Noise levels are likely to remain elevated in the run-up to – and possibly in the immediate aftermath of the upcoming US presidential election, but the post-election outlook should prove positive for EM assets by ushering in a period of more positive risk-sentiment, a long period of low US rates and a lower Dollar.

Analysis of US equity market performance around elections shows that investors have generally assigned too much credit to Republicans on the economy with stock markets running up ahead of Republican wins, but then disappointing afterwards. The opposite is generally true for Democrat wins, especially when Democrats overturn Republicans. This pattern is even more pronounced for EM equities with sharp rebounds, when Democrats overturn Republicans.

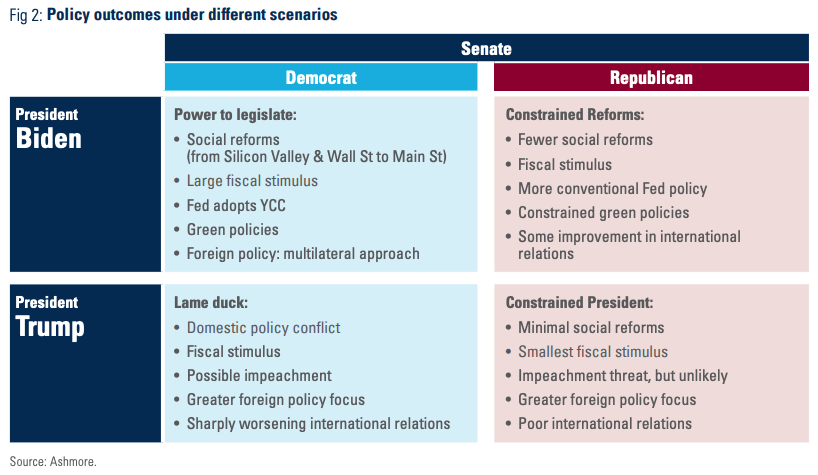

Post-election US domestic policy options – fiscal and monetary depend more on the outcome of the Senate race than the presidential election itself. If Democrats win the Presidency and control both houses of Congress they will be in position to legislate, including passing structural reforms and approving new fiscal stimulus. If Trump wins, but fails to hold the Senate he will be lame duck and political risk rises sharply, including impeachment risk. A Trump win with the Senate remaining in Republican hands is a continuity scenario.

Either way, the economy will be key in the next presidential term. The US economy is in the grip of a classic real exchange rate overvaluation, a late business cycle symptom. The prospect of yet more fiscal stimulus and monetary policies geared towards funding the fiscal deficit are a recipe for lower trend productivity growth and capital outflows. This bodes well for EM equities due to a strong relationship between EM equity outperformance relative to the S&P 500 and the broad Dollar.

Short-term sentiment drivers

In the short term, that is, up to and including the US presidential election on 3 November and the immediate aftermath of the election, markets are likely to react strongly to changes in the level of uncertainty. The clearer the outcome as implied by the polls, the greater the confidence of investors, since an unambiguous election outcome is more likely to give rise to additional fiscal stimulus.

For now, this means that improving poll numbers in favour of Democratic candidate Joe Biden is associated with positive markets. According to most polls, Biden is leading incumbent President Donald Trump by at least 10%. A lead of this size is also evident in a number of individual states with critical Senate races, thus implying a high probability that the Democrats will take the Senate. Since the Democrats already control the House of Representatives, the prospect of a so-called ‘blue sweep’ is a distinct possibility, which would increase odds of decisive and effective government.

The main risk right now is that Trump regains momentum in the polls. A surge in Trump’s poll ratings would once again plunge the election outcome into greater uncertainty, raising the spectres of a contested election, a split Congress, and, by implication a lame duck presidency without the power to effect policy change. This scenario would also imply less chance of fiscal stimulus, or at best reduce the clarity about its potential size.

Historical market performance in the run-up to and in the aftermath of US elections

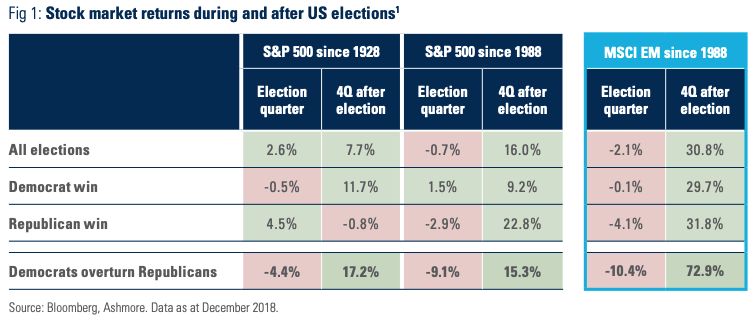

Since 1928, the US equity market has generally tended to assign too much credit to Republicans on the economy with stock markets running up during elections with Republican winners, but then expectations cannot be met and stocks tend to disappoint in the first year of Republican administrations. The market appears to pay a high price for the ‘peace of mind’ of having conservatives in charge, albeit this pattern has changed since 1988 on the elections of Reagan, Bush Sr., and Trump.

The opposite is generally true for Democrat wins as US stocks tended to perform poorly during the election quarter, but then rally very strongly in the following year. This has been the pattern in every Democrat win since 1944 with the exception of Carter’s first year in office. The pattern of poor performance in the run up to election followed by post-election outperformance was even more pronounced, when a Democrat candidate overturned a Republican incumbent.

The pattern is similar, but even more powerful in EM equities. Since 1988, EM equities tend to have negative returns during US election quarters, but delivered strong performance in the 12 months following elections. Post-election rebounds were especially pronounced in the two episodes, when Democrats overturned Republicans with EM equities delivering an average return of 72.9% in the first year of the Clinton and Obama administrations in 1993 and 2009 respectively. Figure 1 summarises these points. The table shows stock market returns in the quarter of the election and in the subsequent 12 months for all election outcomes, Democrat wins, Republican wins, and elections where Democrats overturn incumbent Republican presidents.

US domestic policy options – notably fiscal and monetary policies – after the 3rd November election are likely to depend more on the outcome of the Senate race than the presidential election itself. If Democrats win the Presidency and control both houses of Congress they will be in position to legislate, including passing structural reforms and approving new deficit spending, almost at will. Debt issuance can therefore rise sharply, which means that the Fed may be forced to adopt yield curve control in order to keep term rates under control. Markets will initially be torn between the negative feelings about a more left-leaning Democratic Party in control of both houses of Congress, but once a new Democrat administration is in place markets will likely focus on the fiscal stimulus. If Trump wins, but fails to hold the Senate he will be a lame duck President and political risks rise sharply, including impeachment risk. A Trump win with the Senate remaining in Republican hands is a continuity scenario.

Foreign policy is all about discretion versus rules-based approaches. In our opinion, a Biden presidency would likely favour a return to a more conventional multilateral approach with strong US global leadership, adherence to US-sponsored rules, and a greater role for US-sponsored global governance institutions. This ought to be good for stability, good for smaller countries. There may be more coordinated pressure against Russia, Turkey, and North Korea, while negotiations with China may take place within a more structured framework, which ought to be greater recognition to the mutual economic dependence of the two countries. Environmental policies would likely be given higher priority, which could put the US at odds with the Bolsonaro administration in Brazil, although South America’s relatively modest strategic importance suggests that relations would not break down.

By contrast, Trump would likely escalate his already heavily discretionary approach to foreign policy, especially if he becomes a lame duck at home, which would leave foreign policy as his only remaining policy domain. This bodes poorly for smaller countries, but well for authoritarian regimes. In our view, under a second Trump administration, US policies would likely foster even deeper divisions, which could force traditional allies to pick sides. The clever ones are likely to find ways to play both sides, but global trade, capital flows, and welfare would be inferior to those achievable under a Biden presidency. The table in Figure 2 summarises the four most likely scenarios and their policy implications.

The economic reality beyond the 2020 election

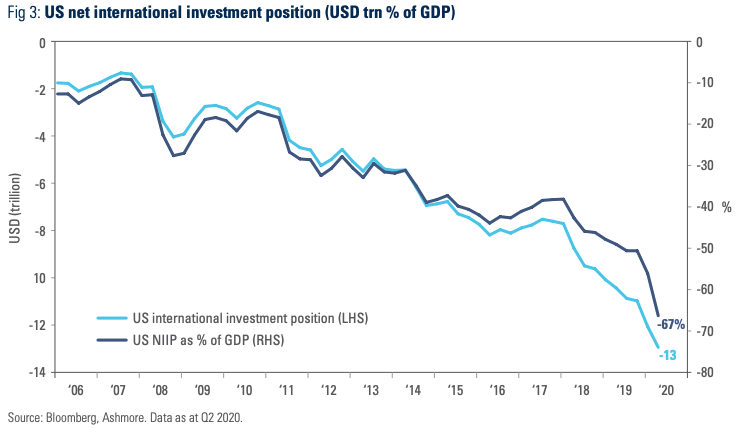

Beyond the election on 3 November, it is all about the economy. The US economy is currently staging a recovery from lockdowns, but the experience has left scars, including higher permanent levels of unemployment and a greater debt load. The sharp economic shock has thereby exacerbated macroeconomic imbalances in a notable way. The larger fiscal deficit has contributed to a wider current account deficit, while the debt burden is clearly on an unsustainable path. Wages and the Dollar remain too high relative to US productivity growth. The US economy is in the grip of a classic real exchange rate overvaluation, which is a classic late business cycle symptom. It has only been possible to sustain these imbalances due to inflows to the US from overseas. However, the US already owes USD 13tn to the rest of the world, or about 67% of GDP (Figure 3). The prospect of yet more fiscal stimulus and monetary policy easing increasingly geared towards funding the deficit is a recipe for capital outflows.

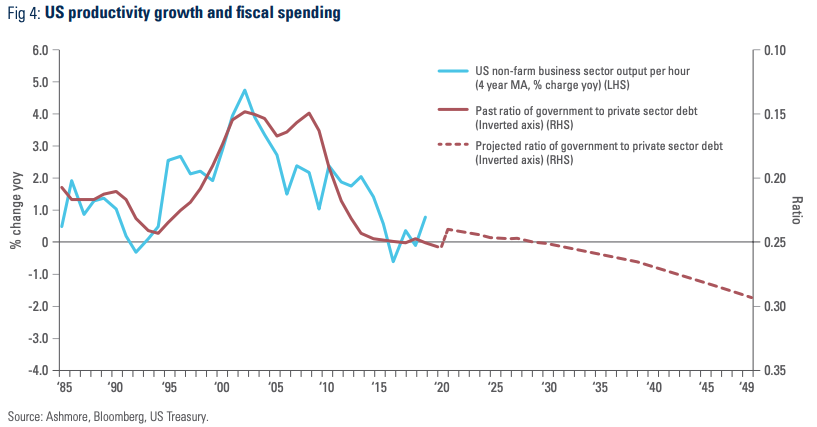

The Federal Reserve (‘Fed’) is stating publicly that the US economy needs more fiscal stimulus.2 Yet, the Fed also regularly argues that the debt stock is unsustainably large.3 Monetary policy has been reduced to asset purchases. Hence, there are no easy solutions. The US is in need of deep structural reform. Reform looks unlikely, however. There is a far higher probability, in our view, that the next US administration embarks on yet more fiscal stimulus, producing a deluge of new debt. Unfortunately, rising government debt is strongly associated with lower productivity growth as shown in Figure 4.4

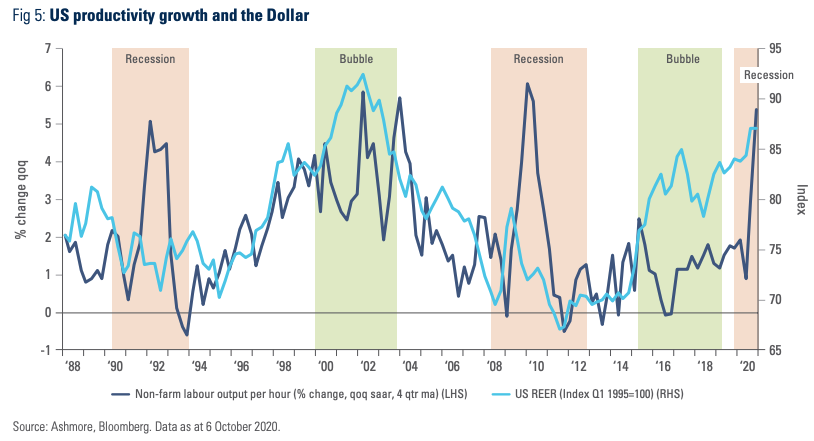

Lower trend productivity has implications for currencies. Lower US productivity growth is strongly associated with a lower Dollar except for temporary aberrations around extreme turnings points in the business cycle, such as recessions and asset bubbles. At these turning points – and the US economy may well be in the grip of one right now – productivity growth and the Dollar may temporarily de-couple as shown in Figure 5. Specifically, productivity growth tends to spike in recessions, but without a sustained rise in the Dollar. In fact, the Dollar typically falls in the course of recessions as there are better investment opportunities elsewhere. Hence, the odds are now rising that capital will flow from US markets towards the rest of the world, including EM.

Ironically, any attempts to correct the unsustainable US fiscal deficit through higher taxation of large corporations and high net worth individuals may end up weakening the Dollar as well. Most corporate cash is highly mobile and will seek out jurisdictions with less onerous taxes. If this happens, not only the Dollar but also US assets more generally would be negatively impacted.

The impact of flows to EM

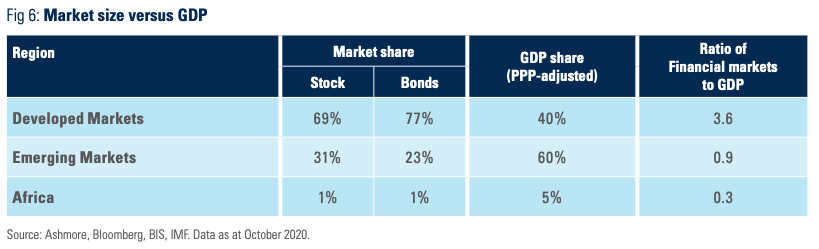

The significance of the Dollar to EM becomes particularly clear when one considers the severity of finance constraints in EM economies. As Figure 6 shows, EM economies have less finance than their GDP (ratio of 0.9x) compared to 3.6x more finance than GDP in developed economies. Inflows to EM would therefore be strongly positive for investment and domestic demand-led growth as credit becomes more widely available. Stronger growth is associated with better fiscal outcomes, higher corporate earnings, and lower default rates for corporates and sovereigns alike, thus strengthening the investment case for EM assets in general.

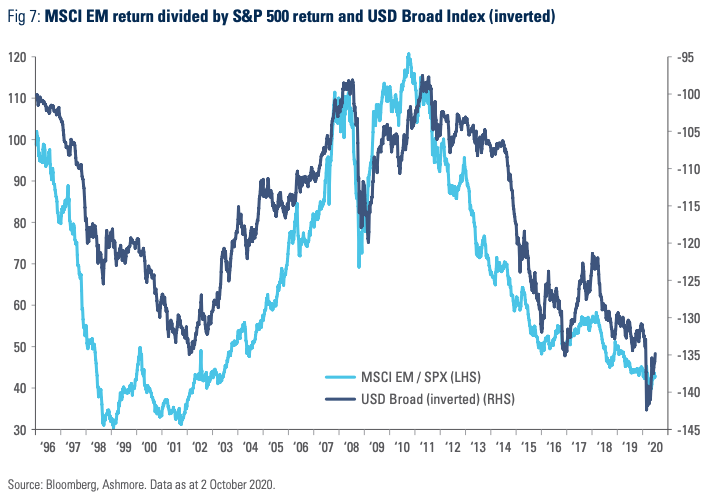

As domestic demand picks up in response to inflows, inflation pressures can be expected to gradually rise. Real bond yields in EM are still high enough that bonds offer value in an environment of modestly rising prices, but over the medium term a lower Dollar environment strongly favours EM equities. This is evident from Figure 7, which shows the close relationship between EM equity performance relative to the S&P 500 and the broad Dollar.

1 This analysis likely overstates the importance of the choice of president for stock market performance. In democracies, the scope for presidential action is constrained by the balance of power in Congress, which is not taken into account. Moreover, the economic cycle has an effect on stock market performance independent of both the choice of president and the balance of power in Congress.

2 See https://www.marketwatch.com/story/powell-says-u-s-economy-needs-more-fiscal-support-11601995205

4 The link between productivity and US government debt arises, because US government spending is far less productive than US private sector spending. Greater debt-funded government spending usurps capital for unproductive spending, which could otherwise have been invested more productively in the private sector, thus reducing productivity in the economy as a whole on average.

No part of this article may be reproduced in any form, or referred to in any other publication, without the written permission of Ashmore Investment Management Limited © 2020.

Important information: This document is issued by Ashmore Investment Management Limited (‘Ashmore’) which is authorised and regulated by the UK Financial Conduct Authority and which is also, registered under the U.S. Investment Advisors Act. The information and any opinions contained in this document have been compiled in good faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. Save to the extent (if any) that exclusion of liability is prohibited by any applicable law or regulation, Ashmore and its respective officers, employees, representatives and agents expressly advise that they shall not be liable in any respect whatsoever for any loss or damage, whether direct, indirect, consequential or otherwise however arising (whether in negligence or otherwise) out of or in connection with the contents of or any omissions from this document. This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any Fund referred to in this document. The value of any investment in any such Fund may fall as well as rise and investors may not get back the amount originally invested. Past performance is not a reliable indicator of future results. All prospective investors must obtain a copy of the final Scheme Particulars or (if applicable) other offering document relating to the relevant Fund prior to making any decision to invest in any such Fund. This document does not constitute and may not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment in any such Fund. Funds are distributed in the United States by Ashmore Investment Management (US) Corporation, a registered broker-dealer and member of FINRA and SIPC.