Do Bonds Still Provide Diversification?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe bond market has been quiet for the past six months, with Treasury yields holding in narrow ranges near historic lows. Given these low yields, there is a lively debate going on about whether bonds can continue to provide diversification in a portfolio. Many fear that if markets become volatile and stocks decline again, bond yields don’t have much room to fall—and therefore, won’t provide the balance to a portfolio that they have in the past. This view is often wrapped up with the idea that the traditional balanced portfolio of 60% stocks and 40% bonds is “dead.” These fears were stoked by the turmoil in the markets in March, when bonds and stocks sold off at the same time for a few days, before the Federal Reserve stepped in to calm the markets.

In our view, those fears appear overblown. The 60/40 portfolio was never right for everyone. The right mix of assets depends on an individual’s capacity and tolerance for risk and specific goals. The 60/40 portfolio was more of a starting point. Moreover, correlations between asset classes diverge from time to time, so it’s a myth that they are stable in the first place. Investors should expect some variations in the short run. More importantly, we still expect low-risk or risk-free bonds, like Treasuries, to provide diversification from stocks during times of market downturns, even though a 60/40 portfolio may not be the best choice for most investors.

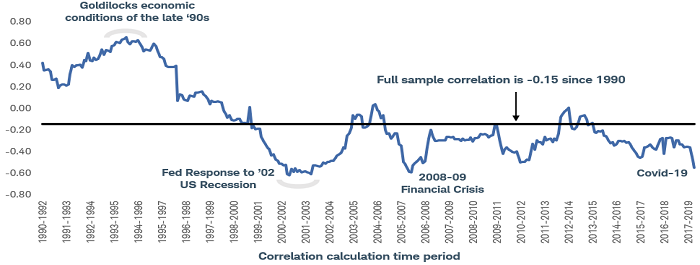

The correlation between stocks and Treasuries varies over time

Rolling 3-year correlation between U.S. stocks and U.S. Treasuries has varied from -0.6 to +0.6

Source: Charles Schwab Investment Advisory, Inc. Historical data from Morningstar Direct, as of 3/31/2020. Indexes representing the investment types are: U.S. stocks = S&P 500 Total Return Index (1990 onward); U.S. Treasuries = Bloomberg Barclays 3-7 Year Treasury Index (1992 onward) and FTSE U.S. Treasury Benchmark 5-year USD (1990-1991). Past performance is no indication of future results.

Separating diversification from expected returns

Despite concerns, Treasuries have demonstrated an even higher level of inverse correlation with stocks over the past six months compared with the past five years. There was a brief period of about a week in March when Treasuries and stocks were positively correlated, but that ended quickly. If your investing time horizon extends beyond a few days or weeks, we would not consider short-term dislocations to be significant. As the chart below illustrates, the correlation between Treasuries and the S&P 500® index over the past six months was similar to the correlation over the past five years. Treasuries—especially long-term Treasuries—have moved in the opposite direction of stocks.

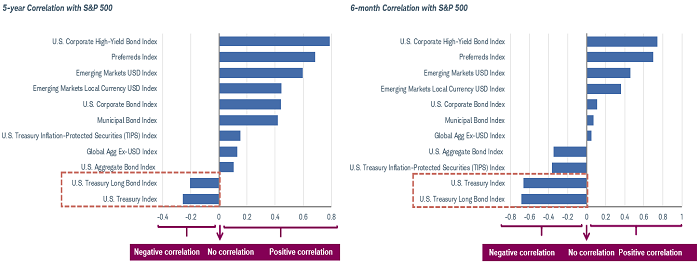

Fixed income asset class correlation with the S&P 500

Note: Correlation is a statistical measure of how two investments historically have moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated. Correlations shown represent an equal-weighted average of the correlations of each asset class with the S&P 500 during the 5-year period between June 2015 and June 2020.

Source: Bloomberg, as of June 2020. Indexes representing the investment types are: U.S. Corporate High Yield Bond Index = Bloomberg Barclays U.S. Corporate High-Yield Bond Index; Preferreds Index = ICE BofA Merrill Lynch Preferred Stock Fixed Rate Index; Emerging Markets USD Index = Bloomberg Barclays Emerging Market USD Index; Emerging Markets Local Currency USD Index = Bloomberg Barclays EM Local Currency USD Index; U.S. Corporate Bond Index = Bloomberg Barclays U.S. Corporate Bond Index; Municipal Bond Index = Bloomberg Barclays Municipal Bond Index; U.S. Treasury Inflation-Protected Securities (TIPS) Index = Bloomberg Barclays U.S. Treasury Inflation-Protected Securities Index; Global Agg Ex-USD Index = Bloomberg Barclays Global Agg Ex-USD; U.S. Aggregate Bond Index = Bloomberg Barclays U.S. Aggregate Bond Index; U.S. Treasury Long Bond Index = Bloomberg Barclays U.S. Treasury Long Bond Index; U.S. Treasury Index = Bloomberg Barclays U.S. Treasury Index. Diversification strategies do not ensure a profit and do not protect against losses in declining markets. Past performance is no guarantee of future results.

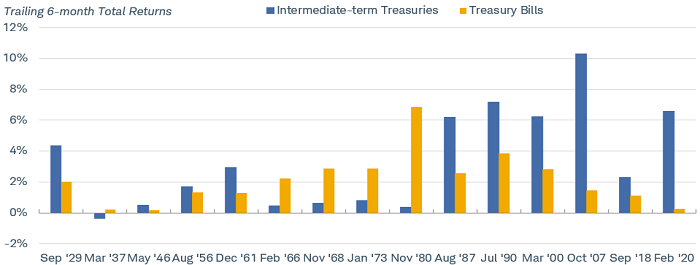

Moreover, we are hard pressed to find an example in history when the stock market has had a significant drop and returns for bonds over the subsequent six months were not positive. Even at very low yields, bonds generally have held their value or appreciated during significant stock market declines.

Intermediate bonds have tended to outperform T-bills during equity bear markets

Source: Schwab Center for Financial Research with data from Morningstar Inc. Indexes used are the Ibbotson Intermediate-Term Government Bond Index and the Ibbotson US 30 Day Treasury Bill Index. Total returns reflect the trailing 6-month total return, beginning with the month shown on the horizontal axis. Dates on the horizontal axis represent the starting months for commonly accepted equity bear markets, with the exception of September 2018. Equity bear markets are defined as periods where the S&P 500 declined peak to trough at least 20%, while the decline that began September 2018 decline was only 19%. Total returns include price change and interest or dividend income. Past performance is no guarantee of future results.

Finally, since the U.S. Treasury market is still considered a safe haven during times of market stress, there is no clear alternative to fill that role. No other government bond market has the depth or liquidity of the U.S. Treasury market. Nor is it necessarily true that bond yields can’t continue to fall. Even with the Fed trying to hold short-term yields above zero, bond yields could fall into negative territory, as Europe and Japan have demonstrated. We don’t expect that to happen, but it’s theoretically possible under adverse economic conditions.

Expected returns are low

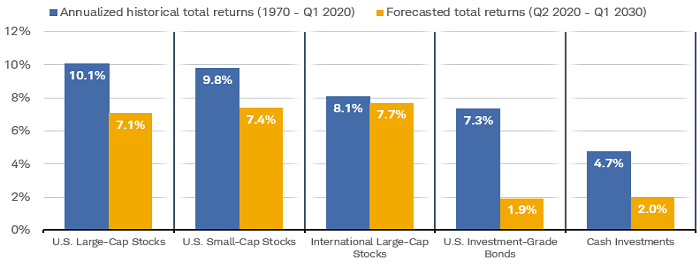

Looking beyond the diversification issue, however, we have to acknowledge that with yields so low, the high returns seen year to date in the bond market aren’t likely to be repeated over the next few years, especially if the economy continues to recover. In fixed income investments, the starting yield is a reliable indicator of future returns over the long run.

Returns for all asset classes are expected to be lower over the next decade

Source: Charles Schwab Investment Advisory, Inc. Historical data from Morningstar Direct, as of 3/31/2020. Indexes representing the investment types are: U.S. Large Cap Stocks = S&P 500 index; U.S. Small-Cap Stocks = Russell 2000 Index; International Large-Cap Stocks = MSCI EAFE Index; U.S. Investment-Grade Bonds = Bloomberg Barclays U.S. Aggregate Bond Index; Cash Investments = Bloomberg Barclays Short Treasury 1-3 Month Index. Past performance is no indication of future results.

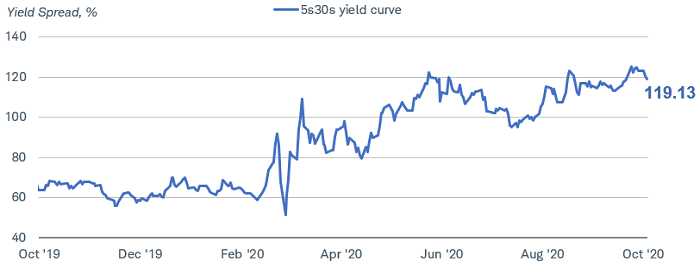

Over the next year, our expectation is that the economy will continue to improve, albeit at a somewhat slower pace than over the past few months, and that inflation will gradually move higher. Another round of fiscal stimulus would provide an extra boost to growth in the short run and likely push inflation expectations higher. In that scenario, bond prices would fall as intermediate to long-term yields would move higher, and the yield curve would continue to steepen.

Yield curve continues to steepen as the economy improves

Source: Bloomberg. Market Matrix U.S. Sell 5 Year & Buy 30 Year Bond Yield Spread (USYC5Y30 Index). Daily data as of 10/12/2020.

We see the potential for 10-year Treasury yields to rise to the 1% level over the next six months, even as the Fed keeps short-term interest rates near zero. Consequently, we continue to suggest reducing the overall duration in a portfolio to mitigate the risk of rising long-term bond yields, but maintaining an allocation to intermediate-term bonds for diversification benefits. (Duration is a measure of the sensitivity of bond prices to changes in interest rates.) Investors could consider using a barbell approach, with some short and long-term bonds. The short-term bonds provide stability and the flexibility to reinvest if rates rise, while the long-term bonds provide a way to offset the risk of another round of market turmoil. Alternatively, investors could use a bond ladder, which allows for reinvesting in longer-term bonds when interest rates move up.

Going beyond 60/40

If the traditional 60/40 stocks-to-bonds allocation isn’t optimal, what’s an investor to do? We suggest broader diversification across asset classes. Our expected returns for both stocks and bonds are lower for the next 10 years than over the past 50 years, due to high starting valuations. We suggest exposure to a wide array of global asset classes to help manage risk and provide a broader set of investment opportunities.

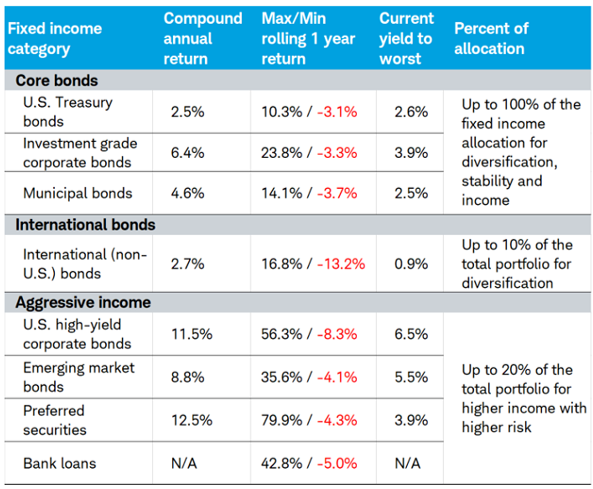

Within the fixed income market, we still favor allocating the bulk of the portfolio to “core bonds,” such as Treasuries and highly rated corporate and municipal bonds, for stability and capital preservation—but also including exposure to riskier asset investments like high-yield corporates, preferred securities, or emerging market bonds, if you have the capacity and tolerance for higher volatility. And while we don’t expect inflation to be a significant problem over the next few years, we believe holding some inflation-linked bonds, such as Treasury Inflation-Protected Securities (TIPS), makes sense, to mitigate the risk of a surprising increase in inflation.

Allocation with the three fixed income categories

Source: Schwab Center for Financial Research, Barclays, Bloomberg. For illustrative purposes only. Average annual return refers to the average total return for each sector, based on index returns from 2/2009 to 2/2019. Max/min rolling 12-month return refers to the maximum (highest) and minimum (lowest) annual return, using index returns during the period. Yield to worst means the current average yield for the representative index assuming bonds are called at their earliest call date, also known as yield to “worst.” This example does not reflect the effect of taxes or fees. Past performance does not guarantee future results.

Indexes representing the investment types are: ; U.S. Treasury bonds = Bloomberg Barclays U.S. Treasury Index; Investment grade Corporate Bonds = Bloomberg Barclays U.S. Corporate Bond Index; Municipal bonds = Bloomberg Barclays Municipal Bond Index; International = Bloomberg Barclays Global Agg Ex-USD; U.S. High-yield bonds = Bloomberg Barclays U.S. Corporate High-Yield Bond Index; Emerging Market bonds = Bloomberg Barclays Emerging Market USD Index; Preferred securities = ICE BofA Merrill Lynch Preferred Stock Fixed Rate Index; Bank loans = Bank loans = S&P/LSTA US Leveraged Loan 100 Index. Diversification strategies do not ensure a profit and do not protect against losses in declining markets. Past performance is no guarantee of future results.

The death of diversification with bonds has been greatly exaggerated

We don’t believe the diversification benefits of holding bonds has changed significantly. In fact, we believe bonds still play an important role as a diversifier from stocks.

However, with bond yields so low, finding the right balance between risk and reward is more challenging. We suggest fixed income investors consider reducing their exposure to long-term bonds to mitigate the risk of rising rates, and focusing on a broader array of bonds for diversification. A mix of domestic and international bonds, inflation-linked bonds like TIPS, along with limited exposure to higher-risk investments—like high-yield and emerging-market bonds, and preferred securities—can be balanced to provide more current income and diversification.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Investing involves risk including loss of principal. Small cap stocks are subject to greater volatility than those in other asset categories.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the U.S. government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the U.S. government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

Preferred securities are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features may affect yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so they are subject to increased loss of principal during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

A bond ladder, depending on the types and amount of securities within the ladder, may not ensure adequate diversification of your investment portfolio. This potential lack of diversification may result in heightened volatility of the value of your portfolio. You must perform your own evaluation of whether a bond ladder and the securities held within it are consistent with your investment objective, risk tolerance and financial circumstances.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All