Stocks posted another good quarter with the S&P 500 up 5.89% (total return). Bonds also posted a strong total return with the TLT bond ETF up 7.93% in the quarter. It was enough to make investors feel all warm and fuzzy inside.

Clearly, the Fed was a key component to the mood music. Anticipation of a rate cut, and then final implementation of the cut, drove positive sentiment through the quarter. With that big policy threshold crossed, the question now is how does the story end?

A nice story

To be sure, the Fed has had an accommodating audience in that market participants have bought the Fed's narrative of a "soft landing" hook, line and sinker. If there is one element that stands out in regard to the investment landscape, it is the high degree of certainty with which investors believe conditions are favorable.

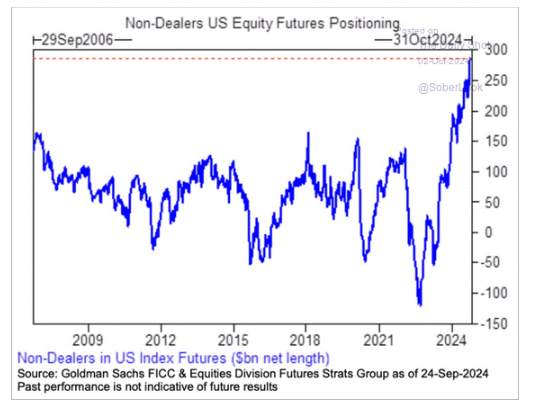

This high degree of certainty is reflected a number of ways. For example, The Kobeissi Letter shows "Bullish sentiment is through the roof: US equity futures positioning by investors excluding market-makers just hit a net long of ~$290 billion, the most on record.”

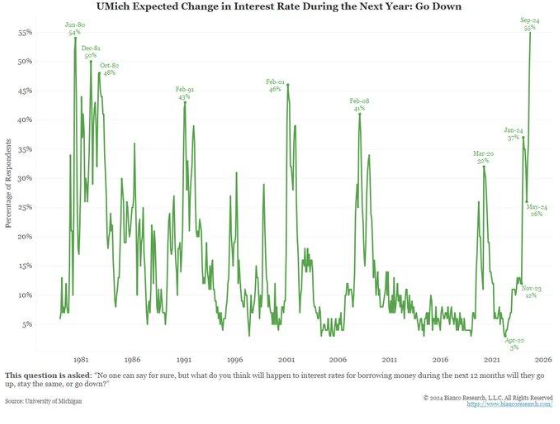

The bullishness has also extended to bonds. Jim Bianco points out "In the last half-century, 'civilians' have never been this bullish on the bond market."

Of course, there are reasons for this extreme sentiment. Inflation has been quiescent as of late, earnings are growing nicely, bond volatility, in particular, has declined, and monetary policy is easing across the board. It's all very appeasing, like a good bedtime story.

Inconvenient truths

Bedtime stories have their purpose, but providing clear-eyed, objective investment analysis is not one of them. For better and worse, we don't have to go too far or work too hard to find evidence to seriously challenge the "Goldilocks" view of investment conditions.

Let's start with inflation. While reported numbers are coming in close to the Fed's targets, they aren't there yet. Further, an easy case can be made that inflation is turning higher. As Robert Armstrong reported for the FT ($), "We like to look at the month-to-month change in core inflation and annualise it ... That figure has now risen smartly for two months in a row."

In addition, Matt Klein ($) shows "Inflation Is Still Hotter than Pre-Pandemic". He highlights that not only is inflation not falling any longer, but it is still noticeably above target. While he does not purport this to be a huge problem necessarily, he notes. "it is worth bearing in mind when thinking about where interest rates might end up once the Fed finishes its 'recalibration'." In short, the so-called "neutral" rate may be a fair bit higher than before the pandemic.

Finally, while most attention is placed on demand as the most likely cause of inflation, supply constraints are every bit as much of a threat. Geopolitical conflict, weather events, and labor strikes can all visibly cause supply disruptions. Further, long-term underinvestment in infrastructure and commodity production also present challenges – and challenges that cannot be resolved quickly.

Indications the placid demeanor of the market may be misplaced come from abroad as well. While China has made news recently with its policy stimulus and soaring stock market, Michael Pettis establishes some valuable perspective: Policy provisions to date do not address fundamental deflationary pressures.

He highlights, "What Caixin doesn't say is that the need to turn these empty apartments into cash as soon as possible can't help but put further downward pressure on apartment prices in the near term." Bob Elliott adds, "So the primary initial macroeconomic focus area is arresting the acute property price declines".

This is a key point. Property price declines have not stopped yet, nor has associated bad debt been dealt with. As a result, the baseline condition in China is still deflation. Elliott concludes, "For a global macro investor, the CHN *economy* matters a lot more." So, China remains a threat to global growth.

Not to be outdone, Japan also needs to be considered for its potential to upset markets. Tracy Shuchart posts a good overview of the situation:

Japan’s $4 Trillion ‘Carry Trade’ Begins to Slowly Unwind

Japan’s investors are starting to lose their decades-long infatuation with overseas assets.

In the first eight months of the year, Japanese investors snapped up a net ¥28 trillion ($192 billion) of the nation’s government bonds, the largest amount for the time frame in at least 14 years. They also cut purchases of foreign bonds by almost half to just ¥7.7 trillion and their buying of overseas equities was less than ¥1 trillion.

“It’s going to be one of the mega trends and it is a super cycle for the next five to 10 years,” said Arif Husain, head of fixed-income at T. Rowe Price, who has nearly three decades of investing experience. “There will be a sustained, gradual but massive flow of capital back into Japan from abroad.”

With $4.4 trillion invested abroad, an amount larger than India’s economy, the speed and size of any pullback has the power to disrupt global markets. Even as the gap in rates between Japan and other countries has narrowed, the inflows have been a trickle rather than the flood some investors have feared.

Since the US stock and bond market has been a primary destination for Japanese capital, it is fair to expect "a sustained, gradual but massive flow of capital back into Japan" from those markets.

Switching back to the subject of bedtime stories, one of the more notable patterns over time is that of the political economy. Incumbent administrations have every incentive in the world to try to boost the economy in front of an election. That involves real decisions to direct spending within its authority, but it also involves the formation of a narrative to "explain" to people what the data mean.

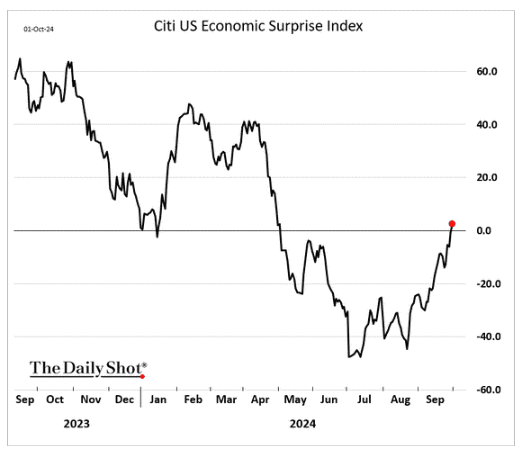

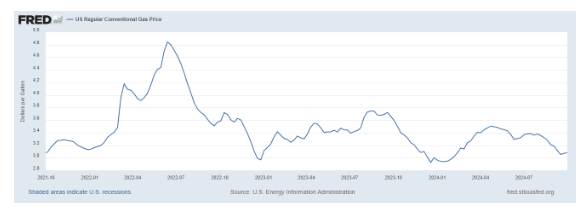

At the present time, the combination of improving economic growth (from The Daily Shot) and a notable decline in one of the most visible indicators of inflation, gasoline (Source: Federal Reserve Economic Data), tells a very nice story for the Harris campaign. Perhaps too nice. Investors should at least consider the possibility that political motives may be at work in regard to both the data we are receiving and the narrative around it. In short, the picture we are getting right now may not be a very representative one -- and may look quite a bit different in a couple of quarters.

Finally, bedtime stories are occasionally dramatized with a big baddie. In financial markets, one of the recurring villains is rates markets, the financial plumbing. Almost on cue, rates markets have begun to wobble again.

Scott Skyrm exclaims, "So much for the Repo Rate Corridor! There is supposed to be a ceiling and floor on Repo rates that keeps rates within the fed funds target range." CrossBorder Capital also suggests heightened awareness is appropriate: "Last two days have seen #US GC repo and SOFR rates blow out...result our daily market #liquidity measures have skidded lower. Nothing yet, but... lets watch".

Conclusion

The common theme that emerges is there are a lot of ways in which the “Goldilocks” scenario may fail to materialize. On one hand, conditions may prove less favorable than currently perceived. Inflation may turn out to be more persistent. Various trade frictions could cause supply shortages reminiscent of the pandemic era. China could export deflation to the rest of the world. Japan could repatriate vast amounts of capital at the expense of markets in the US and elsewhere.

To the extent these types of issues might undermine the current investment thesis, they would fall under the nugget of wisdom, "It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so."

On the other hand, it may be that the conviction of investors to seek risk and to make bets subsides. After the election, it may become clear that policies to support capital at the expense of labor will become a political liability. The government may become unable or unwilling to support markets with the same fervor as it has in the past. The Fed may change direction (again) and pause on rate cuts. Perhaps worse, it may become clear the Fed is no longer able to steer markets as it has in the past.

Either of these reasons would be sufficient for markets to give up ground and both are quite possible. As a result, investors would do well to treat current market euphoria as a trading opportunity at best. Long-term investors should recognize the current risks and incorporate them into their long-run risk allocations. Those who luxuriate in the fairly tale stories about markets are most likely to experience unhappy endings.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Arete Asset Management

Read more commentaries by Arete Asset Management