As we enter the brunt of hurricane season, there are signs of three financial calamities merging to form the perfect storm. The nexus is in commercial real estate, but it extends to banking and the broader economy.

As we enter the brunt of hurricane season, there are signs of three financial calamities merging to form the perfect storm. The nexus is in commercial real estate, but it extends to banking and the broader economy.

The three elements of the perfect storm are as follows:

1. The devastation of the office real estate market

The first storm began in early 2020 as COVID hit and people started working from home, leaving some office buildings vacant. While we have learned to live with COVID, employees have been reluctant to return to the office, at least full-time. A recent article by Larry Swedroe revealed office vacancy rates average roughly 50% in major U.S. cities. Other data is not so dire, with Statista showing national vacancy rates just over 16%. Even that, however, is significantly higher than pre-pandemic levels.

Higher vacancy rates hurt real estate cash flows in two ways. Rents are generally not paid on vacant space, but costs remain fixed. Second, higher vacancy rates bestow more negotiating power upon tenants as landlords give larger discounts to try to fill the vacancies. Additionally, many tenants are attempting to sublet their excess space.

2. Surging interest rates

Last year, 2022, was the worst year ever in the bond market as interest rates surged. In fact, statistically speaking, the bond market last year was the equivalent of the stock market plunge during the Great Depression.

This impacts the commercial real estate market in two ways. Cap rates are significantly higher, which is another way of saying those ever-decreasing cash flows from higher vacancies are now discounted at a much higher rate, lowering the present value and market price of buildings. Second, those with either variable loans or loans that come due soon will be paying a much higher cost to service that debt.

A recent example of these two storms having already merged was in an article in The Wall Street Journal, “Fire Sale: $300 Million San Francisco Office Tower, Mostly Empty. Open to Offers.” The building, at a prestigious address on California Street, might sell for 20% of the $300 million it was worth back in 2019.

3. The debt bomb

Unlike the first two storms, this one is only beginning to form, though conditions indicate it will be the worst of the three. Combined with the first two, it is predicted to cause major damage to the entire economy. Bloomberg reports a $1.5 trillion wall of debt is looming for U.S. commercial properties. That is the amount of debt that will come due and must be refinanced before the end of 2025.

Further, much of this debt is owned by smaller local and regional banks which saw huge amounts of deposits flee to the too-large-to-fail money-center banks earlier this year. If those banks are stressed, it’s reasonable to assume the same thing would happen as this debt bomb explodes. One expert, who requested anonymity, told me many regional banks would be underwater if they had to mark down the value of those commercial-property, real-estate loans to market. Those loans would need to be discounted considering the collapse of the value of the underlying properties.

Assessing the potential damage

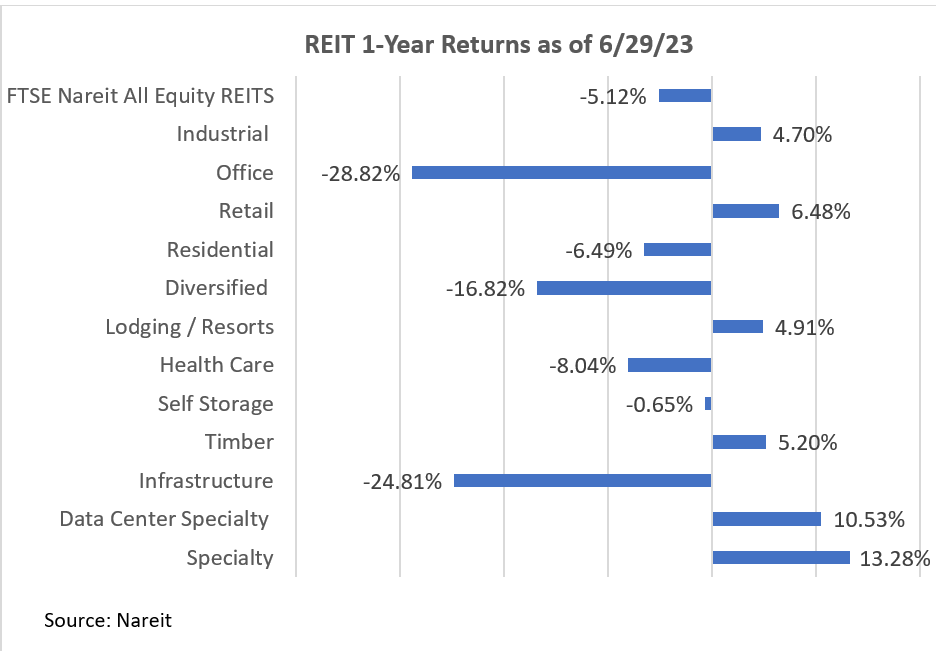

How much damage will be done is not clear. The worst of the storm should be over by 2025 as more than half of commercial debt will have come due by then. Since markets are forward looking, an indication can be seen in publicly held REITS. Office REITs make up only about 23% of the commercial real estate, according to NAREIT, a trade organization representing the REIT industry. Not surprisingly, for the year ending June 29, 2023, office REITS were the worst performing sector, losing nearly 29% of their value. REITs lost 5.12%, though some sectors showed gains.

By comparison, the overall U.S. stock market (as measured by the total return of the Wilshire 5000) gained 16.61% over the past year. So, the market barometer readings indicate REITs underperformed the stock market by 21.73 percentage points and office REITs underperformed by 45.43 percentage points. Stock market returns, however, were driven by ultra-large-cap-growth companies, particularly tech.

Some sectors of commercial real estate are up, such as industrial, retail, lodging and resorts, timber, data centers, and specialty. Though it would be a mistake to say the entire commercial real estate market is in peril and the $1.5 trillion refinancing by 2025 is stressed, the 23% in office space clearly will be a hit. It’s just a question of how bad a hit and whether it will take down weaker banks along with it.

One possibility that could mitigate the damage is whether companies will be successful in getting employees to return to the workplace. According to the Bureau of Labor and Statistics, 34% of Americans work from home now, up from 25% in 2019. The study also showed those who work from home put in an average of 5.4 hours a day versus 7.9 hours for those who work in the office. Companies have the incentive to get workers to return to the office.

There has been fierce resistance from employees, and companies have less leverage to press the issue with unemployment so low. But a recession could change that, and this debt bomb could be at least part of the reason we have such a recession.

Fed Chair Jerome Powell said in a March 22, 2023 press conference, “We’re well aware of the concentrations people have in commercial real estate.” He reiterated, “The banking system is strong, it is sound, it is resilient, it’s well capitalized.” Kevin Fagan, director of commercial real estate analysis at Moody’s Analytics, said, “There likely will be issues but it’s more of a typical down cycle.” Of course, credit rating agencies completely missed the risk of collateral debt obligations during the 2008 real estate crisis.

What to do

I’m extremely concerned about this debt bomb. It will be difficult to get employees to return to the office, even with higher unemployment. But this upcoming refinancing is not comparable to the 2008 real estate bubble that led to the financial crisis. This is one part of one sector of the real estate market, and the stock market has already reacted to this issue as shown by the losses in sectors of REITs. If the debt bomb coincides with other economic downturns, however, this could prove an even more serious problem.

The time to sell REITs, particularly office REITs, has passed. This doesn’t mean they won’t lose more – merely that the market has already reacted to forecasts of this debt bomb. I’m advising clients to stick with their plan. If I’m wrong and stocks plunge as this causes yet another financial crisis, then I’ll have clients rebalance and buy more stock index funds to get back to their target allocation. With stocks in bull territory, clients should be selling to rebalance so any debt bomb will merely mean they will be buying it back at a lower price.

Capitalism will survive. In the last 15 years, we have survived what could have been the collapse of the financial system as well as a global pandemic. We will survive high office vacancy rates, surging interest rates, and the debt bomb.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth

As we enter the brunt of hurricane season, there are signs of three financial calamities merging to form the perfect storm. The nexus is in commercial real estate, but it extends to banking and the broader economy.

As we enter the brunt of hurricane season, there are signs of three financial calamities merging to form the perfect storm. The nexus is in commercial real estate, but it extends to banking and the broader economy.