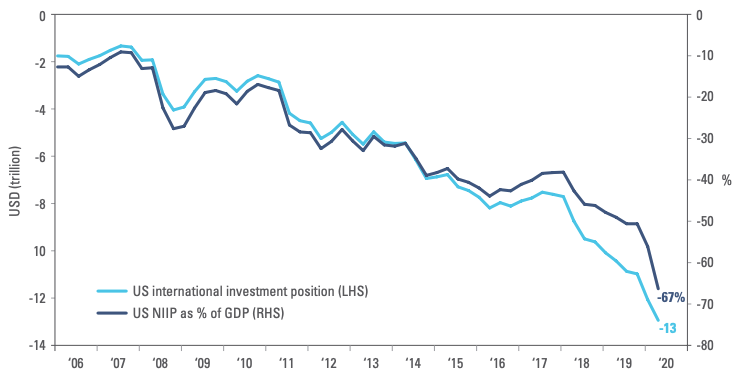

We are in a debt trap. Our political process can’t reduce spending and/or raise taxes enough to balance the budget, so the debt grows and grows. As it does, paying the interest plus the accumulated debt load pulls more capital away from more productive uses. This depresses economic growth, thereby generating even more spending and debt.

Actual third-quarter earnings may be less important than what business leaders say about their expectations.

Given current low yields, some investors wonder whether bonds can continue to provide diversification in a portfolio. Here’s why those fears may be overblown.

Euro-area countries were struggling to achieve growth and inflation even before the coronavirus pandemic. Now global lockdowns and trade disputes have compounded their problems. Still, we believe euro fixed-income markets offer active investors attractive opportunities and worthwhile income.

I recently did a search of the life and health insurance subsector and came up with 25 names that I considered the highest quality in the overall subsector. All of them carried investment grade credit ratings of BBB+ or better – except for one.

In his latest memo, Howard Marks walks readers through the unusual characteristics of this year’s economy; the impact of Covid-related monetary and fiscal policy actions, including low interest rates, on today’s markets; and the possible ramifications of the Fed/Treasury’s rescue efforts. What does it all mean for investors who face an environment marked by some of the lowest prospective returns in history?

There’s more consensus than usual over the likely winner of the U.S. presidential election. After that, there’s plenty of disagreement on strategies to wager on an election that’s been flashing warnings of chaos ahead in volatility markets.

Single-premium immediate annuities (SPIAs) can deliver superior retirement outcomes by reducing sequence-of-return and inflation risks if a portion of the monthly payments are systematically invested in equities.

The Investment Company Act of 1940 contains a loophole providing institutional investors an advantage over individual investors that some are using to the detriment of closed-end funds and their retail investors.

We compare fixed annuities to other safe investments, such as CDs and Treasury securities, to better understand whether they provide attractive risk-adjusted performance and are a reasonable alternative for risk-averse investors.

Noise levels are likely to remain elevated in the run-up to – and possibly in the immediate aftermath of the upcoming US presidential election, but the post-election outlook should prove positive for EM assets by ushering in a period of more positive risk-sentiment, a long period of low US rates and a lower Dollar.

The environment is one of many sets of regulations under consideration.

The transportation sector in the municipal bond market faces significant headwinds as a result of the COVID-19 pandemic.

High-yield bonds can generally offer more income in a very low-interest-rate world. However, if the economic or stock market outlook deteriorates, it could be a bumpy ride.

The pandemic has amplified four long-term macroeconomic disruptors, and fiscal policy – a key swing factor – may hold the key to upside or downside surprises. Read our long-term outlook and learn implications to consider when investing.

The S&P 500 SPX and Nasdaq NASD have recently hit a series of fresh all-time highs and the Dow DJIA now sits less than 2% off of its all-time high which has many people wondering if the market is overbought and due for a correction.

Whether you’re focused on improving risk management, pursuing sharper business-development strategies, or enhancing M&A outcomes, data analytics will improve your RIA’s overall success.

The U.S. economy improved significantly this quarter, but investors continue to face several serious risks. In late September, confirmed COVID-19 cases were rising worldwide, and the pandemic may intensify as winter approaches. A combative U.S. presidential election looms.

Can bonds continue to play defense and provide income when yields are at historic lows? We think so.

I will try to make the case for a much slower recovery thus much higher debt by 2030. Note first, I’m not saying there will be no recovery. I am simply postulating it will look like the slow recovery from the Great Recession, unless the government makes it worse, which is a nontrivial possibility.

While the US economy has been staging a strong recovery from the COVID-19 pandemic, the challenge is far from over, says Franklin Templeton Fixed Income CIO Sonal Desai. She says the tug of war between the virus and the economy seems likely to continue until an effective vaccine is made available at scale.

Policy will continue to be carefully calibrated as China walks a tightrope between supporting growth and maintaining financial stability.

The fastest, most economically destructive recession is now in investors’ rearview mirrors. CIO Larry Adam shares his perspective on the unfolding recovery.

Despite a September slump, the S&P 500 and NASDAQ wrapped up the third quarter with gains of 8.47% and 11%, respectively.

What will a Trump or Biden win mean for munis? From taxes to infrastructure, the candidates differ—sometimes dramatically—on policy.

Recent history suggests that low—and even negative—yields don’t eliminate the offset to risk assets provided by government bonds.

As economies reopen from COVID-19 lockdowns, there have been fundamental shifts to daily life and work, as well as the investment landscape.

It's a new cycle for the economy, but some asset classes look decidedly late cycle in terms of valuation. What might this mean for markets through the remainder of the year?

A basket of emerging market bonds may offer the same appeal investors have long sought from U.S. Treasuries.

Even as markets were rocked by uncertainty as the coronavirus lockdowns began, the seeds of stability were sown in the massive fiscal and monetary policy response.

The legendary bond investor and former Navy signal officer remains wary of collateralized loan obligations even as prices start to recover.

In the revised edition of The Incredible Shrinking Alpha, Larry Swedroe and Andrew Berkin make the case that investors are better off choosing passive investments because markets have become more efficient as managers became more skilled.

This article explores the trade-offs associated with the decision to delay an annuity purchase – in particular the interaction between changes in bond yields and assumed portfolio rates of return, and the impact of mortality improvement.

This “exodus,” as some are already calling it, may end up being among the biggest in U.S. history, or at least the biggest since the 1950s and 60s. A record 27.4 percent of homebuyers sought to move out of their metro areas in the second quarter, according to Redfin data.

Global stock markets seem to be defying the reality of recessions this year. Despite recent volatility, we think market gains for the year are more rational than perceived, given the powerful impact of stimulus and low rates on stock valuations.

The United Kingdom officially left the European Union in January of this year, but issues remain in the Brexit saga, namely trade relations. David Zahn, our Head of European Fixed Income, weighs in on the odds no deal will be reached by year-end—and the market implications.

Sierra Mutual Funds CIO Terri Spath covers the current state of the markets, and gives three possible ways to participate in investment returns while keeping a close eye on risk.

Many investors are attempting to justify higher stock “valuations” because interest rates are at historical lows. I would agree that lower interest rates could affect “market valuations” based on the simple law of supply and demand. The concept is simple, when fixed income offers lower returns it logically stimulates more demand for equities where higher returns can be found.

A brief monthly update on what's happening in the municipal bond market.

The COVID-19 pandemic has been devastating for Brazil, but heavy government spending and monetary policy easing have helped bring some stability to the economy.

Markets have been walking a fine line, with a still-struggling economy on one side and hopes for a COVID-19 vaccine breakthrough on the other. Heading into the fourth quarter, there are both encouraging signs and cause for caution.

Ed Perks and Gene Podkaminer of Franklin Templeton’s Multi-Asset Solutions team discuss the attractions of alternative assets that can offer natural portfolio diversification. Over a longer-term horizon, they continue to believe global stocks have greater performance potential than global bonds, or alternatives, but this outlook will not be reached along a smooth path.

Markets may press even higher this year, but some areas may fall behind.

In recent years, global equities had slightly outpaced market forecasts for lower equity returns. Then the COVID-19 pandemic hit the global economy, putting an end to the 10-year bull market. Equity markets have now started to recover, but the pandemic introduced and exacerbated challenges that we expect to subdue financial market returns over the next five years.

Another market high, with expectations for a “V”accine-shaped recovery.

Overall, EM IG bonds represent a great opportunity for investors seeking to monetise the EM risk premium with moderate volatility in a world, where higher yielding IG-rated securities are increasingly difficult to come by.

The risk of a “no deal” Brexit and the potential economic harm that accompanies it increased last week.

In a challenging year dominated by the COVID-19 pandemic, the municipal market is recovering on the strength of unprecedented federal support.

A strong understanding of market dynamics exposes some valuable gems. When the time comes, these stocks will make playing defense productive.

The U.S. stock market hit pause in early September, as investors took a harder look at market overconcentration and frothy sentiment. Meanwhile, global economies may be entering a new phase, and the Federal Reserve’s newly announced inflation policy is likely to keep U.S. rates lower for longer.