Beaten-down US Treasuries are proving irresistible to some investors even after Federal Reserve Chair Jerome Powell said he’s ready to raise interest rates again to choke off inflation.

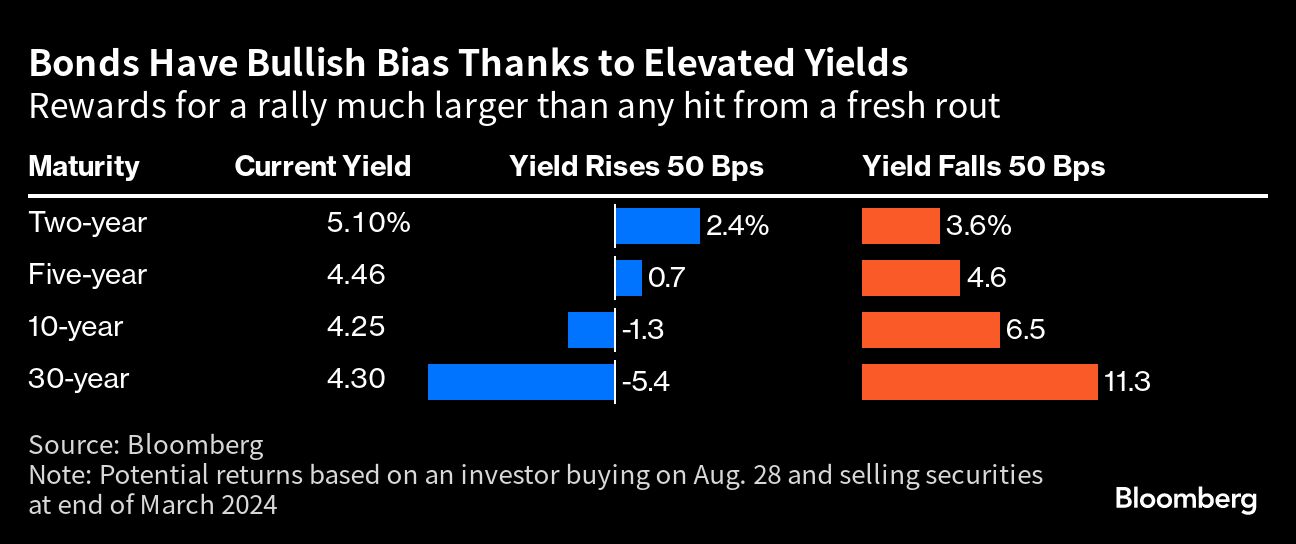

Western Asset Management says bonds are set to outperform due to attractive yields, while JPMorgan Chase & Co. is keeping its bullish bets on fixed income despite Powell’s warning at Jackson Hole Friday. Even fresh Fed hikes won’t deliver bond losses steep enough to outweigh the income from the highest yields since 2007, the bulls argue.

“There may be considerable value in the bond market at current yields,” John Bellows, a fund manager at Western Asset in Pasadena, California, wrote in a client note. “Further declines in the inflation rate will eventually allow the Fed to return real interest rates to more normal levels.”

Benchmark 10-year Treasury yields were 2 basis points lower at 4.22% at 10:23 a.m. in London, having climbed to a 16-year high last week as markets grew less optimistic about a potential Fed pivot to cutting rates. Speaking at Jackson Hole, Powell acknowledged inflation had slowed thanks to tighter monetary policy but cautioned the process “still has a long way to go.”

Treasuries have handed investors a loss of 1.3% in August, heading for a fourth month of declines, according to a Bloomberg index.

Treasury yields at current levels suggest the worst of the rout is probably done, according to money manager James Wilson at Jamieson Coote Bonds Pty. in Melbourne.

“We are very confident we are close to the top in yields,” he said. “Rates are at restrictive levels, but the lagged effects of monetary policy mean that it’s hard to know when, and by how much, rates will trigger a slowdown to growth.”

JPMorgan is also bullish.

“With yields near their cycle highs, valuations somewhat cheap, and next week’s data likely to show further easing in labor markets, we remain holding tactical longs in 5-year Treasuries,” strategists including Jay Barry wrote in a note published Friday.

Bearish Funds

Not everyone views Treasuries as a buy.

Hedge funds boosted their bearish Treasury bets just days before the Jackson Hole symposium. They added net short positions across the curve from two-year futures to ultra-long securities, according to data from the Commodity Futures Trading Commission.

Some of those positions may be linked to what is known as the basis trade — a strategy seeking to profit from differences in the prices between cash Treasuries and corresponding futures.

What Bloomberg’s Strategists Say...

“Powell also did not go out of his way to rule out rate cuts. Ultimately, he signaled that the Fed can afford to proceed ‘carefully’ — a management style he shares with one of his most famous predecessors, Alan Greenspan,” Anna Wong, chief US economist.

Investors “need a clearer trajectory for rates,” said Kellie Wood, a fund manager at Schroders Plc in Sydney. “We have been cautious on adding to rates here on the view that cuts continue to be priced out in a higher-for-longer environment, which would see the five and 10s underperform.”

While hedge funds increased their bearish positions, real-money investors are betting Treasuries will rebound. Asset managers added to net long positions in 10-year Treasury futures in the week to Aug. 22, the CFTC data also showed.

“Investors have wanted a chance to lock in compelling yields since 2008,” Gautam Khanna, a money manager at Insight Investment in New York, said before the Jackson Hole event. “So they should seriously consider taking this opportunity to increase allocations to intermediate and longer-duration US fixed-income assets.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Ruth Carson, Garfield Reynolds