Hear David Blanchett speak at the AP Thought Leader Summit on retirement income. Register now!

Hear David Blanchett speak at the AP Thought Leader Summit on retirement income. Register now!

Low yields have important implications for retirement strategies. One example is the decision of when to purchase an annuity.1 Despite the fact that interest in guaranteed income has risen, demand has declined significantly since the onset of the pandemic.

Single-premium immediate annuities (SPIAs) have interest rate exposures similar to a long-duration bond, and a rise in interest rates can increase payouts. Therefore, retirees who are interested in additional guaranteed income2 might delay the SPIA purchase in the hopes interest rates and payouts rise.

This article explores the trade-offs associated with the decision to delay an annuity purchase – in particular the interaction between changes in bond yields and assumed portfolio rates of return, and the impact of mortality improvement.

After crunching some numbers, I find that the “cost” associated with delaying an annuity purchase varies. For super-conservative investors (e.g., those who would invest entirely in government bonds) and older annuitants (age 75-plus) delaying the annuity purchase doesn’t make much sense, even if rates do end up rising; it’s better to go ahead and buy the annuity now. However, to the extent the investor expects to realize a higher return (e.g., by investing in risky assets) or bond yields to rise, or if the investor is younger (under the age of 65), delaying the annuity purchase is the smart move.

It’s impossible to know where the markets are headed, though, so the best strategy for retirees to increase guaranteed income is “dollar-cost averaging,” where annuities are purchased over time. This reduces the regret associated with future changes in rates and ensures the household has a plan to generate consistent lifetime income.

Annuity payout rates

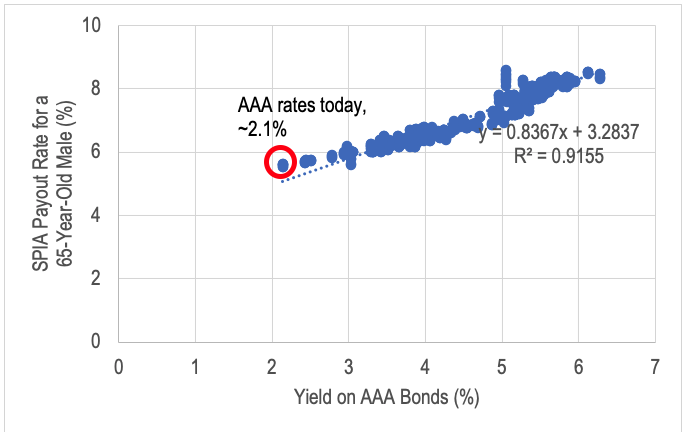

Annuity payout rates move relatively in-sync with bond yields. The chart below shows the historical relation between the average SPIA payout for a life-only annuity for a 65-year-old male3 and prevailing AAA yields4.

65-year-old male life-only SPIA payout rates and AAA bond yields: September 2004-August 2020

There is a notably high correlation between AAA yields and annuity payouts, with an R² of 91.55%. Annuities offer more attractive payouts when insurers expect to earn a higher return from investing premiums. Given today’s low bond yields, insurers can’t expect to earn as much through investing and therefore have to decrease payout rates to reflect lower expected returns.

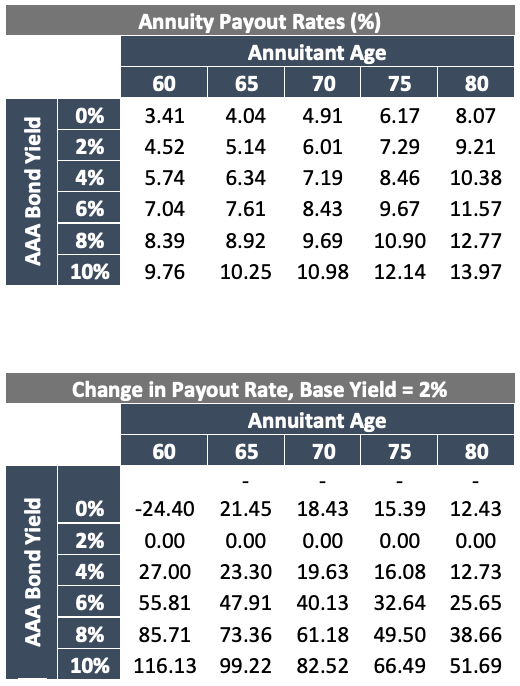

The first table below shows the expected payout rate for a SPIA assuming different purchase (start) ages and bond yields, as well as how the payout rates change assuming the base yield of 2% (which is where AAA yields are approximately today). The payout rates are determined using the Society of Actuaries 2012 immediate-annuity mortality table with improvement to 2020, assuming a 10% mortality reduction and an expense load of 5%.

Assuming a base yield of 2%, the second table shows how the payouts change. For example, focusing on a 65-year old, if interest rates rise to 4%, they would increase from 5.14% to 6.34%, which is an increase of 23.3%.

Younger annuitants are impacted more by lower interest rates. This is because the duration of the payments is greater. In other words, the expected payout period for a 60-year-old is longer than that of an 80-year-old, so the compounding effect of the yields is going to influence payouts more. Younger annuitants benefit from waiting should interest rates rise. At the same time, though, younger annuitants are more affected when rates fall. If interest rates keep falling, the payouts available today may be unavailable.

The benefits associated with mortality credits are also lower for younger annuitants. For readers not familiar with mortality credits, it’s based on the idea that some people who purchase an annuity will die relatively young, and others will live a long time, but by pooling the money together at the insurer the payout an annuitant can receive is collectively higher than it would be for each person planning for their own retirement.

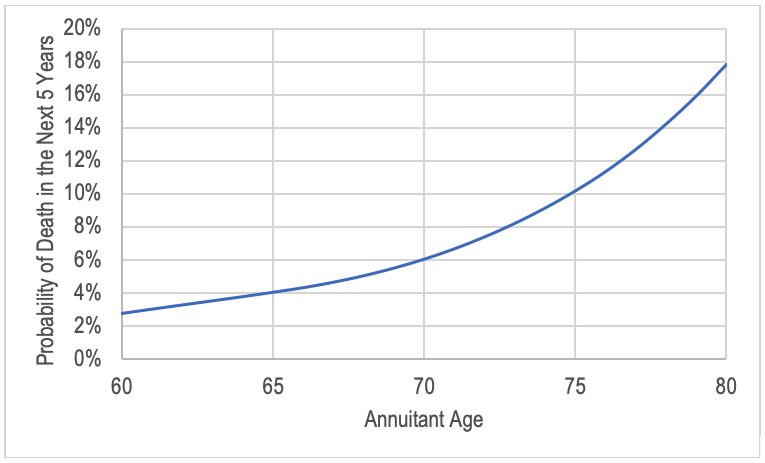

The higher the probability of death, the greater the benefits of mortality credits (i.e., mortality pooling). Younger people are less likely to pass away compared to older individuals. The chart below provides some perspective on how mortality rates vary by age and includes the probability of death within five years using the same mortality assumptions used to estimate the annuity payouts.

The probability of a 60-year-old dying within five years (by age 65) is 2.7% versus 17.8% for an 80-year-old. Again, this suggests the costs of waiting for yields to rise is lower for someone who is younger.

One of the costs associated with waiting to purchase an annuity, though, is improvement in mortality. Mortality rates have decreased over time (i.e., people are living longer) and which means $1 of income is going to cost more in the future, even if bond yields stay the same.

For example, assuming AAA bond yields stay constant at 2%, the cost of an annuity (i.e., what it takes to buy $1 worth of income) is going to increase by about 2% in five years based on the improvement rates in the Society of Actuaries 2012 immediate-annuity mortality table. In other words, even if interest rates stay the same, a 65-year-old today can be expected to get a 2% higher payout than a 65-year-old in five years.

Analysis

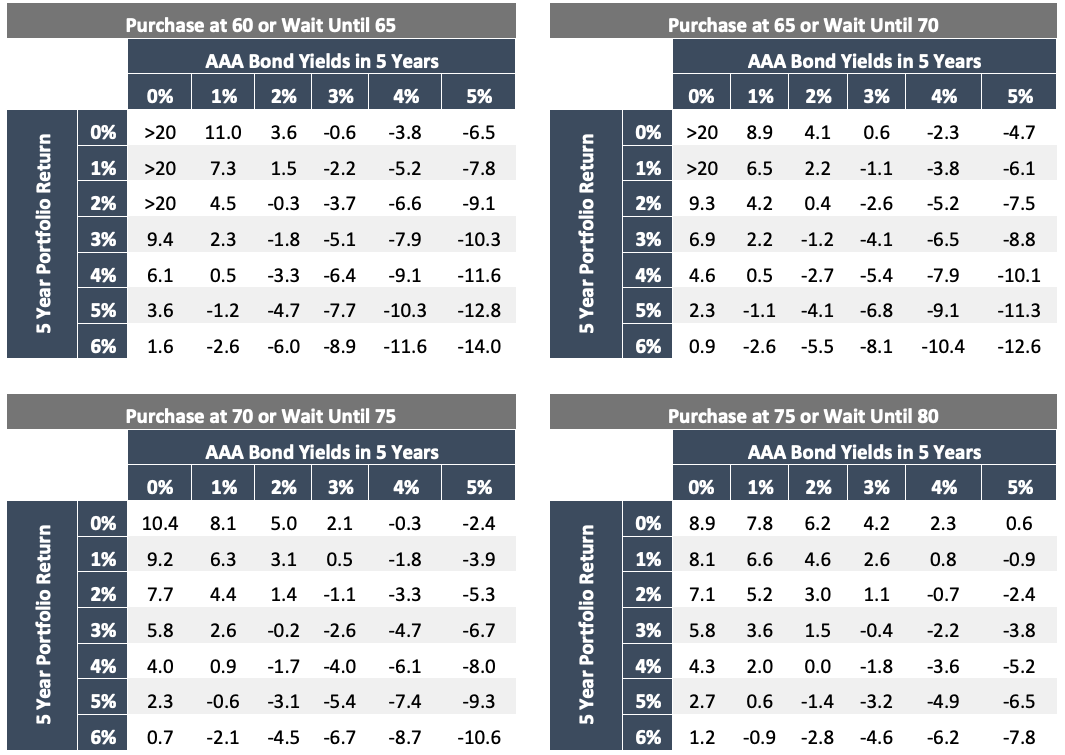

Analyzing potential changes in bond yields, assumed portfolio returns and the impact of mortality improvement is complex. Therefore, to better understand when it makes sense, I conducted an analysis.

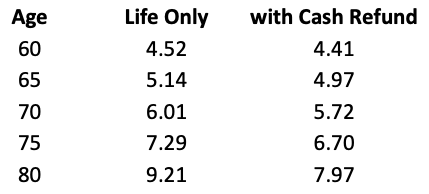

I assume a male either purchases an annuity today (in the year 2020) or waits five years (in the year 2025). Since it’s possible the individual could pass away during the initial five-year period, opposed to using the life-only payout rates estimated previously, I attached a five-year cash refund provision when pricing the annuity to ensure the individual would get at least the entire premium back should he pass away during the five-year period. I solved for the payout rate for the annuity with the five-year cash refund provision assuming the same load as the more traditional life-only annuity (5%).

Information about how the SPIA payout rates change when including the cash refund feature (again, just for the first five years) is included below. These payout rates are based on a 2% AAA bond yield, which is roughly consistent with rates today, so the analysis would be especially relevant for someone interested in delaying now.

The analysis estimates the “benefit” associated with buying the annuity now given an assumed prevailing AAA-bond yield versus purchasing the SPIA in five years (i.e., in the year 2025), given the assumed (annualized) rate of return investing in the premium dollars over the five-year period. In theory these two should be related, given the negative relation between changes in bond yields and returns; however, these values are assumed to be independent.

The “benefit” associated with buying the annuity now is shown as the internal rate of return of the mortality-weighted cash flows for the respective scenario. In other words, this is the “return” associated with buying the annuity now. A positive number means the individual is better off annuitizing now and a negative number means the individual is worse off. Four potential delay scenarios are considered (60>65, 65>70, 70>75, and 75>80), which spans the payout ages previously covered.

The results are of the analysis are included in the tables below:

As the five-year portfolio return increases and the future AAA bond yield increases, the benefit to delaying increases. Additionally, older individuals are better off not delaying (this is due to the higher relative impact of mortality credits for older ages versus younger ages).

Since annuity payouts are guaranteed (baring insurer default), the most relevant proxy (for investment purposes) is government bonds. Yields on five-year government bonds are approximately 0.25%. If we assume the expenses related to owning the securities reduces the expected return to 0%, AAA yields would have to rise to about 3% for it to make sense delaying from age 60 to age 65, but to approximately 6% to make sense delaying from age 75 to 80. If the individual is able to realize a higher return, say closer to 2%, the AAA yield wouldn’t have to move nearly as much.

It is possible rates could go lower (e.g., if AAA rates went to 1%). If this were to happen, the required return on the portfolio would have to be 5% or higher in the scenarios above to make the delay decision worthwhile.

Conclusions

The best opportunity for guaranteed income is delaying claiming Social Security retirement benefits. Social Security retirement benefits aren’t tied to prevailing interest rates, so the payouts become increasingly attractive versus SPIAs as interest rates fall. Assuming delaying Social Security isn’t sufficient and you have a client looking for guaranteed income, buying an annuity is worth considering.

Low bond yields have reduced payouts for annuities, but the lower income that can be achieved from an annuity reflects the lower return expectations from investing in fixed income. This analysis explored the impact from delaying the annuity purchase in the hope bond yields rise (which will increase payouts) or if the retiree believes they will be able to earn a higher return in the meantime.

Assuming someone is going to invest in government bonds, delaying the annuity purchase doesn’t make much sense. However, to the extent an individual is able to earn a higher return or that bond yields rise, it makes sense delaying the purchase. The older someone is, though, the more it makes sense to annuitize to start realizing the benefits of mortality credits.

Given the uncertainty associated with markets and the potential regret of timing the purchase decision incorrectly, a sensible strategy is to dollar cost average into an annuity strategy. The retiree won’t get the most income, nor will they get the least. It also creates a strategy to convert savings into guaranteed income.

David M. Blanchett, Ph.D., CFA, CFP®, is head of retirement research for Morningstar's Investment Management group.

1 For this piece I’m not going to focus on whether someone should annuitize, rather explore what factors relate to the timing decision.

2 In particular for whom delaying Social Security retirement benefits is not an option. Social Security retirement benefits are the best thing around when it comes to guaranteed income, especially today given the low bond yield environment.

3 Data is from CANNEX and reflects the average quote for all insurers providing quotes for the period

4 Source: https://fred.stlouisfed.org/series/AAA

Read more articles by David Blanchett

Hear David Blanchett speak at the AP Thought Leader Summit on retirement income. Register now!

Hear David Blanchett speak at the AP Thought Leader Summit on retirement income. Register now!