The holy grail of stock investing is buying great companies on the cheap. Stock picker Peter Lynch plied a variation of that strategy to fame and fortune in the 1980s using his so-called PEG ratio. It compares companies’ valuation, as measured by their price-earnings ratio, with expected growth to find stocks that offer the highest growth for the lowest price.

It’s harder to find overlooked stocks than it was in Lynch’s day because more people are looking for them — anyone with a smartphone has free access to extensive markets and financial information. The result of greater competition is evident in the numbers: Fast-growing or highly profitable companies are almost always the most expensive while the cheapest ones come with lackluster growth or thin profits.

Stock funds have replaced individual stocks in most portfolios, but the choice is the same. A basket of big US technology companies, for instance, offers huge profits at a high valuation while many smaller US and overseas companies are much cheaper but generally less profitable.

There’s an investment case for both groups — buying cheap stocks has been a winning strategy historically, and so has buying shares of highly profitable companies. Still, differences in valuation and profitability make stock funds difficult to compare. One way to solve that is with a variation of Lynch’s PEG ratio that substitutes profitability for growth. This PEP ratio, let’s call it, compares funds’ P/E ratio with their profitability, and like the PEG ratio, the lower the PEP ratio, the better.

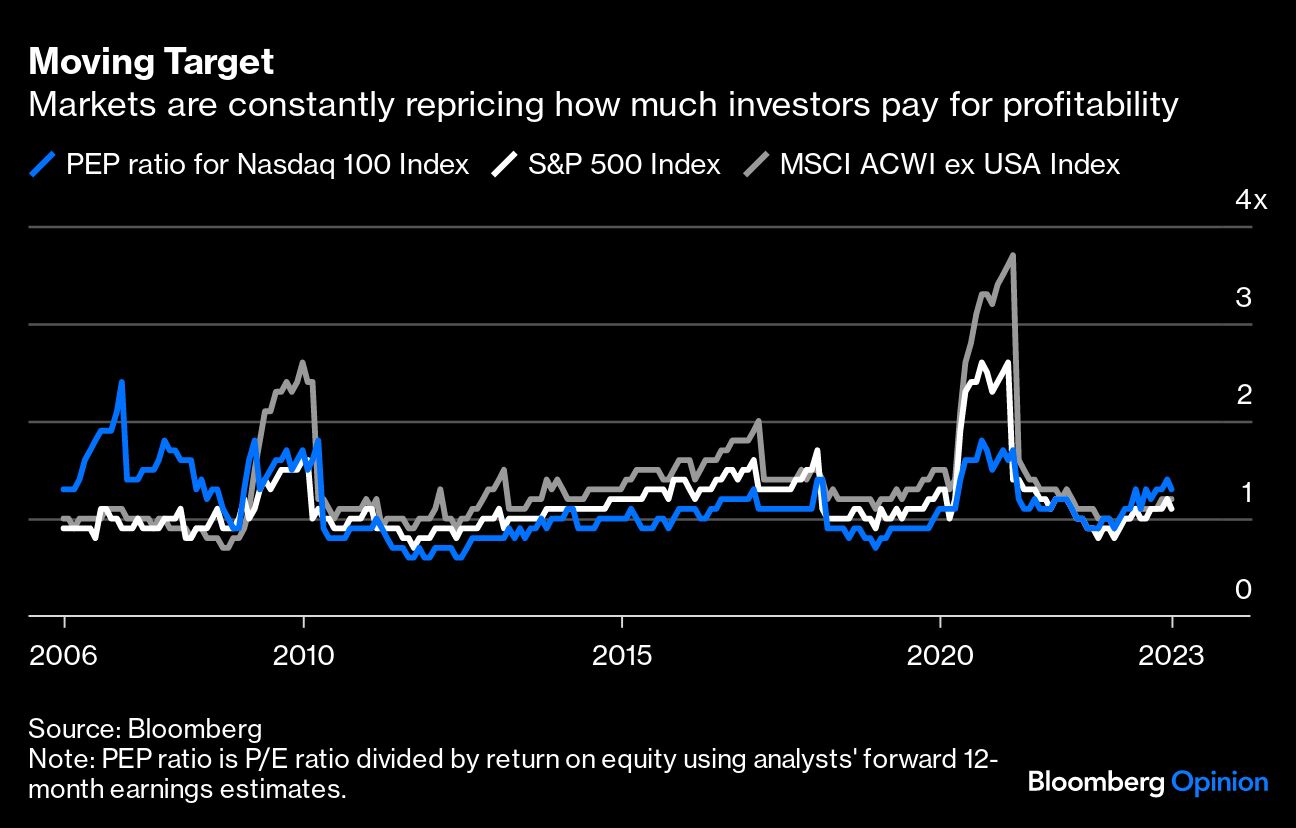

For example, based on analysts’ earnings estimates for the next 12 months, the technology-dominated Nasdaq 100 Index has a P/E ratio of 27 and a return on equity of 21%, which yields a PEP ratio of 1.3. By the same measure, the S&P 500 Index and the MSCI ACWI ex USA Index, which represents the global stock market excluding the US, have a PEP ratio of 1.1 and 1.2. Of the three, the Nasdaq 100 offers the lowest profitability for the price.

It’s not always that way because markets are constantly repricing. For much of the time since the 2008 financial crisis, the Nasdaq 100 had a lower PEP ratio than the S&P 500 and ACWI ex USA, a lead it gave up only recently.

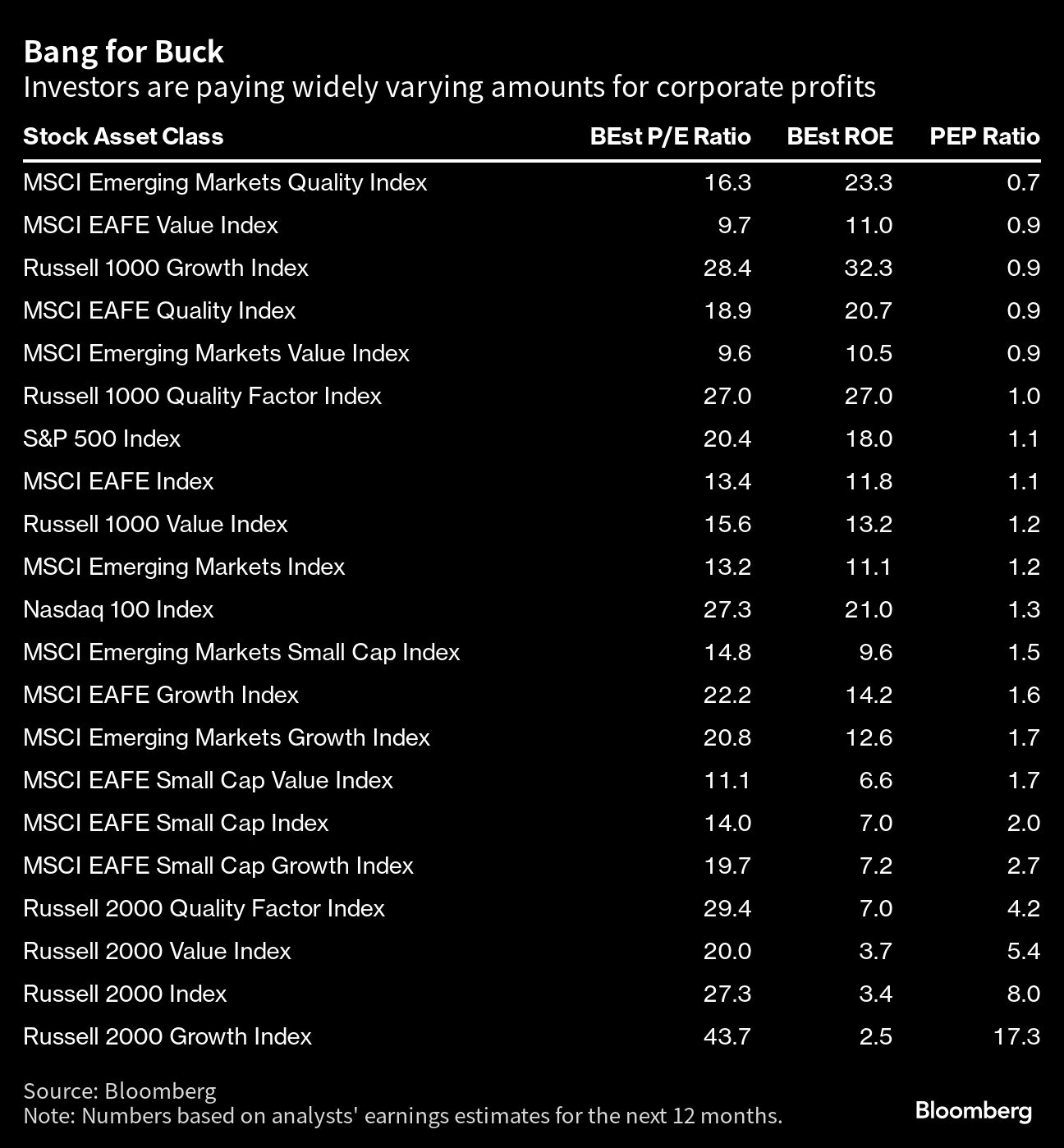

But those aren’t the only three choices. I compiled a list of stock asset classes that commonly appear in portfolios and calculated a PEP ratio for each one. The highest PEP ratio goes to US small-cap growth stocks, for which investors are paying 44 times forward earnings for a 2.5% return on equity, resulting in a ghastly PEP ratio of more than 17. The best bang for the buck belongs to high-quality stocks in emerging markets, which fetch 16 times earnings in exchange for a 23% return on equity, or a PEP ratio of just 0.7.

There’s not enough historical data across all stock asset classes to say anything empirical about the PEP ratio, but the available evidence around individual stocks suggests that low price and high profitability are a potent combination. In the US, shares of the cheapest and most profitable companies have been the best performers historically, outpacing the most expensive and least profitable companies by 9 percentage points a year over the past 60 years, including dividends, according to numbers compiled by Dartmouth professor Ken French sorting companies by price-book ratio and a variation of return on equity and weighting them by market value. The overseas data are shorter but tell a similar story so far.

The PEP ratio has another use. One of the problems with P/E ratios is that they can vary greatly depending on the measure of earnings. The S&P 500’s P/E ratio, for instance, is as low as 18 based on earnings estimates for 2024 and as high as 28 using an average of inflation-adjusted earnings during the past decade. The PEP ratio can also vary depending on the P/E ratio used, but the inclusion of profitability dampens the differences, better-allowing investors to compare PEP ratios across stock funds that use different measures of earnings.

So for those struggling to size up mighty US technology companies against lowly value stocks in emerging markets, give the PEP ratio a try.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar