With the Fed Cutting Rates, What Is the Outlook for Future Mortgage Rates?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsLast week marked the beginning of the end of one of the most rapid interest rate hiking cycles in history. There has been no historical precedent for the events that followed Covid-19 and the ensuing response, so there is no relative example for what may continue to happen going forward.

As one of the most interest rate sensitive sectors, the housing market has been highly affected. Higher mortgage rates have shuttered demand. Mortgage originations fell over 50% in 2022, then fell another 39% in 2023, and are trending at similar rates in 2024—roughly 40% below pre-Covid levels. The existing home market is similarly weak with existing home sales volumes 24% below pre-Covid levels[1].

Despite this weakness, home prices remain near historical highs as overall supply has also been curtailed with homeowners unwilling to part with their existing low-rate mortgages. And, despite the 10-year treasury settling in at 3.68%—forecasting lower continued inflation—market rates for mortgages remain stubbornly high at 6.08% according to Freddie MAC and an even higher 6.69% according to the BankRate benchmark[2].

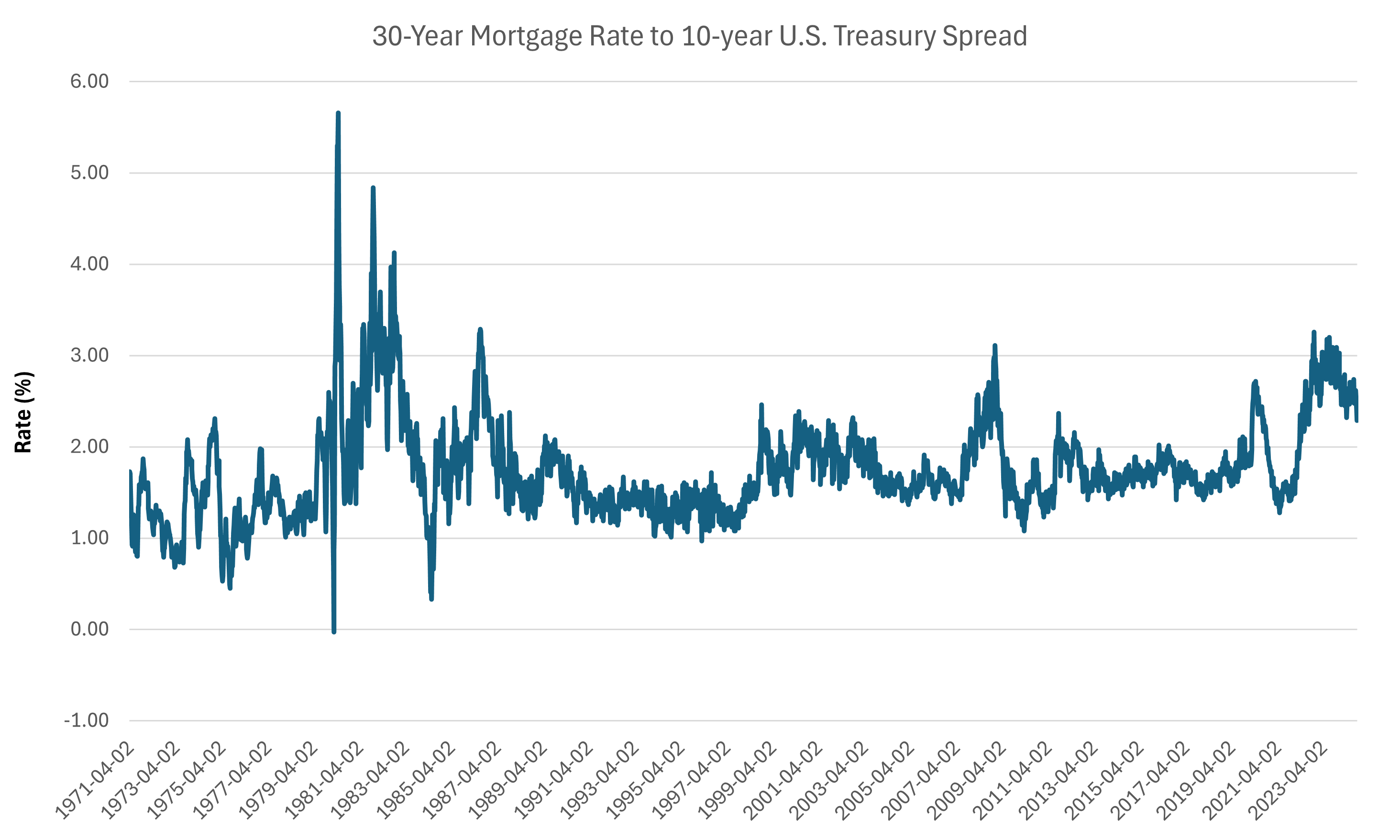

Source: FRED, Federal Reserve Bank of St. Louis. Accessed 9/20/24. 4/2/1971 to 9/26/2024.

Current Mortgage Rates and Spreads

Typically, mortgage rates are driven directly off the 10-year treasury, trading at a relatively low spread given the relative stability of the underlying asset (collateral) and the high propensity of homeowners to pay their mortgage. As the chart below shows, this “spread” peaked even higher during the current rate cycle than during the most stressed housing market in recent history. Now, nearly every market-based interest rate has trended lower and yet mortgage spreads remain anomalously high relative to history.

Source: FRED, Federal Reserve Bank of St. Louis. Accessed 9/20/24. 4/2/1971 to 9/26/2024.

What drives mortgage rate spreads?

There are two major components that create the risk that lenders must be compensated for when issuing a mortgage:

- Interest rate volatility

- Asset price risk

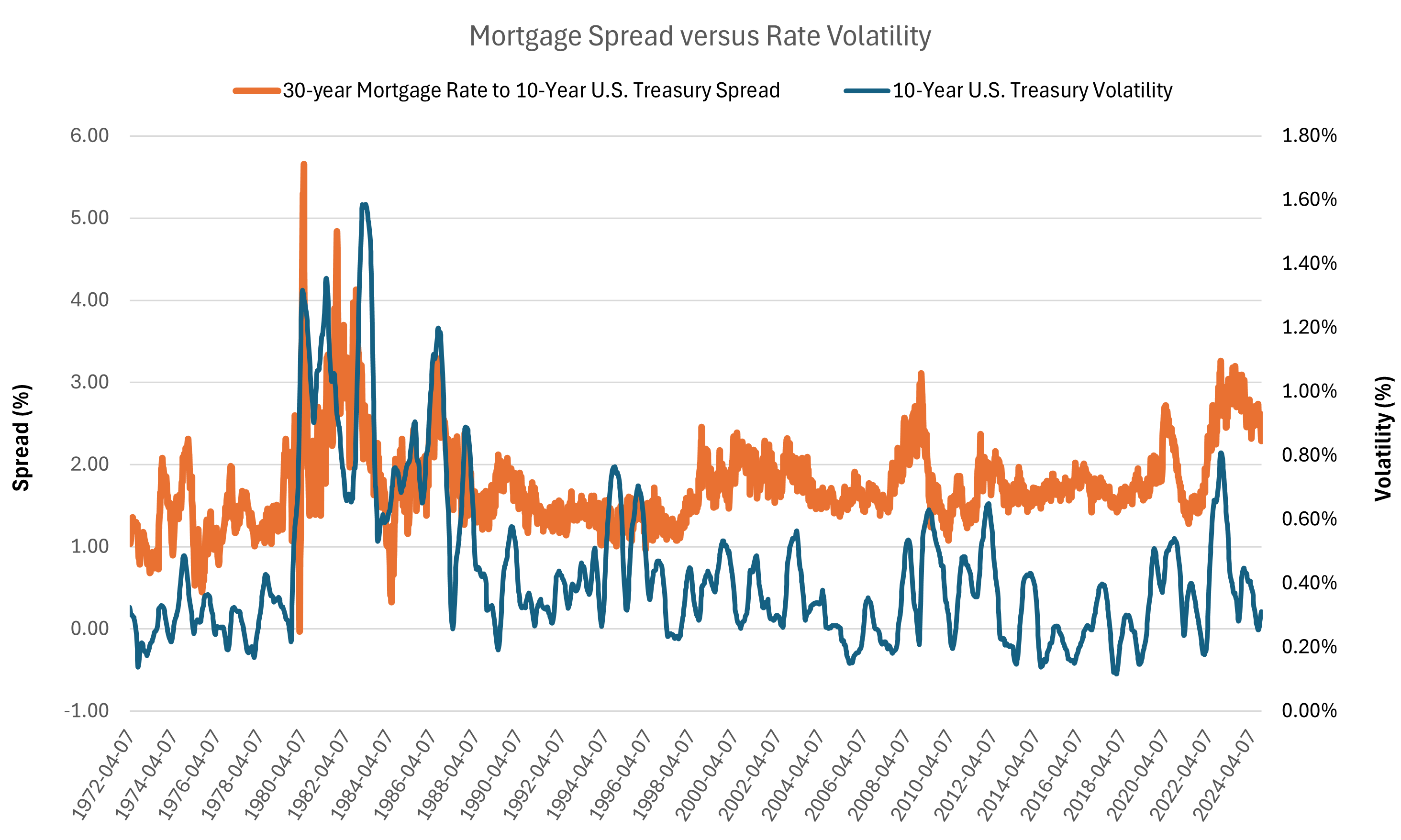

Mortgage owners have the ability to pre-pay (re-finance) their mortgages at any time should interest rates fall, therefore, lenders are essentially making a fixed rate loan with an embedded put option on interest rates. The value of any option is predominantly driven by the expected volatility of the underlying asset hence a more uncertain rate outlook should drive wider mortgage spreads and indeed it has.

Source: FRED, Federal Reserve Bank of St. Louis. Accessed 9/20/24. 4/7/1972 to 9/26/2024.

Secondarily, if creditors are worried about the value of the underlying asset, they would view the loans as riskier, which is likely to occur in periods of extreme market stress such as 2008. Despite continued strong pricing in the home market, volumes are relatively low which may make prevailing prices a bit stronger than they would be if more sellers were willing to enter the market. It is possible lenders attribute some price risk due to this as well, aiding the higher spread.

Homebuilders as evidence of future mortgage rates.

We’ve discussed homebuilders at length over the past two years. They’ve been a somewhat unlikely beneficiary of the rate hikes, substantially increasing their share of the overall homes sales market which is typically far more driven by existing (owner-occupied) home sales.

Builders have been able to hold prices high even as input costs have cooled with inflation. One technique they’ve used to great success in the current higher rate environment has been mortgage rate buydowns. Builders are typically spending to bring the rate into a range of 5-5.5%[3].

Where should mortgage rates land?

With homebuilders increasingly the marginal seller of homes, they may represent the most accurate “market clearing rate”. History supports this range as well. In the 10-year period from 2009 to 2019 mortgage rates averaged 1.69% more than the prevailing 10-year treasury. This number closely coincides with the average for the entire history of the available data dating back to 1971 of 1.75%. These imply a “normal” mortgage rate of 5.48% to 5.54%[4] and we expect mortgages will ultimately trend towards this range over the next year or two

There are likely large amounts of homebuyers and sellers currently sitting on the sidelines in anticipation of lower mortgage rates. We would agree with their apprehension and suggest they will be rewarded with lower rates in time but believe the effect on home prices is less predictable. Lower rates may bring back more sellers than buyers, creating a great situation for prospective new homeowners but perhaps introducing some risk to the strength of the overall housing market.

For more timely market updates from our portfolio management team or our weekly Fireside Charts blog, visit and subscribe at blog.investbcm.com.

By Brendan Ryan, CFA, Partner and Portfolio Manager

Originally Published October 2, 2024

For more news, information, and strategy, visit the ETF Strategist Channel.

Disclosures:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)

[1] Bloomberg data 12/31/2019 through 12/31/2023, National Association of Realtors

[2] Bloomberg data as of 9/26/2024, Bankrate.com – US Home Mortgage 30 year Fixed National Average

[3] In normal times, homebuilders offer varying levels of discounts. For example, the largest homebuilder in the US, Lennar, typically offers incentives in the range of 3-7%, but since 2022 these have ballooned to 9-10% driven by increased “mortgage rate buydowns”.

[4] Based on the 10-year treasury rate as of 9/26 of 3.79%

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All