The heated debate on the threat posed by the boom in stock derivatives that expire within 24 hours is pitting two of Wall Street’s biggest banks against each other.

After Goldman Sachs Group Inc. blamed the rise of zero-day options for the late-afternoon S&P 500 selloff seen on Aug. 15, Bank of America Corp. dubs the logic “largely misguided.”

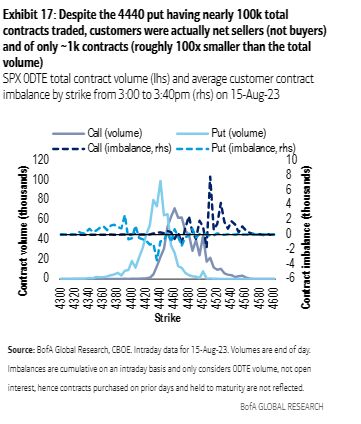

At the center of the disagreement: The precise role played by put derivatives that protect against equity losses with a strike price at 4,440, a level close to where the market was trading at that time.

In Goldman’s view, rising client demand for those contracts forced market makers on the other side of the transactions to abruptly hedge their exposures — ultimately leading to a sharp drop in share prices over a roughly 20-minute span.

BofA sees it differently. While trading in those puts added up to almost 100,000 contracts during the session, it was far from a one-way bet.

After breaking up flows into buy and sell orders, strategists including Matthew Welty found customers were net sellers of only 1,000 contracts. Theoretically, that positioning amounted to a bullish stock wager that would have required market makers on a mission to balance their books to snap up shares — rather than, as per Goldman, sell.

“As the S&P sold off market maker hedging needs for the 4,440 put were likely small and in the direction of pushing markets up (not down), exactly the opposite effect of what was claimed,” Welty and his colleagues wrote in a note Tuesday. “High-frequency positioning data from the exchange suggests this is more of a good story than reality.”

Source: BofA

A Goldman spokesperson didn’t return an email seeking comment on the diverging view from BofA.

Options with zero days to expiration, or 0DTE, are in the spotlight again as their trading has spiked to record in August, sparking concerns that the fast-twitch investment tool may have contributed to the S&P 500’s worst monthly decline in 2023.

More than a year after 0DTE contracts became available for S&P 500 traders for every weekday, debate goes on about its impact on the marketplace. Analysts such as JPMorgan Chase & Co. quant guru Marko Kolanovic warn their popularity risks reprising past shocks such as the 2018 Volmageddon episode, while others see just another example of doomsayers stirring up fear over the latest market evolution.

The BofA team has for months viewed worries over 0DTE as somewhat overblown. In the latest note, they attributed last week’s equity pullback to other factors such as selling from rules-based traders and renewed pressure from higher bond yields.

Still, while disagreeing with Goldman on the market dynamics on Aug. 15, they also said the recent spike in options volume alongside falling share prices is probably not a coincidence.

“The record 0DTE volume has disproportionately (and increasingly) favored puts over calls, a phenomenon which predates the market selloff starting at the beginning of August,” BofA strategists wrote. “We are not saying 0DTEs can‘t exacerbate intraday fragility,” they added. “But the impact 0DTEs may have had last week was clearly greatly overstated.”

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 a.m. ET. Click here to register.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Lu Wang