Holding expectations low will help the battle against high prices.

I love grocery shopping, but others hate grocery shopping with me. I like to take my time going through each aisle, developing recipe ideas. I’ll often double back to get ingredients, or to reshelve items after I have changed my mind. I always start with a list, but I rarely stick to it. Anyone who dares to accompany me quickly grows frustrated with my supermarket ADHD.

For the past three years, there has been another method to my supermarket madness. Food prices have skyrocketed: while there has been some moderation of late, groceries in the U.S. are still 25% more expensive than they were prior to the pandemic. It’s gotten to the point where I expect more markups every time I shop, and I feel I have to scour the shelves even harder to stay within budget.

The anticipation of higher prices can be very dangerous for an economy, as those expectations can become self-fulfilling. Fortunately, inflation expectations have remained reasonably well-behaved in spite of the price level surges we’ve endured over the past two years. This is an especially fortunate outcome for central banks around the world.

Economists have long feared rising inflation expectations. When we anticipate higher prices, the theory goes, our demands for wages to keep pace with costs of living can lead our employers to charge more for goods and services. The desire to avoid that kind of feedback loop has informed monetary policy for several decades.

Measuring inflation expectations is far from a precise science. Indications can be taken from the financial markets: comparing yields on fixed rate and inflation-protected bonds produces an implied forecast for inflation over a given period of time. A number of countries also take surveys of inflation expectations, asking respondents how they believe prices will evolve over different terms.

Readings from the two sources can be somewhat volatile, clouding the picture. And neither has a perfect track record of foreshadowing what the price level will actually do.

Managing the psychology surrounding inflation is not easy. Central banks have tried to steer perceptions with their actions, leaning against unwanted price level increases with tight monetary policy. This orientation has been formalized over the last thirty years by the advance of inflation targeting. The trend began in New Zealand, spread to Europe and finally landed in the United States in 2012.

It is hard to understate how important inflation targeting has become to central banks. They view it not only as a way to anchor expectations but as an operating model that promotes long-term growth and aids market function. Federal Reserve Chairman Jerome Powell has often said that inflation discipline and maximum employment are not conflicting objectives and that the pursuit of price stability does not favor one community over another. Achieving the target is considered a measure of central bank credibility.

It seems like a long time ago, but prior to the pandemic, inflation was running below targeted levels. (Almost all major economies seek 2% inflation over some interval.) To address the situation, central banks began offering forward guidance that their interest rates would remain low for a long time, a step which was intended to promote borrowing. In September of 2020, the Federal Reserve adopted “flexible average inflation targeting,” which allowed periods of higher inflation to offset periods of low inflation. Unfortunately, the Fed got a lot more than it bargained for.

We’ve covered the roots of post-COVID inflation on a number of occasions. Excesses of demand, partly the product of government support, collided with supply limitations in the markets for goods and labor. The consequences initially appeared isolated to a few goods and services but quickly became more deeply entrenched. Inflation transitioned from too low to far too high.

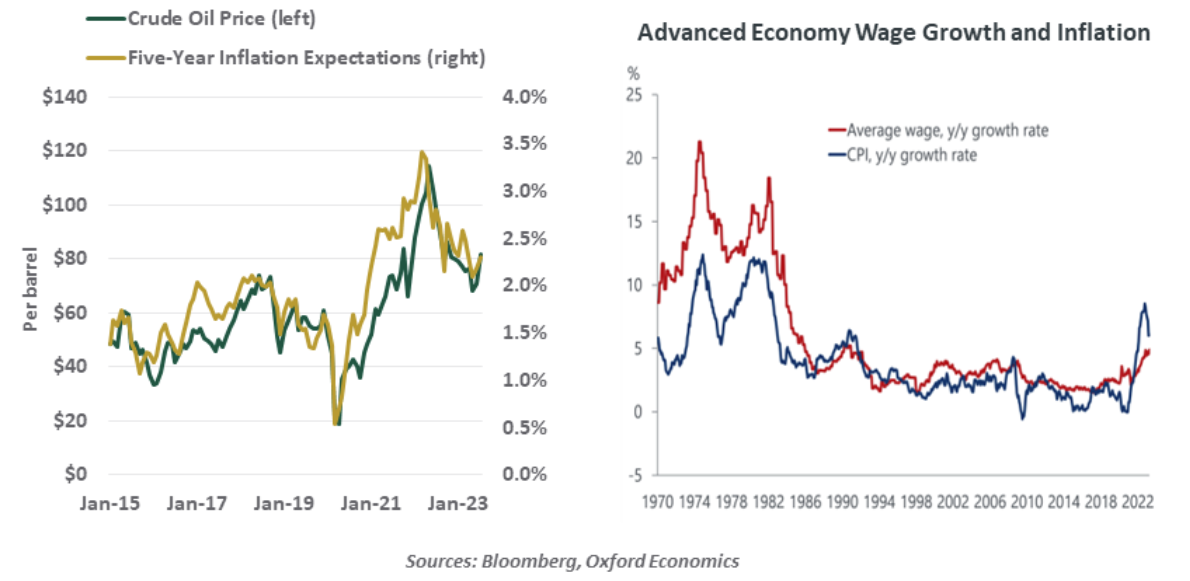

Measures of inflation expectations increased in sympathy with the price level. Market measures in the U.S. and continental Europe moved from about 1% to about 3% for the five-year horizon. Surveys of inflation one year forward peaked at more than 6%. Alarmed, central banks began a tightening phase that continues to this day.

Actual inflation remains too high for comfort. Core measures have moved down more slowly, and our good fortune with falling energy prices has ended. The latter is doubly worrisome, as inflation expectations are closely correlated with petroleum prices, as experienced at the gas pump.

But much to our surprise and relief, inflation expectations have receded. While the pace of pay increases has risen, a wage-price spiral has yet to form.

One potential explanation for this development is the concept of “rational inattention,” which was featured in Fed Chair Jay Powell’s keynote at last year’s Jackson Hole conference. Given limited time and capacity for dealing with complicated problems, human beings tend to pay more attention to things that are pressing and relegate others to a mental parking lot.

For the longest time, inflation wasn’t one of those things we had to worry about. When it began to rise, central banks were slow to react; but the initial delay was followed by an aggressive response. That action, and the recent decline in inflation, may have headed off a tendency of households and investors to pull inflation out of the parking lot and back onto the street.

Central banks are certainly not likely to jeopardize their good fortune by relaxing their inflation targets. There has been a growing chorus calling for an increase from 2% to 3%, to avoid the economic pain that might result from crossing the final few yards. But what seems like a small change can be significant over time, especially if it results in a commensurate change in inflation expectations.

These days, my meandering in the store is less about being a foodie and more about being frugal. I’ve traded down from beef to beans and from Kerry Gold to Country Crock. That is my way of taming inflation.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 a.m. ET. Click here to register.

© Northern Trust

Read more commentaries by Northern Trust