The performance of private-equity (PE) funds has been disappointing. New research explains why this happened: Instead of driving operational efficiencies (as PE investors typically claim they do), those funds relied heavily on increasing the debt burden for the companies they bought.

The performance of private-equity (PE) funds has been disappointing. New research explains why this happened: Instead of driving operational efficiencies (as PE investors typically claim they do), those funds relied heavily on increasing the debt burden for the companies they bought.

Attracted by the glamour and potential for lottery-like returns, global private equity (PE) assets under management reached $4.2 trillion in 2022. PE involves pooling capital to invest in private companies either in the form of providing venture capital (VC) to startups or by taking over and restructuring mature firms via leveraged buyouts (LBOs). PE investors believe that the benefits outweigh the challenges not present in publicly traded assets – such as complexity of structure, capital calls (and the need to hold liquidity to meet them), illiquidity, higher betas than the market, high volatility of returns (the standard deviation of private equity is in excess of 100%), extreme skewness in returns (the median return of PE is much lower than the mean), lack of transparency and high costs. Other challenges for investors in direct PE investments include performance-reporting data, which suffer from self-report bias and biased NAVs, which understate the true variation in the value of PE investments.

Another important challenge for PE investors is understanding the drivers of returns. The PE industry touts its ability to create operational efficiencies in the companies they acquire, thereby increasing valuations. Is this fact or marketing hype? To attempt to answer that question, the research team at Verdad analyzed a sample from S&P’s Capital IQ of 993 PE deals from 1996 to 2021 in which both preacquisition and post-acquisition financials were publicly disclosed as a result of public-debt issuance. While 993 deals is admittedly a small sample of the total number of transactions (in the last decade, there were about 5,000 to 10,000 deals per year, while its database included only 16-105 deals per year), its data set captured a meaningful percentage of the largest deals: The average revenue of a company in the dataset was $760 million, average EBITDA was $96 million, and most of the big headline-making deals like Dell, Staples and Toys “R” Us were included.

To determine if PE acquirers created operational efficiencies or achieved gains due to changes in capital structure (increased use of leverage) – or some combination of both – Verdad analyzed six key metrics in the three years before and after the deal (buyout holding periods are about three years on average). They then compared their data to the aggregate metrics for public companies in the same sector in the same year. Following is a summary of their findings:

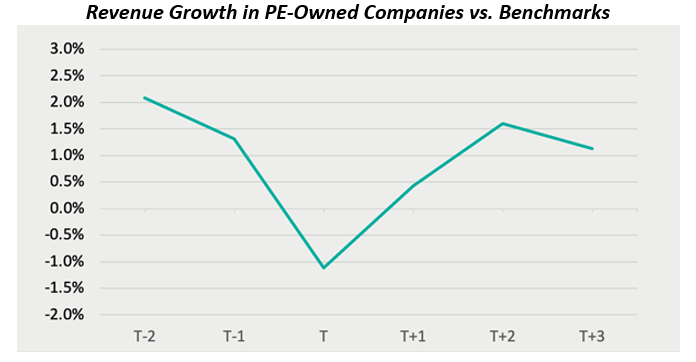

- Revenue growth: PE firms tended to target companies outperforming their industries. Revenue growth was on average 1.7% above industry standard in the two years before the deal. But in the three years after the deal, revenue growth was on average only 1.1% above industry standard, 60 basis points lower than preacquisition. Verdad hypothesized that major LBO transactions were distracting to management and led to suboptimal outcomes from a sales and margin perspective during the deal year.

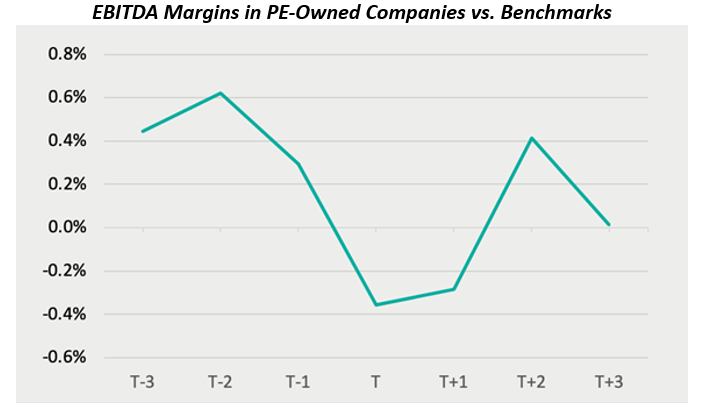

- Earnings before interest, taxes, depreciation and amortization (EBITDA) margin: PE firms tended to target companies outperforming their industries. EBITDA margin was on average 0.5% above industry standard in the three years before the deal. In the three years after the deal, EBITDA margin averaged out to exactly the industry standard, 50 basis points lower than preacquisition.

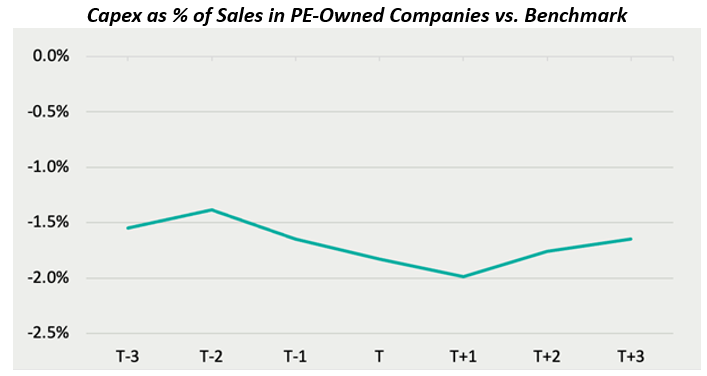

- Capital expenditure (capex) as a percentage of sales: Given their high use of financial leverage, PE firms tended to acquire companies with lower capex/sales than industry averages. After acquisition, capex spending decreased marginally relative to preacquisition.

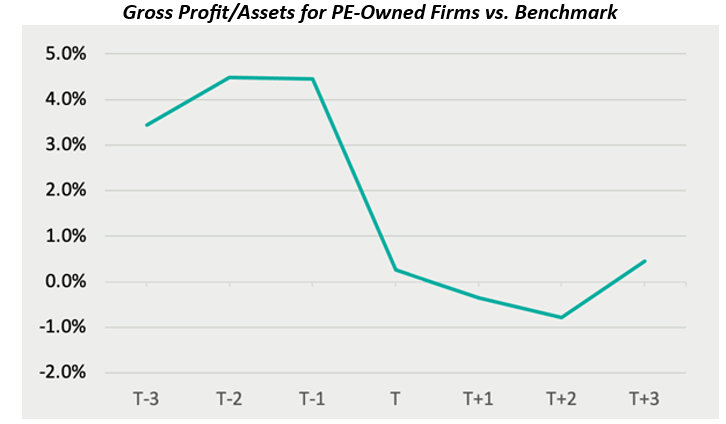

- Gross profit to total assets: At the time of the deal, gross profit/assets dropped sharply at the time of the deal. But the spike down was explained by the write-up in total assets on the balance sheet caused by the incorporation of goodwill. Post deal, however, companies that looked to be higher than industry benchmarks in terms of profitability and return on assets came almost perfectly in line with sector benchmarks – PE firms were paying a full price for the higher-quality companies they were buying.

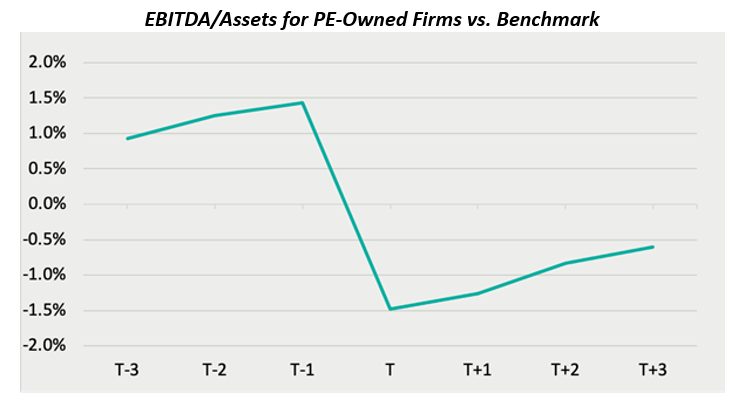

- EBITDA-to-total assets: It followed the same pattern as gross profit to total assets – EBITDA dropped sharply at the time of the deal, with the spike down explained by the write-up in total assets on the balance sheet caused by the incorporation of goodwill. Post deal, companies that looked to be higher than industry benchmarks came in line with sector benchmarks.

Summarizing its findings, Verdad observed: “Revenue growth and margins do seem marginally better than sector benchmarks, but this does not appear to be a result of the transaction or any systematic operational improvements. Instead, PE firms appear to be buying slightly higher-performing companies that then experience some mean reversion post-acquisition.” In terms of capex, they added: “We see no evidence of a major change in strategy post-acquisition, no evidence that private equity is systematically investing dramatically more or dramatically less on average.”

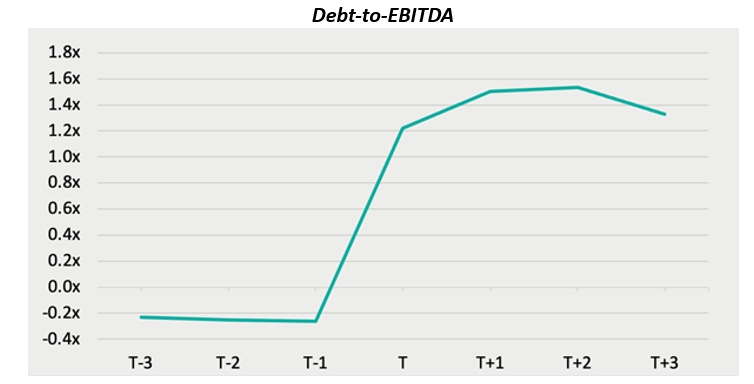

Having analyzed revenue growth, EBITDA margins, capex spending and return on assets and observing no evidence for systematic operational improvements in PE-owned firms (PE firms don’t seem to grow businesses faster, invest more in growth or gain much operational efficiency), Verdad examined the ratio of debt to EBITDA to determine what was going on.

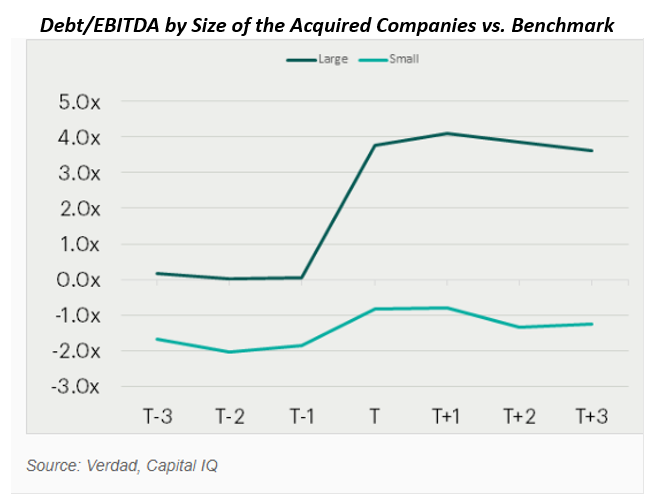

- Debt-to-EBITDA: PE firms were leveraging up the businesses they bought and not significantly deleveraging in the years post acquisition.

Verdad also found that although both large and small companies experienced an increase in debt-to-EBITDA relative to the benchmark at the time of the deal, this increase was much bigger for larger companies.

Following are other findings of interest:

- Smaller companies tended to have lower margins than the industry average, while larger companies tended to have higher margins. But the trend for both was roughly similar, with no big differences before and after acquisition.

- Perhaps surprisingly, larger companies tended to grow EBITDA at a faster rate than smaller companies.

- In terms of EBITDA growth, smaller companies appeared to benefit more from PE management than larger companies.

- More expensive deals required significantly more leverage than cheaper deals.

- There was no noticeable trend in EBITDA growth by sector after acquisition, with growth quickly reverting to benchmark for all sectors.

- In the year of the transaction, the top-PE funds (KKR, Apollo, The Carlyle Group, Bain Capital, J.P. Morgan, TPG Capital, Apax Partners, Blackstone, Clayton Dubilier & Rice, CVC Capital and Madison Dearborn) leveraged their companies more than the other companies in the database. “This could be because the top PE firms tend to invest in larger companies, which tend to be leveraged more than small companies. Median transaction value for the top PE funds amounted to $1.6B, compared to $335M for all PE funds.” They also tended to buy companies with higher margins, making the case that the larger private equity firms can buy higher quality businesses.

Their findings led Verdad to conclude: “The real reason PE firms want control of the companies they buy is not because of superior strategic insight but because they want to significantly leverage them. Our sample is obviously not sufficient to say this is true of all PE firms, but we believe it’s representative enough to be able to justify significant skepticism of any claims of operational improvements being a major contributor to PE’s performance relative to public markets.”

Are the empirical research findings consistent with those of Verdad?

Empirical research findings on private equity performance

My September 12, 2019, article for Advisor Perspectives provided a summary of the research on the performance of private equity. Unfortunately, it was not encouraging – in general, private equity has underperformed similarly risky public equities even without considering their use of leverage and adjusting for their lack of liquidity. But the authors of the 2005 study, “Private Equity Performance: Returns, Persistence, and Capital Flows,” offered some hope. They concluded that private equity partnerships were learning – older, more experienced funds tended to have better performance – and there was some persistence in performance. Thus, they recommended that investors choose a firm with a long track record of superior performance.

The most common interpretation of persistence has been either skill in distinguishing better investments or in the ability to add value post investment (e.g., providing strategic advice to their portfolio companies or helping recruit talented executives). Verdad’s work showed a lack of evidence supporting either hypothesis. But the research does offer another plausible explanation for persistence: Successful firms are able to charge a premium for their capital.

Robert Harris, Tim Jenkinson, Steven Kaplan and Ruediger Stucke confirmed the prior research findings of persistence of outperformance in their November 2022 study, “Has Persistence Persisted in Private Equity? Evidence from Buyout and Venture Capital Funds.” But it was only true for venture capital (not the full spectrum of private equity), as they found that there was no persistence of outperformance in buyout firms.

Investor takeaways

Verdad’s findings demonstrated that PE firms were buying quality companies and leveraging them, permanently changing the capital structure of their companies. But the hyped efficiency and cost-cutting simply didn’t show up in the numbers.

The late David Swensen, legendary chief investment officer of Yale’s endowment fund, offered this caution on private-equity investing: “Understanding the difficulty of identifying superior hedge fund, venture capital and leveraged buyout investments leads to the conclusion that hurdles for casual investors stand insurmountably high. Even many well-equipped investors fail to clear the hurdles necessary to achieve consistent success in producing market-beating, active management results. When operating in arenas that depend fundamentally on active management for success, ill-informed manager selection poses grave risks to portfolio assets.”

Those who choose to ignore Swensen’s warnings still need to understand that, due to the extreme volatility and skewness of returns, it is important to diversify the risks of private equity. This is best achieved by investing indirectly through a private equity fund rather than through direct investments in individual companies. Because most such funds typically limit their investments to a relatively small number, it is also prudent to diversify by investing in more than one fund. And finally, top-notch funds are likely to be closed to most individual investors. They get all the capital they need from the Yales of the world. Forewarned is forearmed.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners. For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth or its affiliates.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Read more articles by Larry Swedroe

The performance of private-equity (PE) funds has been disappointing. New research explains why this happened: Instead of driving operational efficiencies (as PE investors typically claim they do), those funds relied heavily on increasing the debt burden for the companies they bought.

The performance of private-equity (PE) funds has been disappointing. New research explains why this happened: Instead of driving operational efficiencies (as PE investors typically claim they do), those funds relied heavily on increasing the debt burden for the companies they bought.

Verdad also

Verdad also