Join the experts at Invesco for an educational webcast exploring strategies and ETFs for tax optimization.

A series of unprecedented and historic events has completely shifted the candidates and dynamics of the race for the presidency and Congress.

Should China deliver sufficient stimulus to break the cycle of tightening fiscal policy, we may find China, and emerging markets, investable again.

The puck has certainly moved since our last market commentary. This month, we argue that the needle on portfolio construction should move with it. Equities have been the driver of returns for much of the last few years.

Alpha (α) is a fundamental yet poorly understood concept in finance. Simply put, it is the difference between the return of an investment and that of a risk-adjusted benchmark. In a more advanced definition, alpha is the residual in an asset pricing equation (see Appendix A). Alpha is what active managers strive to achieve and passive managers do not pursue.

The wait is over for earnings watchers, as the latest quarterly read on US corporations kicks off with reports from JPMorgan Chase and Wells Fargo on Friday. Earnings will provide a gut check on the state of the US economy, and investors will be looking for these results to confirm the mostly improving economic data that’s been released in the last month or so.

A return to lower yields has been every bond fund manager's dream since the nightmare of 2022. But now, with expectations dashed that they’d get their wish this year, it appears they’ll have to hang their hopes on 2025.

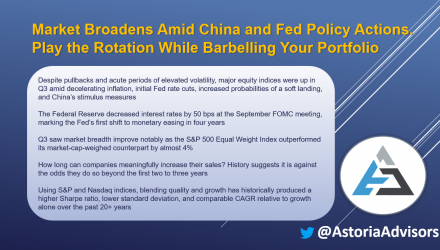

With many having characterized China as “uninvestible” just a few months ago, investors’ enthusiastic response in recent weeks to a perceived shift in the authorities’ policy reaction function is also likely to be an overreaction. It grossly oversimplifies the competing priorities of a country with internal imbalances, inefficient resource allocation channels, and exposure to further geopolitical tensions.

Underlying US inflation rose more than forecast in September, representing a pause in the recent progress toward moderating price pressures.

Wall Street banks are expected to launch a barrage of bond sales as soon as next week, capitalizing on ultra-low credit spreads and strong demand from investors after they report quarterly results.

Investors who buy bundles of loans packaged into bonds are increasingly using exchange-traded funds to do so, according to a report from Bank of America.

Private capital – encompassing private equity and private credit – is in the midst of a bit of a renaissance at the moment. IPO activity hit a peak in 2021, the year after the pandemic and then promptly plunged to levels not seen in years.

Tougher stances on trade are a point of bipartisan agreement.

The Fed’s “recalibration” of monetary policy is more than just about shifting to rate cuts. It also involves where the policy maker is now placing its greater emphasis on setting the course for easing in the future. Rather than inflation being the primary driver in the decision-making process, labor market activity has now taken center stage, and with that, one could argue, for the Fed, it’s now about the economy.

With interest rates declining, enthusiasm for muni bond ETFs could be reborn in income investors, including retirees.

Market participation broadened beyond technology stocks during the third quarter.

Elon Musk went all-in to get robotaxis onto roads, sacrificing a widely anticipated cheaper car, gutting teams focused on other projects and downplaying Tesla Inc.’s sales slowdown.

The US Justice Department is considering asking a federal judge to force Google to sell off parts of its business in what would be a historic breakup of one of the world’s biggest tech companies.

Britain’s stock-investing culture has been withering for years, with the only real growth coming from consultants, policymakers and commentators generating ideas on how to revive it. So why is Robinhood Markets Inc. so keen to expand in the UK? The draw may be more the country’s enthusiasm for online betting than allocating savings to equities.

It is hard to be “the most pro-union president in American history,” as Joe Biden likes to claim, while also leading an effort to “reimagine and rebuild a new economy,” as he has also promised. That’s because these goals are fundamentally incompatible: America’s unions no longer fit the modern economy.

If investors in Alphabet Inc. weren’t all that worried at first about the possible consequences of Google losing its search antitrust case, they perhaps should be now.

We hear it all the time: If you want to drive organic growth, create content online. Watch the short 4-minute video above to learn my 3-step process.

It is more common that teammates really enjoy the people they work with and have one another’s backs, but they don’t particularly want to give up personal time to spend more with workmates.

Unbundling services and offering them à la carte could appeal to clients who want more control over their financial management. This approach allows clients to tailor the services they receive to their unique needs and preferences.

On the latest edition of Market Week in Review, Investment Strategist BeiChen Lin examined the current state of the U.S. economy and outlined key investor watchpoints ahead of third-quarter earnings season.

Many emerging markets have delivered a robust performance this quarter amid a number of headwinds and we expect key geographies to build on that in the coming months.

Sports fans know that a lot can change in the fourth quarter of a game. So too for the U.S. economy, as a substantial labor action commenced the minute that calendars turned to the fourth quarter of 2024.

The jobs report closed last week with robust read outs of an official number that beat economist expectations. Below the surface, however, hours worked fell to levels often associated with recessions. This juxtaposition of more workers clocking fewer hours suggests that while employment figures are up, the quantity of work didn’t expand much.

As the November 2024 election draws near, the election outcome will profoundly affect the financial markets. Whether Donald Trump or Kamala Harris wins the presidency, each administration will bring distinct policies creating investment opportunities and potential risks for investors. With a divisive political landscape, it is crucial to understand how these potential outcomes can shape the stock market and your portfolio strategy.

Earnings season usually lasts around six weeks, so this wave of data will take us almost to Thanksgiving.

Last week marked the beginning of the end of one of the most rapid interest rate hiking cycles in U.S. history.

Real estate stocks are notoriously rate-sensitive assets. It’s not surprising the delivery of the rate cuts were beneficial to the sector.

Energy infrastructure companies are known for their free cash flow generation and generous, growing dividends. But what are the long-term growth drivers for these businesses and how do structural trends in energy benefit midstream/MLPs?

Today I'm going to share an excerpt from my fall letter to IMA clients. I'll discuss Charter Communications (CHTR) and Liberty Broadband, the vehicle through which we own Charter.

Whether you’re transitioning from another firm or starting from scratch, setting up your own independent registered investment advisor (RIA) firm is a tremendous opportunity that can provide higher earning potential, freedom, flexibility, and the opportunity to build a legacy.

If we all acted purely on logic, coffee shops would be out of business. Is that likely to happen any time soon? Don’t bet your latte on it.

A crystal ball enlightening a trader about the rate cut headlines would have been costly. However, a trader with the crystal ball and proper context may have been more successful.

Palmer Square Founder Chris Long discusses the $32 billion firm’s ETF entrance, spotlighting their Credit Opportunities ETF (PSQO) and CLO Senior Debt ETF (PSQA). VettaFi’s Todd Rosenbluth offers perspective on Bitwise’s XRP ETF filing, CLO ETFs, and the continued rise of actively managed ETFs.

Foreign Agents provides a powerful and depressing master class in the famous warning of Hamilton’s Federalist No. 21. To quote another founding father, Benjamin Franklin, “a republic, if you can keep it” indeed.

China’s recent stimulus announcements sparked a massive rally in its stocks, and a growing chorus of analysts see more gains ahead. Is this a reawakening of the country’s long slumbering stock market or just another false start? Bloomberg Opinion’s Nir Kaissar and Shuli Ren, based in the US and Hong Kong respectively, met online to discuss the risks and opportunities.

Judging from the public commentary, last Friday’s US jobs report confused economists in terms of their understanding of economic developments in the world’s largest economy and the policy approach of the Federal Reserve.

The rout in US government debt extended slightly on Tuesday, with longer-dated yields at the highest levels since late July and inflation data later in the week expected to enable Federal Reserve interest-rate cuts.

It’s no secret that betting on defense suppliers when geopolitical tensions ratchet higher pays off — at least in the short term. But Wall Street says there’s more to this latest rally.

US investment-grade corporate bond spreads have narrowed to the lowest level in more than three years, a clear sign of just how bullish credit investors are even as macro and geopolitical risks mount.

The federal debt is already $35 trillion and currently rising by roughly $2 trillion every year – with no end in sight. As a result, some investors are worried that the US could become a 21st Century version of Argentina: completely bankrupt and unable to pay the bills.

Just like road trips can bring unexpected detours, the economy and financial markets are at their own crossroads: recession or soft landing?

We bring together historical and real-time analysis for insight into the economy, markets, and potential alpha opportunities and risks we’re watching.

Policymakers have recognized China's slower economy.

Monetary policy began to transition from restrictive to neutral last quarter, and we’re optimistic that continued easing can prevent a hard landing.

Global monetary easing and modest growth are creating a fairy tale story for investors. Their very high conviction in the outcome of that story, however, belies a number of serious risks.