Market Broadens Amid China & Fed Policy Actions. Play the Rotation While Barbelling Your Portfolio

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMajor Indices Rally in Q3 2024

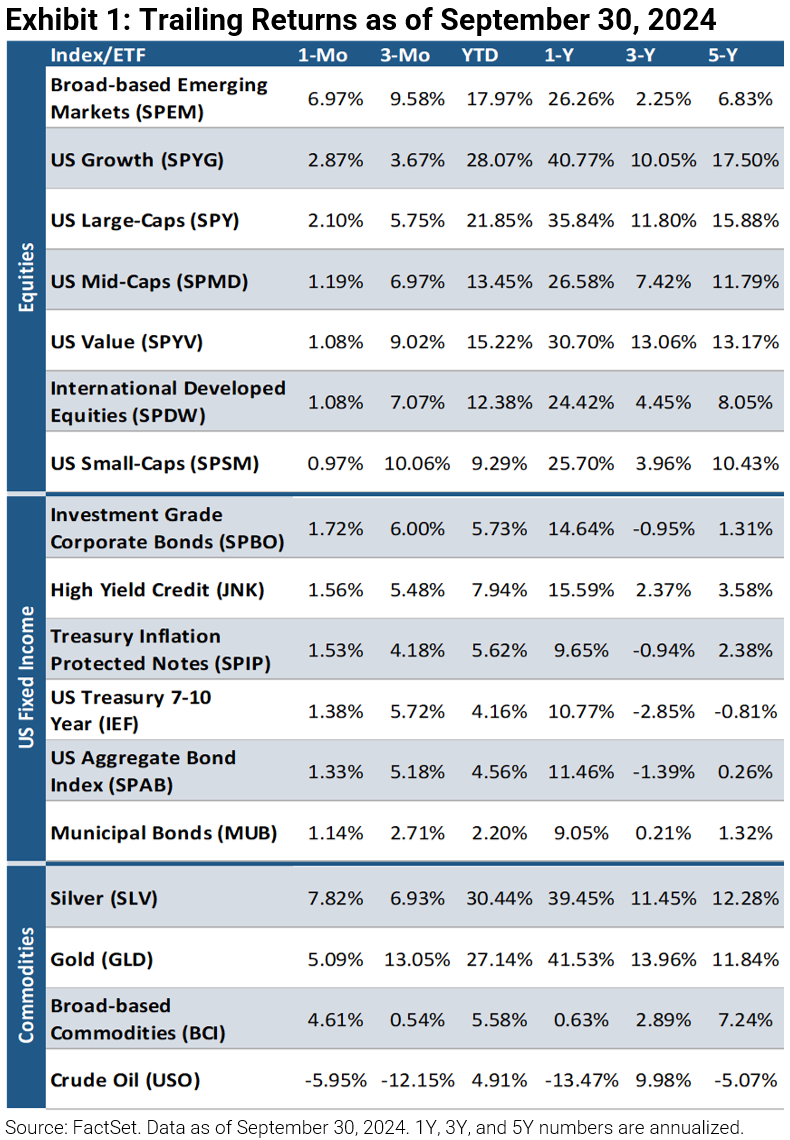

Despite pullbacks and acute periods of elevated volatility, major equity indices were up in Q3 amid decelerating inflation, initial Fed rate cuts, increased probabilities of a soft landing, and China’s stimulus measures. Market participation broadened beyond technology stocks during the quarter as the S&P 500 Equal Weight Index rose 9.6% while the market-cap-weighted S&P 500 and Nasdaq 100 gained 5.9% and 2.1%, respectively. US small-caps (+10.1%) were among the best performers, followed by emerging markets (+9.6%) and US value (+9.0%). Bonds fared well as investment grade corporates rose 6.0%, 7-10 year US Treasuries gained 5.7%, and high yield credits increased 5.5%. Aside from crude oil (-12.2%), commodities produced positive returns as gold was up 13.1%, silver rose 6.9%, and broad-based commodities increased 0.5%.

Fed Cuts Rates by Half Percentage Point

The Federal Reserve decreased interest rates by 50 bps at the September FOMC meeting, dropping the fed funds rate to the 4.75–5.00% range. The move marks the Fed’s first shift to monetary easing in four years. As recent Consumer Price Index (CPI) and Personal Consumption Expenditure (PCE) readings continue to trend downwards and various measures of job growth have softened, Fed Chairman Jerome Powell stated, “Inflation is now much closer to our 2 percent objective. Today, we see the risks to achieving our employment and inflation goals as roughly in balance.” Although most interest rate cuts of 50 bps in magnitude have historically coincided with panic in the market, Powell stressed confidence in both the strength of the economy and the Fed’s ability to reduce inflation without a significant rise in unemployment. “The time to support the labor market is while it's strong, not when you start seeing layoffs... You can take this as a sign of our commitment not to get behind,” he said. In the updated dot plot, policymakers indicated 50 more bps of easing over the last two meetings in 2024.

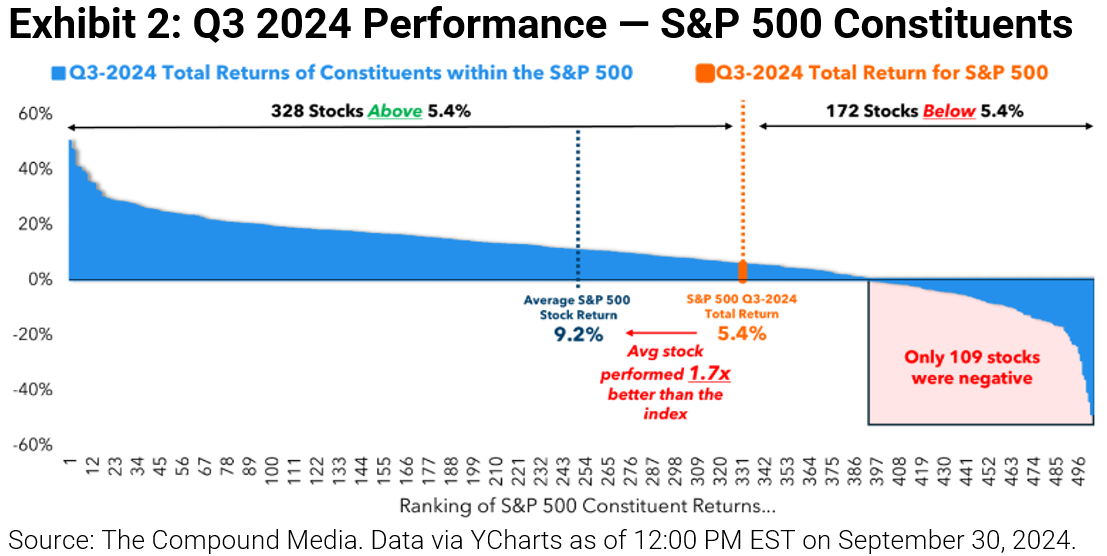

Market Breadth Improves in Q3

Q3 saw market breadth improve notably as the S&P 500 Equal Weight Index outperformed its market-cap-weighted counterpart by 3.7%. Data from The Compound (see Exhibit 2) shows over 65% of the stocks in the index generated a greater quarterly return than the market-cap-weighted S&P 500. The average constituent was also up 9.2%, which is almost two times greater than that of the market-cap-weighted index.

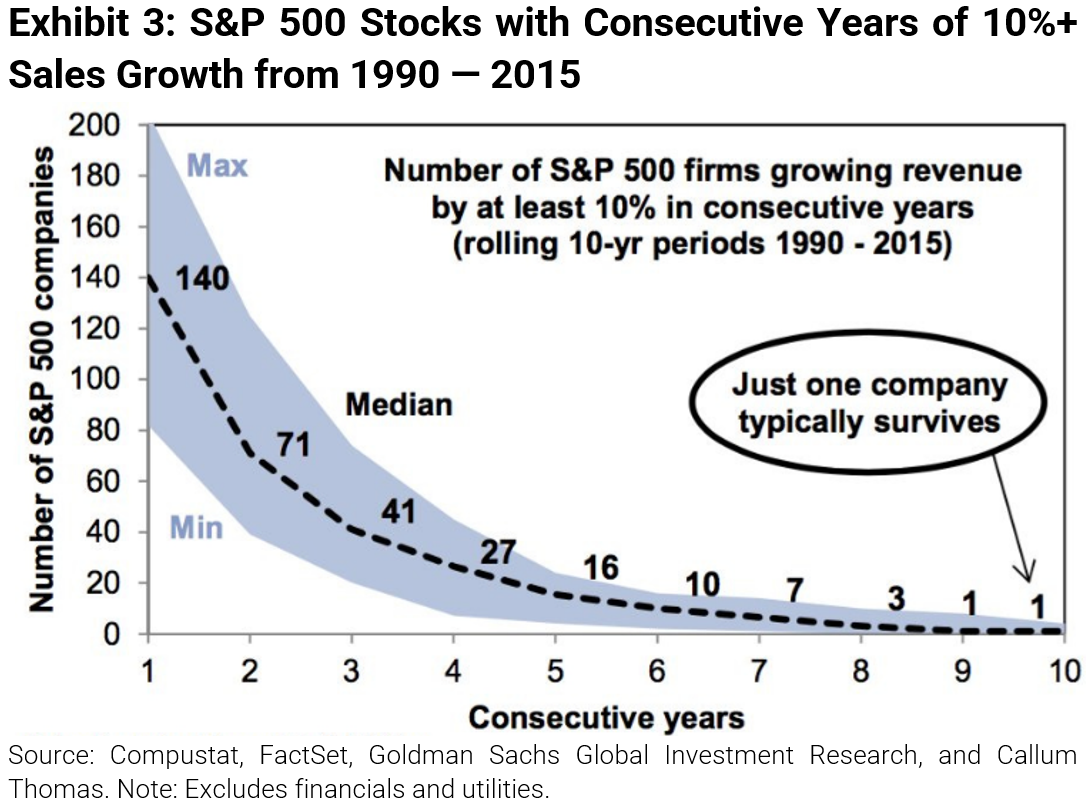

How Long Can Companies Meaningfully Increase Their Sales?

When analyzing historical year-over-year revenue growth of S&P 500 stocks, it appears unlikely that companies can consistently achieve rapid sales growth over an extended period. While there are numerous instances in which stocks have grown their sales by more than 10% for two to three consecutive years, the number of companies that can do so beyond that period declines over time.

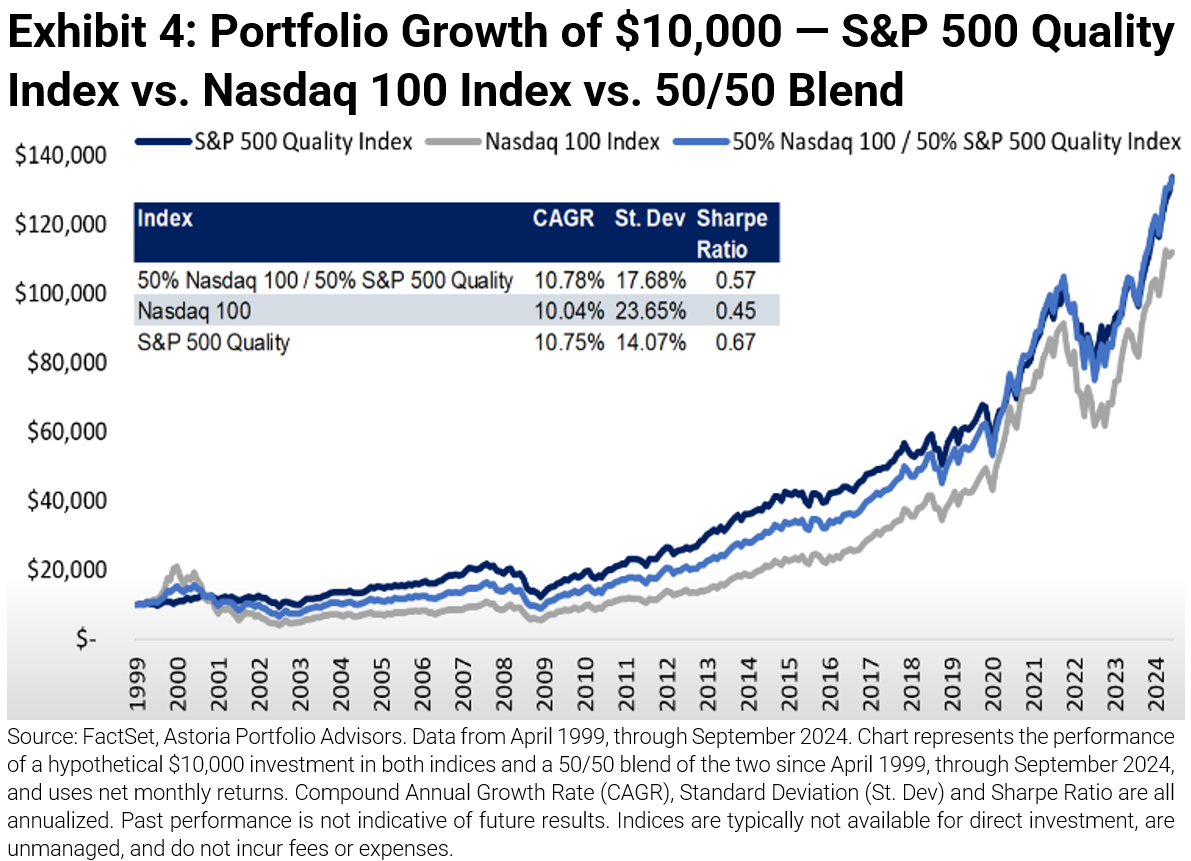

Blending Quality and Growth

When blending the S&P 500 Quality Index with the growth-oriented Nasdaq 100 Index (see 50/50 blend in Exhibit 4), quality and growth combined have historically produced a higher Sharpe ratio, lower standard deviation, and comparable CAGR relative to the Nasdaq 100 Index alone over the past 20+ years.

Market Broadens Amid China and Fed Policy Actions. Play the Rotation While Barbelling Your Portfolio

The Fed cutting interest rates by 50 bps earlier this month could be interpreted as a catch-up move as the US central bank did not cut at the July meeting, and the 2-year US Treasury yield was priced for a reduction of that magnitude. In our view, it’s more important that initial 50 bps decrease was delivered without causing a growth scare.

More cuts are now priced in through 2024 and 2025 end, but the rate at which economic data deteriorates, specifically regarding growth and the labor market, will likely determine if the rate cuts will be supportive (the Fed cuts because it can) or detrimental (the Fed cuts because it must) for equities.

As initial claims have retreated somewhat from recent highs and Q3 GDP growth estimates remain healthy, concerns of a significant slowdown have declined. Up until the cut, defensives have performed well, and their valuations have now richened, so we believe trimming such areas and buying quality growth exposure is appropriate. However, if future payroll numbers come in much lower than expected, or Q3 S&P 500 earnings are largely disappointing, defensives may once again come into play.

For these reasons, we prefer to barbell one’s portfolio by owning own high quality growth orientated stocks along with a smaller portion of defensives while hedging with value sectors like industrials, materials, and energy. Both emerging and international developed markets have also become more attractive to own given high estimate revisions, low valuations, a weakening dollar, accommodative central bank policies, and China’s monetary and fiscal stimuli.

Moreover, we remain bullish on the rotation away from the Magnificent 7 and into broader US market, we are playing this via equal weighted strategies. Earnings estimates are expected to be higher for the S&P 493 vs. Mag 7, and value/high quality dividend-oriented equities and small-caps may become more attractive as rate cuts continue. Lastly, we advocate extending duration from cash into Treasuries while hedging overall portfolio risk with gold.

Originally published October 2, 2024

For more news, information, and analysis, visit the ETF Strategist Channel.

Warranties & Disclaimers

As of the time of this publication, Astoria Portfolio Advisors held positions in SPYG, SPY, SPYV, SPDW, SPMD, SPSM, SPEM, SPBO, SPAB, MUB, IEF, SPIP, GLD, SLV, USO, and BCI on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All