Private capital – encompassing private equity and private credit – is in the midst of a bit of a renaissance at the moment. IPO activity hit a peak in 2021, the year after the pandemic and then promptly plunged to levels not seen in years. In the U.S., although counts can vary due to differing criteria, in the vicinity of 1,000 IPOs launched in 2021, but fewer than 200 came to market in 2022. The reasons for this are complex, ranging from increased regulations to geopolitics to interest rates, but it’s left a hole – one that the private capital industry has flooded into.

Companies looking for funding are currently more likely than in previous years to seek it on the private markets rather than by taking their firm public. In fact, even before the pandemic, a report from Citizens Bank noted that companies backed by private equity firms outnumbered publicly held firms and had done so since 2012.

Private equity companies take stakes in nonpublic companies that allow them to exert some control over how the company is run such as the hiring and firing of c-suite executives. Meanwhile, private credit companies provide loans to both public and nonpublic firms rather than taking direct stakes in them.

However, that “private” aspect can leave the average investor out in the cold when it comes to getting access to those high-growth firms that would normally debut via IPO, unless the private capital firm involved is itself publicly traded. There are a number of such companies, but selecting them for investment purposes is most likely challenging for investors who aren’t experts in the field and may not know how to evaluate such a security.

And make no mistake, retail investors are the next major growth source for private capital.

“According to a report by Bain Capital, as of 2022, individual investors held approximately 50% of the $275 trillion of global AUM. But those same investors represent a very small percentage of AUM held by alternative investment funds,” Elie Azar, founder and CEO of White Wolf Capital Group, an alternative investment firm, noted.

He went on to point out that in the 1970s and 1980s, institutional investors owned small allocations to private equity in the range of 1% to 5%. That range is closer to 20% to 30% today.

“My opinion is that we will see that same trend with the individual investor,” Azar added, pointing out that the potential represented by retail investors is a major tailwind for the growth of private capital markets.

The Perfect Wrapper

And this is where ETFs come into play. The investment wrapper has long been referred to as a democratizing force in financial markets as many of the products available offer exposure to areas of capital markets previously unavailable to the average retail investor, whether it be commodities or currencies or other alternative asset classes.

Private capital is yet another area ETFs have penetrated to offer institutional-type exposure beyond the high-net-worth audience. The benefits include ownership of a basket of securities representing the desired asset class, generally lower costs and tradability.

The first private equity ETFs appeared shortly before the Great Financial Crisis, and today there are four currently trading, with a variety of differentiating features. The newest of these is the WHITEWOLF Publicly Listed Private Equity ETF (LBO), which is actively managed by White Wolf Capital, which specializes in investing in private capital markets. It started operations in 2011. LBO launched in November 2023.

LBO is, in fact, the only private capital ETF that is managed by a firm that operates primarily in the private equity space. Thus, its management team can leverage that boots-on-the ground knowledge (as well as its more than 10 years of experience) to select the fund’s portfolio.

“We always go back on a quarterly basis to make sure that all underlying holdings align with our thesis” said Rahul Hukeri, White Wolf managing director and head of private fund investing. He notes that holdings are under constant review, with each 10-K and 10-Q scrutinized as they become available.

This is quite notable, but it’s also just one feature of the fund’s value proposition relative to private capital markets.

Why Private Capital?

The investment argument for exposure to the private capital category is multi-faceted, but as with all alternative investments, diversification is perhaps the primary reason to consider the space. Uncorrelated returns are increasingly hard to find, and private capital offers a unique type of exposure in that regard.

Consider that private capital firms, including the publicly traded ones, offer investors exposure to all the firms that they invest in. Given that each one can invest in many companies, with some firms’ counts numbering in the hundreds, there is a significant amount of diversification to potentially be derived from exposure to the equities of even just one private capital company. Moreover, with fewer companies going public, that means broad equity ETFs are somewhat less diversified, meaning that investing in private capital helps investors account for that gap somewhat.

But that’s not all that private capital exposure offers. Income is a little less elusive for investors now that interest rates are in a somewhat normal range, but it’s still a key concern for them, especially those headed for retirement. Private credit firms like business development companies are structured as registered investment companies (RICs), so they must distribute the vast majority of their investment income to shareholders. That means investors in those securities can see large distributions. Investors in private equity companies also often receive dividends, but not to the same extent as private credit firms.

Private capital also comes with a growth element. Private capital investments tend to be in small- to midcap companies that the private capital firm expects to demonstrate strong and rapid growth such that it makes its investment back – along with a tidy profit – within a reasonable window of time. Private equity companies can see the benefits of that rapid growth, which in turn benefits their shareholders.

Private equity and private credit do not behave like traditional equity and fixed income assets, which makes it all the more imperative that funds investing in private capital firms have managers with the expertise to drive their investment choices.

Why LBO?

Management by an experienced private capital-focused investment firm is not the only advantage LBO brings to the table. Although, that active management means that not only can the fund’s managers leverage their firm’s aggregate knowledge, the managers are also given the latitude to respond to developments in the market in real time, rather than having to wait for an index rebalance as is the case with passively managed funds.

LBO’s portfolio, which can hold up to 40 securities, is among the most diversified private capital ETFs available. Its combined holdings offer exposure to roughly 4,000 unlisted small- to midcap companies, on a look-through basis.

The fund’s managers seek that exposure by investing in a range of types of participants across the leveraged buyout ecosystem, covering both private equity and private credit. The private equity segment of the portfolio includes limited partners, asset managers, and buyout firms, all representing roughly 45% of the fund’s portfolio. Leveraged finance providers, meaning private credit, constitute the remaining (and largest) portion of the portfolio.

Its existing competitors focus on either private equity or private credit (the latter in the form of BDCs), so investors do not get the benefit of exposure to the whole private capital space.

“We wanted to have an ETF that provided exposure to that ecosystem,” Azar said

The fund’s methodology combines qualitative and quantitative criteria to arrive at its portfolio, with rebalances occurring on (if needed) on a quarterly basis. The qualitative portion of the investment approach mainly relates to what firms are eligible for inclusion, while the quantitative portion targets firms that demonstrate liquidity, income generation in the form of stable and sizable dividends, low volatility and the delivery of value for investors, with liquidity considered the highest priority.

That means, according to Azar, that LBO can handle large inflows without seeing any corresponding movement in its share price.

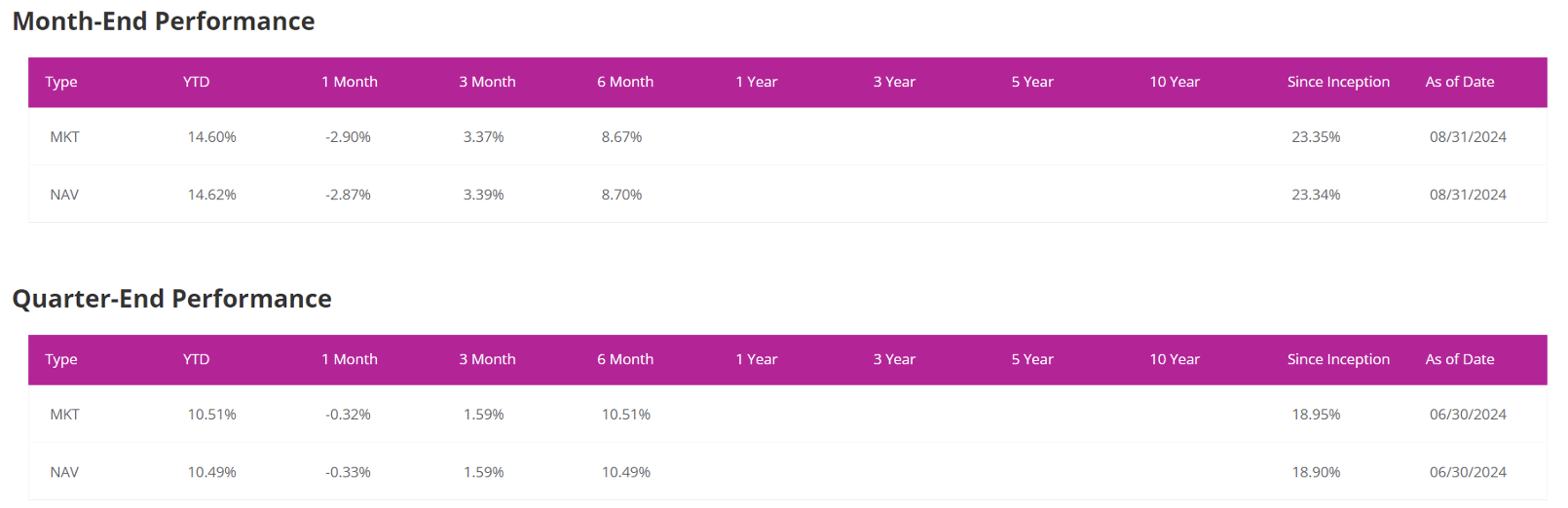

But perhaps most remarkable for investors considering the ETF is its performance. Having launched in late 2023, the fund’s performance in 2024 has outstripped that of its private capital competitors as well as matched the performance of the broad U.S. market, despite minimal overlap in exposure.1

Final Thoughts

LBO stands alone among its peers, due to its expert active management by actual participants in the private capital space, its unique mix of company types – including both private equity and private credit – and its exceptional performance. The fund has the potential to deliver outsized returns in the current environment, with private capital still growing in importance relative to public capital markets.

- Performance quoted represents past performance and does not guarantee future results. Investment return and principal value will fluctuate so shares may be worth more or less when redeemed or sold. Current performance may be lower or higher than that quoted.

Market price returns are based upon the closing composite market price and do not represent the returns you would receive if you traded shares at other times. Returns are average annualized total returns, except those for periods of less than one year, which are cumulative. YTD is year-to-date and ITD is inception-to-date. NAV: The dollar value of a single share, based on the value of the underlying assets of the fund minus its liabilities, divided by the number of shares outstanding. Calculated at the end of each business day.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a Prospectus or SAI with this and other information about the Fund, please call +1-305-605-8888 or visit our website at https://lbo.fund/. Read the prospectus or summary prospectus carefully before investing.

Investments involve risk. Principal loss is possible. Redemptions are limited and often commissions are charged on each trade. Unlike mutual funds, ETFs may trade at a premium or discount to their net asset value.

Investment Risk. When you sell your Shares of the Fund, they could be worth less than what you paid for them. The Fund could lose money due to short-term market movements and over longer periods during market downturns. Securities may decline in value due to factors affecting securities markets generally or particular asset classes or industries represented in the markets.

Listed Private Equity Companies Risk. There are certain risks inherent in investing in listed private equity companies, which encompass financial institutions or vehicles whose principal business is to invest in and lend capital to or provide services to privately held companies. Generally, little public information exists for private and thinly traded companies, and there is a risk that investors may not be able to make a fully informed investment decision. The Fund is also subject to the underlying risks which affect the listed private equity companies in which the financial institutions or vehicles held by the Fund invest. Listed private equity companies are subject to various risks depending on their underlying investments, which include additional liquidity risk, industry risk, foreign security risk, currency risk, valuation risk and credit risk.

Business Development Company (BDC) Risk. BDCs generally invest in less mature U.S. private companies or thinly traded U.S. public companies which involve greater risk than well-established publicly traded companies. While the BDCs in which the Fund invests are expected to generate income in the form of dividends, certain BDCs during certain periods of time may not generate such income. The Fund will indirectly bear its proportionate share of any management fees and other operating expenses incurred by the BDCs and of any performance-based or incentive fees payable by the BDCs in which it invests, in addition to the expenses paid by the Fund.

Master Limited Partnership Risk. An MLP is an entity that is classified as a partnership under the Internal Revenue Code of 1986, as amended, and whose partnership interests or “units” are traded on securities exchanges like shares of corporate stock. Investments in MLP units are subject to certain risks inherent in a partnership structure, including (i) tax risks, (ii) the limited ability to elect or remove management or the general partner or managing member, (iii) limited voting rights and (iv) conflicts of interest between the general partner or managing member and its affiliates and the limited partners or members.

New Fund Risk. The Fund is a recently organized management investment company with no operating history. As a result, prospective investors have no track record or history on which to base their investment decision. There can be no assurance that the Fund will grow to or maintain an economically viable size.

The Fund is distributed by Quasar Distributors, LLC. The Fund’s investment advisor is Empowered Funds, LLC which is doing business as ETF Architect.