Suppose you are retired, or soon-to-be retired, and you have no reason to leave a bequest. You have no offspring, or they are financially independent – or you want them to be – and you have no charities to which you wish to leave money. You just want to assure yourself of as much income as possible while you are alive. What is your best course of action? My research shows it’s almost impossible to beat an annuity1.

The comparison

In an August 14, 2012 article in Advisor Perspectives, Joe Tomlinson showed that annuities have been an extremely safe investment, and that there is no reason to believe they will not be in the future. Let us therefore, tentatively, say that they have a 99% chance of delivering their promised income (the only risk being the failure of the insurance company and the lack of adequate government funds to pay annuitants).

In this article I explore comparably safe, “safe withdrawal strategies” from a stock-bond portfolio, in order to compare the lifetime income they provide with the lifetime income from an annuity purchased with the same initial investment.

The annual payout rates on the annuities used in the comparison were supplied by immediateannuities.com and checked against numbers provided by CANNEX. The rates used were drawn from the Immediateannuities.com column in Table 1, and were obtained a few weeks ago.2

The question is, what safe withdrawal strategy from a stock-bond portfolio maximizes lifetime income, while providing 99% certainty that the money won’t run out during the investor’s lifetime? And how does its total income compare with an annuity’s?

Many strategies have been proposed as “safe withdrawal strategies,” and many more are possible. Exploring every conceivable strategy to see which one maximizes lifetime income while offering a 99% chance (or any other strong chance) of not running out of money is a task I will not attempt.

I will test only two strategies. One was established as a norm by William P. Bengen in a seminal article, “Determining Withdrawal Rates Using Historical Data,” in the October 1994 issue of the Journal of Financial Planning. The strategy is to set a dollar number as a percentage of the investor’s initial portfolio to be withdrawn in the first year, and then to increase that dollar number for inflation each year thereafter.

For example, suppose that the initial investment is $1 million and that the withdrawal percentage is 4%, so that the first year’s withdrawal is $40,000. Suppose that inflation in the subsequent year is 5%. Then the withdrawal in year 2 would be five percent greater than the initial $40,000, or $42,000.

Bengen concluded by testing the strategy against historical returns and asserting that an initial withdrawal rate of 4% would be “safe.” More recent articles such as one in 2013 by Michael Finke, Wade Pfau, and David Blanchett have argued that a 4% withdrawal rate is too high to be considered “safe” in the current low-interest environment.

But because the Bengen safe withdrawal rate approach uses an unchanging percentage of (the inflation-adjusted value of) starting assets, it fails to withdraw more in scenarios in which assets increase rapidly. Thus, it often leaves money on the table.

My research finds that another withdrawal strategy, which I will call the high withdrawal strategy (HWS), increases lifetime income compared to the Bengen strategy, while still adhering to the “safety” requirement. That strategy is to set both an initial withdrawal percentage, call it p, and a lesser, minimum withdrawal percentage, call it p0, and to withdraw p percent of the current value of assets each year (rather than the inflation-adjusted value of initial assets), subject to a minimum of p0 percent of the inflation-adjusted value of starting assets.3 This strategy sets a minimum annual withdrawal, while allowing it to be greater when assets are greater.

The HWS strategy produces substantially more lifetime average annual income than the Bengen strategy. The pattern of withdrawals tends higher over time, however, so that the final withdrawals are significantly greater than the initial withdrawals, even adjusted for inflation. But since even the initial withdrawals are larger than they are with the Bengen strategy, the HWS strategy is better than the Bengen strategy for producing lifetime income.4

Methodology

I tested the two strategies against annuities using two simulation methods: by simulating random sequences of annual stock-bond portfolio returns with a standard Monte Carlo generating process, and by random sampling of past stock and bond returns. (Details of the simulations are in the endnotes.5,6)The two methods produced results that were similar enough to not report both. Therefore, I will report the results with Monte Carlo simulation. Coincident inflation rate sequences were also generated.7 Random ages at death were generated for each simulation using actuarial mortality tables provided by Joe Tomlinson. It was assumed that all investors and annuitants were initially age 65.

For each simulation, withdrawals were made each year in accordance with the withdrawal strategy used in that series of simulations. Wealth was then updated using the stock-bond portfolio return generated for that year. Note was made of whether wealth went to zero before death (failure of the withdrawal strategy to sustain income), and the age at death. Running totals of income over the simulated investor’s life were kept in the process, then averaged at death to obtain an average annual income for each simulated life. Average annual incomes were then averaged across all simulations, and the percentage of failures of the withdrawal strategy was calculated.

After testing against various stock-bond mixes, a 60%/40% mix of stocks and bonds was used for the stock-bond portfolio because testing showed that it produced the highest lifetime average incomes compared to other allocations.

Results

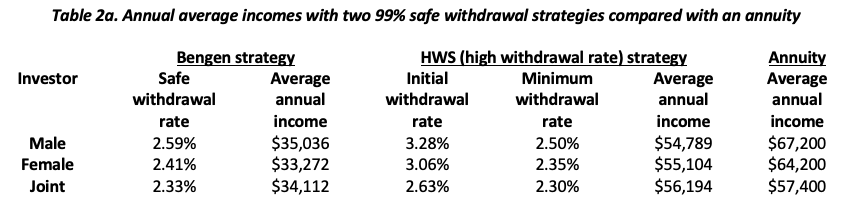

Safe withdrawal rates were explored for male investors, female investors and joint investors (couples). In every case, withdrawal rates that were “safe” at the 1% failure level yielded much lower lifetime average annual incomes than the corresponding non-inflation-adjusted annuity (see Table 2a).

For male investors using the Bengen strategy, the safe withdrawal rate was only 2.59% in order to keep the failure rate below 1%. The lifetime average annual income (in nominal dollars) was only $35,036 compared to $67,200 for the annuity. For female investors, the safe withdrawal rate was 2.41% with a lifetime average annual income of $33,272 compared to $64,200 for the annuity, and for joint investors, the safe withdrawal rate was 2.33% with a lifetime average annual income of $34,112 compared to $57,400 for the annuity.8

With the alternative HWS withdrawal strategy, lifetime average annual incomes were higher, but still less than for an annuity. For male investors, an initial withdrawal percentage of 3.28% with a minimum withdrawal percentage of 2.5% produced lifetime average annual income of $54,789 compared to $67,200 for the annuity. For females, an initial withdrawal percentage of 3.06% with a minimum percentage of 2.35% produced average annual income of $55,104 compared to $64,200 for the annuity, and for joint investors, an initial withdrawal percentage of 2.63% with a minimum of 2.3% produced average annual income of $56,194 compared to $57,400 for the annuity.

Lowering the minimum withdrawal percentage in the HWS strategy increases average annual income, but at the risk that some annual withdrawals will be too low to meet basic expenses. The minimum should be set at the minimum level required to maintain a safety net.

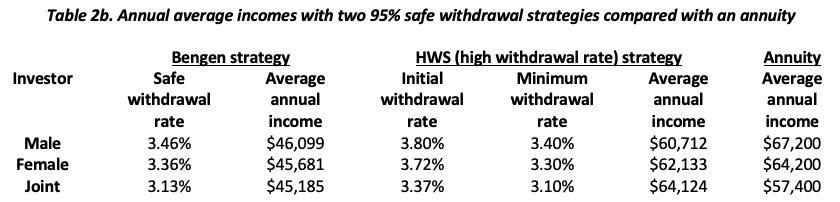

What if a 5% failure rate is comfort enough?

Suppose that instead of a 1% failure rate, a 5% failure rate is assumed. Either the investor believes that the annuity provider is not 99% safe but only 95% safe, or the investor is effectively indifferent between 99% and 95% safety.

Under this assumption, minimum withdrawal rates (95%) are higher than with 99% safety, and average lifetime incomes are higher, but still generally not as high as for the annuity. Table 2b gives the results.

Only in the joint investor case with the HWR strategy does the lifetime annual average income with the safe withdrawal strategy exceed the annuity. However, with that strategy the withdrawals increase greatly over time on average, with the final year’s (nominal dollar) withdrawal averaging $106,399 compared with an initial year withdrawal of $33,700. Because of this back-loading of income over a long time period, real average incomes for both are nearly the same, $45,585 for the HWR safe withdrawal rate and $44,214 for the annuity.

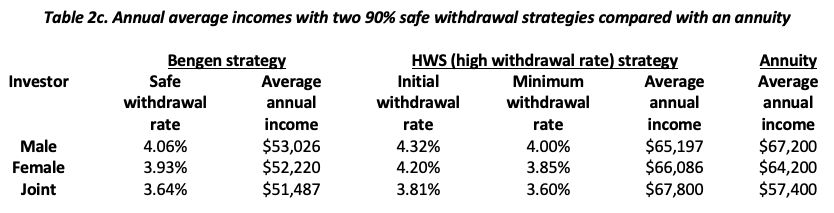

If we go even further and assume that a 10% failure rate with the safe withdrawal strategy is acceptable, the results are shown in Table 2c.

Even at this low level of certainty of safety, the Bengen safe withdrawal strategy falls well below the annuity in lifetime average annual income. Even the HWR strategy is not fully competitive with the annuity. And, remember that these are only lifetime average annual incomes averaged across all scenarios. The lifetime averages vary across scenarios, posing the risk that a particular investor’s lifetime average will be lower. The annuity income, by contrast, remains the same predictable amount for all investors – so long as the insurer does not default.

What about inflation-adjusted annuities?

By using the actuarial tables and simulated inflation sequences, I ran projections of average lifetime income with both inflation-adjusted annuities and non-inflation-adjusted annuities. The projections showed that the non-inflation-adjusted annuity produced higher average annual lifetime incomes than the inflation-adjusted annuity (whether expressed in nominal or real dollars). For example, for a male annuitant the non-inflation-adjusted annuity yielded an annual average of $7,401 more nominal dollars than the inflation-adjusted annuity. The median increment for the non-inflation-adjusted annuity over the inflation-adjusted annuity was $5,092. Still, there was some risk of the non-inflation-adjusted annuity underperforming the inflation-adjusted one in inflationary periods. There was a 5% chance that the inflation-adjusted annuity would yield more than $10,000 annual average income (in nominal dollars) than the non-inflation-adjusted one.

This is not surprising. The investor in a non-inflation-adjusted annuity bears more risk of inflation than the investor in an inflation-adjusted annuity. Therefore, that investor, as compensation for bearing more risk, should expect an accordingly higher amount of lifetime income. Nevertheless, investors who expect a future pattern of U.S. inflation not substantially different from the past pattern will likely choose the non-inflation-adjusted annuity. But investors who are particularly concerned about the possibility of hyperinflation even in the U.S. may choose the inflation-adjusted one. The decision whether to use an inflation-adjusted or inflation-unadjusted annuity may be more a matter of preference and of the investor’s projection of the pattern of future expenditures than of their average projected difference.

Conclusions

Even at no more than 90% assurance that the money won’t run out over an investor’s lifetime, and emphatically for any level of certainty above that, an annuity is preferable to a safe withdrawal strategy. The annuity’s advantage is that it leaves no money for bequests when you die, while a safe withdrawal strategy usually leaves a large amount.

This is assuming historic rates of return are adjusted downward slightly because of projections of lower future than historical returns. If one believes that future returns may be even lower – as, for example, Jeremy Grantham does – then a “safe withdrawal rate” may not be safe at all; an annuity is the clear safe haven. Thus, uncertainty about the expected returns on stocks and bonds adds to the uncertainty of the safe withdrawal strategy.

If an investor does desire to leave a legacy, this study points to the possibility that the investor should split their investment between a portion intended to provide the maximum income for the investor’s lifetime and a portion intended to provide a legacy, and invest the lifetime portion in an annuity. Moreover, the annuity payment amounts are, of course, inflexible, suggesting that to provide for fluctuating expenditures a portion of assets should be held outside the annuity – and it could be the same portion that is intended to fund a legacy.

Economist and mathematician Michael Edesess is adjunct associate professor and visiting faculty at the Hong Kong University of Science and Technology, chief investment strategist of Compendium Finance, adviser to mobile financial planning software company Plynty, and a research associate of the Edhec-Risk Institute. In 2007, he authored a book about the investment services industry titled The Big Investment Lie, published by Berrett-Koehler. His new book, The Three Simple Rules of Investing, co-authored with Kwok L. Tsui, Carol Fabbri and George Peacock, was published by Berrett-Koehler in June 2014.

1 Unless otherwise noted, I use the term “annuity” to refer exclusively to single premium immediate annuities, or SPIAs.

2 I am grateful to Allan Roth and especially to Joe Tomlinson for help in obtaining the market rate on simple annuities, and to Joe for providing me his table of mortalities based on the Society of Actuaries’ 2012 IAM table. I am also appreciative of comments by both Allan and Joe on a draft of the article.

3 For example, suppose that p is 4.5% and p0 is 3.5%. With starting assets of $1 million, the initial year’s withdrawal will be $45,000. Suppose assets increase in ten years to $2 million. The withdrawal would then be 4.5% of $2 million or $90,000. But if, instead, the value of assets had declined to $900,000 while inflation had caused the initial $1 million to be worth $1.2 million in today’s dollars, the withdrawal would be 3.5% of $1.2 million or $42,000, because it is greater than 4.5% of $900,000.

4 Another withdrawal strategy has been proposed by M. Barton Waring and Laurence B. Siegel. It begins by withdrawing at the initial annuity rate and then withdraws at the annuity rate prevailing for the investor’s age in subsequent years. However, this strategy sets no minimum withdrawal and can never completely run out of money, although withdrawals can dwindle almost to the point of vanishing. It is, therefore, difficult to compare it with the other strategies in the current context.

5 Assumptions used for the Monte Carlo simulations were that the probability-weighted (i.e. occurrence-weighted) average of the annual probability distribution of equity returns – i.e., their “expected” return – is 9.5% with a standard deviation of 18%, that the corresponding expected return on bonds is 4.5% with a standard deviation of 7%, and that the correlation coefficient between them is 0.25. These stock-bond assumptions correspond to a long-run (i.e., asymptotic) return on equities of 8% and a long-run return on bonds of 4.25%. To state it with more mathematical rigor, the probability that the annualized equity return is outside an arbitrarily small window around 8% tends toward zero as the time period lengthens (similarly, around 4.25% for bonds). This note addresses with more rigor the often noted but often confused distinction between arithmetic and geometric averages of rates of return.

6 As a check, I also generated stock-bond portfolio sequences in a different way by using the 91 historical equity (S&P 500) and bond (10-year T-bill) returns for the years 1928-2018 that can be downloaded from a web site maintained by Aswath Damodaran of the Stern School of New York University. The methodology was, for each year of a sequence, to randomly choose one of the 91 years from 1928-2018 and use the stock and bond returns that occurred in that year, adjusted downward so that their long-run returns were 8% and 4.25%, respectively. The results – perhaps surprisingly – were negligibly different from the results obtained using the Monte Carlo simulation procedure.

7 Because inflation rates are strongly serially correlated (autocorrelation coefficient for U.S. annual inflation rates from 1914 to 2018 was 0.64), and because their distribution is leptokurtic (fat-tailed), the simulation method used for stock and bond returns is not appropriate to use for generating random future inflation rates. Instead, for each sequence, a random starting year between 1914 and 2018 was chosen. Then an inflation rate sequence was generated using the historical inflation rates beginning at that starting point (downward adjusted so that the long-run annualized inflation rate was the consensus forecast of 2.3%); then when the 105-year inflation rate sequence ended, circling back to continue the simulated sequence with the first year’s, 1914’s, inflation rate. Historical correlations between annual inflation and annual equity returns were near zero and similarly, so were correlations between annual inflation and annual bond returns (though bond returns and inflation are correlated over longer time periods); therefore, it was not necessary to correlate the inflation rate sequence thus generated to the stock and bond return sequences.

8 In the latter case, because the dollar annual averages quoted here are averages of nominal dollar withdrawals, not real dollar withdrawals, the higher average annual income compared to that for a female is due to the greater number of years of withdrawals for the joint investor and thus a higher weighting of future inflated dollar withdrawals.

More Alternative Investments Topics >