Multi-sector fixed income strategies can deliver significant benefits to investors – including yield enhancement, volatility reduction and diversification of asset-class exposures – because of managers having the freedom to make tactical shifts between fixed-income sub-sectors.

Stocks are up 18.7% year-to-date, which is good news for portfolios and 401(k)s, but did you know that most of the heavy lifting has been done by a very small number of S&P 500 stocks?

We believe idiosyncratic credit events may occur over the next 12 months, but systemic bank risk is remote.

A steady stream of news helped drain enthusiasm from the equities markets through most of August, snapping a five-month growth streak at a time of the year known for cool market performance despite the swelter of its dog days.

While the S&P 500 delivered solid performance this summer, we remain cautious in the near term given the Index remains modestly above our year-end target of 4,400.

US hiring picked up in August and wage growth slowed, offering a mixed picture of both resilience and moderation in the labor market.

Given their overall credit risk versus safer government debt, corporate bonds may not get enough exposure in a retirement portfolio. However, they can serve a purpose as long as investors are aware of their nuances.

Investors looking for extra yield are driving corporate bonds to some of their tightest valuations of the year, pushing money managers including Pacific Investment Management Co. toward mortgage debt that looks much cheaper.

We believe the best way to add value is through relative positioning in sector allocations, individual security selection and along the yield curve, holding duration neutral overall. That approach, however, does not prevent us from having views on interest rates and we think bonds offer good value at current rate levels.

Although high-yield bonds have performed well so far this year, we continue to take a cautious view.

Investors seeking higher yields and relatively low risk, and are willing to sacrifice liquidity, will find attractive opportunities in interval funds that invest in senior-secured, sponsored middle-market loans.

The turmoil in the banking system earlier this year caused private-debt issuers to make concessions, including floating rates and improved covenants, which make this an attractive asset class.

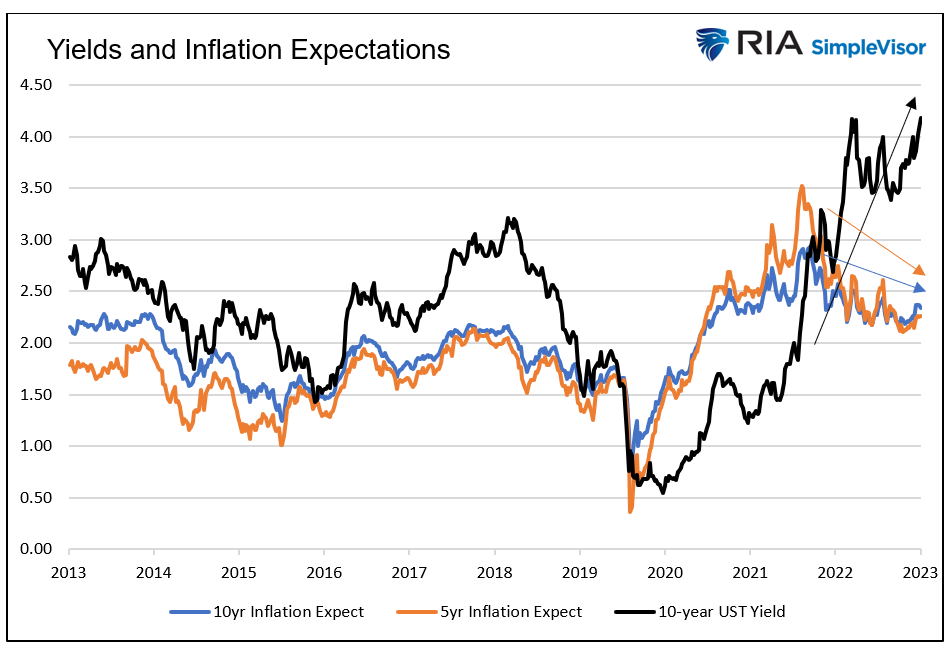

Fitch’s recent downgrade of the U.S. debt rating alarmed investors as the deficit and debt steadily increased. The downgrade sent 10-year Treasury bond yields above 4%, causing concern about America’s deteriorating financial condition.

Michael Lebowitz: Inflation, deficits and QT don’t mean higher yields

In the wake of the Federal Reserve’s annual gathering in Jackson Hole, Stephen Dover, Head of Franklin Templeton Institute, conveys one clear message: interest rates aren’t coming down anytime soon.

The world’s most powerful central bankers have vowed in unison to keep interest rates higher for longer if necessary to tame inflation.

Holding expectations low will help the battle against high prices.

Taxable municipal bonds may be an attractive option for investors in lower tax brackets, but there are things investors should know before making a decision.

Beaten-down US Treasuries are proving irresistible to some investors even after Federal Reserve Chair Jerome Powell said he’s ready to raise interest rates again to choke off inflation.

Jerome Powell has the bond market exactly where he wants it: lacking conviction as to the Federal Reserve’s next steps.

Surprised that the S&P 500 swung into the green Friday? Don’t worry. Just wait. It’ll fall again after the next opening bell.

At its annual summit in Johannesburg this week, the bloc of five emerging countries—Brazil, Russia, India, China and South Africa—announced plans to expand for the first time since 2010.

Federal Reserve Chair Jerome Powell said the US central bank is prepared to raise interest rates further if needed and intends to keep borrowing costs high until inflation is on a convincing path toward the Fed’s 2% target.

As brutal as it’s been for US bond investors, the math is finally turning in their favor.

Technology stocks are in trouble, with the buzz around artificial intelligence set to be overshadowed by the effects of higher-for-longer interest rates, according to Bank of America Corp. strategists.

It’s premature to call off a recession. Lower shelter costs will ease inflationary pressures. Treasury supply dynamics caught the market by surprise.

Longer-dated US Treasuries – those with maturities of 5 years or longer – continue to struggle. At best, coupon payments are keeping investors relatively flat.

The drop in US stocks on Thursday despite a bumper report from Nvidia Corp. shows the rally this year is “exhausted” and portends more declines to come, according to Morgan Stanley’s Michael Wilson.

Markets seem to be coming around to our Franklin Templeton Fixed Income CIO Sonal Desai’s view that the Fed will have to keep interest rates higher for longer, but now runaway fiscal deficits pose further upside risk to yields in the long term, she warns.

International stocks and the related exchange traded funds have accumulated bum reputations after lengthy spells of underperforming domestic equivalents.

The holy grail of stock investing is buying great companies on the cheap. Stock picker Peter Lynch plied a variation of that strategy to fame and fortune in the 1980s using his so-called PEG ratio.

An abstract interest-rate metric is dominating discussions across trading desks ahead of the Jackson Hole symposium, with investors wondering if Federal Reserve Chair Jerome Powell will weigh in, and bracing for further declines in US Treasuries if he does.

The first six months of 2023 were full of surprises for investors, not the least of which was a Nasdaq surge of 32% — its best first half since 1983. The S&P 500 Index gained nearly 16% for the first half, powered by mega-cap stocks.

Interest rates are the penalty you pay for purchasing something today instead of postponing consumption until tomorrow. They are also the reward you receive for saving and engaging in delayed gratification.

Central bankers generally believe in an abstract phenomenon known as the neutral real rate of interest, or r-star. It’s the inflation-adjusted rate that should prevail when the economy is balanced with price increases subdued and the labor market healthy.

The prospect of global interest rates remaining higher for longer is tipping the case for many investors to switch into bonds from stocks.

The heated debate on the threat posed by the boom in stock derivatives that expire within 24 hours is pitting two of Wall Street’s biggest banks against each other.

As the demand for faster, smaller, and more efficient electronic devices grows, so does the need for advanced semiconductor manufacturing techniques. Traditional methods have their limitations, and ASML’s mission revolves around transcending these boundaries.

In the current landscape, where bonds and stocks are experiencing positive correlation, it becomes even more important (if not critical) to incorporate additional diversification strategies to help mitigate portfolio risk and preserve portfolio balance.

Russia’s 2022 invasion of Ukraine and the ensuing war have prompted new and difficult questions for sovereign debt investors.

Entrenched long-term economic growth trends and low inflation, coupled with high and increasing leverage, all but ensure lower interest rates. This article defends that thesis and helps us better appreciate the bearish concerns weighing on bond traders.

Gold isn’t losing its allure, according to a dozen money managers who all told Bloomberg News they expect to maintain or raise their exposure to the precious metal in the coming 12 months.

What’s going on with the markets and the economy? Long-term Treasury yields are up substantially since last Fall while the stock market, after a big rally, has stumbled so far this month. Meanwhile, the real economy appears to continue to chug along – even accelerating!

With the path of least resistance for stocks seemingly lower for now, key to watch will be a stabilization in interest rate volatility and clarity on the path of monetary policy.

Nick Goetze discusses fixed income market conditions and offers insight for bond investors.

The US bond-market selloff resumed Monday, driving 10-year yields to a 16-year high, as the persistently resilient economy has investors positioning for interest rates to remain elevated even after the Federal Reserve winds up its hikes.

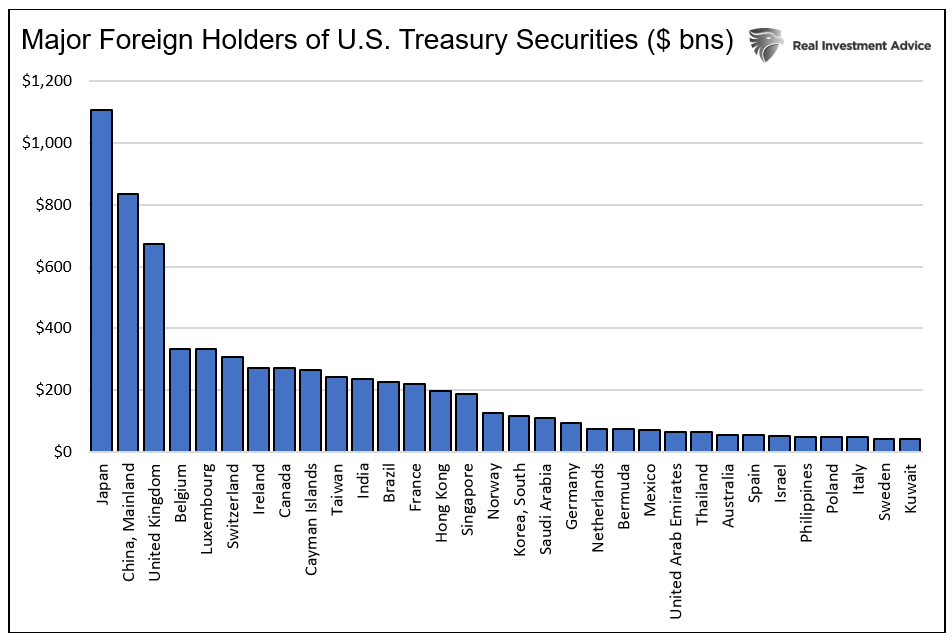

The government has issued an eye-watering $1 trillion in Treasury bills since the debt ceiling was suspended in early June. So far, the market hasn’t batted an eye.

The role of the human psychological cycle in driving stock and bond prices is well understood and pre-dates behavioural economics. There are elements that suggest we may be going through another period of ‘irrational exuberance’ as several long-term investors seem stuck in the mindset that ‘There Is No Alternative’ (TINA) to US equities.

Yields on 10-year Treasury notes have spent 18 sessions trading above 4% this year, but some doomsayers are ready to declare a permanent shift to a higher-yield regime. They attribute it to factors such as demographics, the looming clean-energy transition and large government deficits. And sure, that could be.