Repositioning SPIAs in Retirement

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Single-premium immediate annuities (SPIAs) can deliver superior retirement outcomes by reducing sequence-of-return and inflation risks if a portion of the monthly payments are systematically invested in equities.

Consider that in the context of a number of contributors to Advisor Perspectives and elsewhere who have written favorably about SPIAs, including Michael Edesess, Allan Roth, and Joe Tomlinson.

Retirees are not getting the message.

SPIA sales are languishing: According to LIMRA, sales grew a meager 2% in 2019 and fell dramatically in 2020. One reason has been the steady decline in long-term interest rates; annuity payments per dollar of deposit have shriveled. With paltry payouts, clients may shy away from SPIAs. Limited liquidity and worries about premature death are further disincentives.

This article offers a different perspective on integrating SPIAs into retirement plans. I present an implementation that links the relative attractiveness of longevity credits in a low-interest rate environment to the mitigation of sequence-of-return and other retirement risks through a rising equity glide path.

Increasing role of longevity credits

Consider the composition of annuity payments. Insurance companies collect the premiums and largely invest them in bonds. SPIA payments reflect:

return of principal + interest + longevity pooling – insurance company charges

The formula illustrates why, as interest rates decline, the relative contribution of longevity insurance in annuity payments increases. Even though the payments are lower, the advantage of a SPIA over a bond portfolio is greater. Michael Finke has an illustration here.i

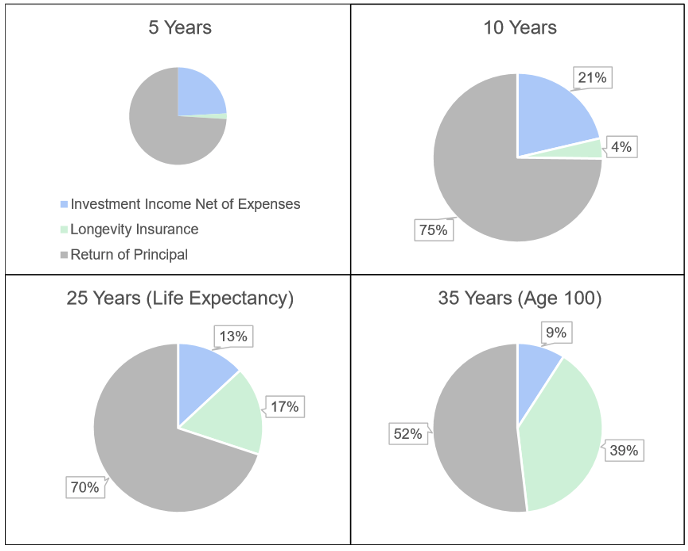

But compared to a bond investment, the longevity credits only meaningfully kick in if the client actually experiences longevity. SPIA returns increase with time. To illustrate this, I decomposed a hypothetical, life-only SPIAii for a 65-year old female into the above components. Longevity insurance only accounts for 4% of the cumulative payments in the first 10 years. Three quarters of the money comes from return of principal. However, after 25 years (life expectancy) longevity insurance accounts for 17%, and at age 100 (about 12% survival probability) it accounts for 39% of cumulative payments.

Composition of cumulative SPIA payments (Female Aged 65)

In addition to mortality risk (early death), a SPIA is exposed to the risk of unexpected inflation and to interest rate risk (while there is no reduction in the payments if interest rates rise, the client is locked into a below-market rate and faces opportunity costs.)

Is there a way to mitigate these risks in the context of a retirement plan?

Rising equity glide path

In 2013, Michael Kitces and Wade Pfau made a splash with the claim that an increasing allocation to equities during retirement made it less likely that a retiree would run out of money.iii Other researchers refuted the findings using different assumptions. I don’t know how much acceptance the concept has gained among practitioners; for example, to my knowledge, no target date fund took up the idea. One could see how implementing such a strategy would give clients pause – convincing those in their 70s or 80s to shift their portfolio from “safe” fixed income to “risky” stocks could be challenging. Nevertheless, the idea holds appeal when implemented slowly and consistently.

A simple strategy

I look at a simple strategy that implements a rising equity glide path by harvesting SPIA longevity credits and investing them in equities. In this approach, a retiree purchases a SPIA and invests the periodic payments in equities. Instead of thinking of the SPIA as a “floor” to fund “necessary” retirement expenses, it is positioned as a retirement risk-mitigation tool that provides attractive upside.

The source of funds for purchasing the SPIA could be the equity portfolio, with a view to reducing risk, or it could be the fixed income portfolio for clients who are at their target allocation. In either case, the SPIA converts some of the recent strong market performance into a guaranteed payment stream, albeit at very low prospective interest yields. In either case, the intent is not to use the annuity to fund near-term living expenses.

The strategy highlights the benefits of SPIAs while addressing some key risks:

- It mitigates sequence-of-return risk. Because the strategy starts a new equity accumulation period when the client is already retired it offsets exposure to sequence-of-return risk.

To illustrate this point, I compared investing annual payments in stocks to investing a lump sum. I assumed a $100,000 deposit and the same generic quote for a 65-year old female as in the decomposition above, providing annual payments for life of $5,507.

I compared portfolio accumulation using a basic Monte Carlo simulation (10,000 scenarios, annual arithmetic returns of 7%, standard deviation of 17%.) Not surprisingly, investing the lump sum provides a greater accumulation most of the time. However, in about 15% of scenarios with low long-term returns or early negative returns – precisely the scenarios which retirees are concerned about from a sequence-of-return perspective – the SPIA strategy accumulates more than a lump sum investment after 20 years.

Students of dollar-cost averaging (DCA) will see the analogy. In most DCA simulations, investing a lump sum outperforms DCA; it does not when equity returns are low and/or the sequence of returns is unfavorable.

- It addresses, but does not eliminate, inflation risk. One concern with SPIAs is that the payments do not increase with inflation. There are no true inflation-adjusted income annuities available; the one company that offered them reportedly stopped. By investing periodic payments in stocks, clients may benefit from the tendency of equity returns to best inflation.

- It insures against longevity risk. This of course is a fundamental benefit of SPIAs. Because longevity credits become more powerful and returns increase as the annuitant ages, the longer the strategy is in place, the greater the probability that it will match or outperform the lump-sum investment strategy.

- It preserves flexibility. SPIA payments as well as the accumulated equity balance are always available for consumption if the remainder of the portfolio is insufficient to support ongoing expenses. The “safety blanket” aspect of the annuity remains intact.

- It may provide tax benefits. If the SPIA is purchased with taxable money, the taxable portion in our example is about $500 a year for the first 20 years (after which the full payments are taxed). This amount compares favorably to the taxable interest earned if the deposit were instead invested in long-term bonds.

Mental accounting

There is clearly a good dose of mental accounting involved here, not unlike various “bucket” strategies recommended by many advisors. The economic benefits of the strategy are those that are standard for a SPIA (harvesting of longevity credits and insuring against longevity risk) and include the gradual increase in equity risk during retirement and potential tax deferral benefits. As an alternative, one could use the SPIA for basic living expenses and gradually increase the equity allocation in the portfolio for a similar effect. However, by linking the SPIA purchase to the equity contributions, it is easy to systematize implementation of the strategy and illustrate its benefits to clients.

Interest rate risk

The biggest caveat to the strategy is that it exposes the retiree to substantial interest rate risk. Investors who opt for bonds in the current environment are able to mitigate this risk by keeping duration relatively short. The flat yield curve means they won’t give up much in yield compared to longer-duration bonds. But SPIAs are inherently long-duration – a sharp rise in rates can negate the benefit of longevity credits. The question for retirees is whether reducing longevity and other retirement risks is worth taking on interest rate risk.

Peter Hofmann, CFA, is with Fieldmark Advisors, a registered investment advisor based in North Salem, N.Y.

i I am also grateful for an email exchange with Wade Pfau that helped me think through this concept.

ii Assumptions: 65-year old healthy, non-smoker female; longevity interpolated from American Academy of Actuaries and Society of Actuaries, Actuaries Longevity Illustrator, http://www.longevityillustrator.org/; annual payments based on a generic quote from Blueprint Income; constant investment yield of 2.5%; insurance company expenses 1% of account value plus $50 per year.

iii See Kitces and Pfau (2013)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All