Originally published Oct. 4, 2024

Sports fans know that a lot can change in the fourth quarter of a game. So too for the U.S. economy, as a substantial labor action commenced the minute that calendars turned to the fourth quarter of 2024.

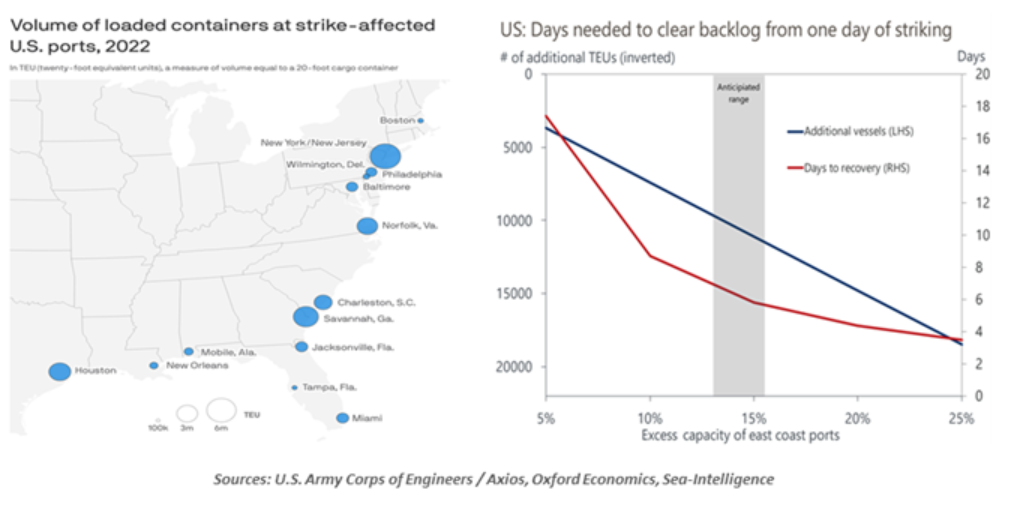

Roughly 45,000 members of the International Longshoremen’s Association union conducted a brief strike this week. These are the workers who move cargo between ships and ground transportation. The 14 affected ports, spanning from Texas to New England, account for 19% of the nation’s imports and 10% of exports, by value. The workers' primary demand was protecting their jobs against automation, along with higher wages.

One demand proved easier than the other. An offer by the U.S. Maritime Alliance of a graduated 62% wage increase over five years was enough to end the strike after three days. But the deal only runs through January 15 of next year. Negotiations will continue on the more thorny issue of protecting workers’ jobs against automation. This trend is inexorable and not unique to the ports; strident demands may be in vain.

While short, the port strike showed that supply chain friction can still arise.

The strong leverage of workers was a theme of the COVID reopening cycle. A shortage of labor amid high demand enabled workers to make more aggressive demands. Despite a normalizing labor market, the stevedores demonstrated that labor still has some power. Consultancy RSM estimated a loss of $4.3 billion in trade, or about 0.1% of gross domestic product, for each week the strike carried on. The knock-on shortages of fresh food and raw materials for production of vehicles and pharmaceuticals had the potential to cause broad upset.

The strike was one among many reasons to be braced for an unusual interval ahead. A prolonged walkout could have weighed down readings of employment and gross domestic product. The damage from Hurricane Helene is still being tallied but has certainly brought some regions to a standstill. Oil prices are on the rise again amid escalations in the Middle East. Election uncertainty is forestalling decisions about investments. The fourth quarter, only days old, is already bringing much more suspense than we would like.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust