more tempting when the media keeps telling us that climate change is responsible for the losses (as it did after 2004-05, which was followed by perhaps the most profitable 11 years ever for the industry). But it is not a prudent strategy to decide to get out of reinsurance immediately after losses – an investor has taken the losses but hasn’t gotten the benefit of increased premiums and reduced risks (from tougher underwriting standards and increased deductibles). Because premiums adjust on an annual basis, investors need to have a long horizon to realize the true economics of the asset class.

As with any long-term risk premium, the evidence demonstrates that it’s highly unlikely investors can time entry and exits because it’s simply not possible to know when losses will occur. Getting out of reinsurance now would be the classic “buy high/sell low” strategy – like exiting equities in March 2009 or exiting value stocks in 1999. It’s not easy to help investors stay the course, but doing so is a big part of the value advisors provide.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners.

The opinions expressed here are their own and may not accurately reflect those of Buckingham Wealth Partners or its affiliates. For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Mentions of specific securities should not be construed as a recommendation. Reinsurance funds have unique risk characteristics including liquidity risk and may be subject to large swings in returns. Individuals should speak with a qualified financial professional about the risks associated with the above-mentioned asset class before potentially implementing them in their portfolio. Past performance is not indicative of future returns. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. Buckingham is not affiliated with Stone Ridge. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article. LSR-23-484

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All