I don’t think that data means what you think it means. Indeed, much of the data in the way we use it is simply broken.

The opportunity cost for inflation protection is high—is it worth the cost?

Read the latest model portfolio market insights to see where BlackRock’s Multi-Asset Income team see potential risks and opportunities across the landscape.

What’s a “zombie company”? You may have heard the term in the financial media recently and wondered if it’s something you should be worried about.

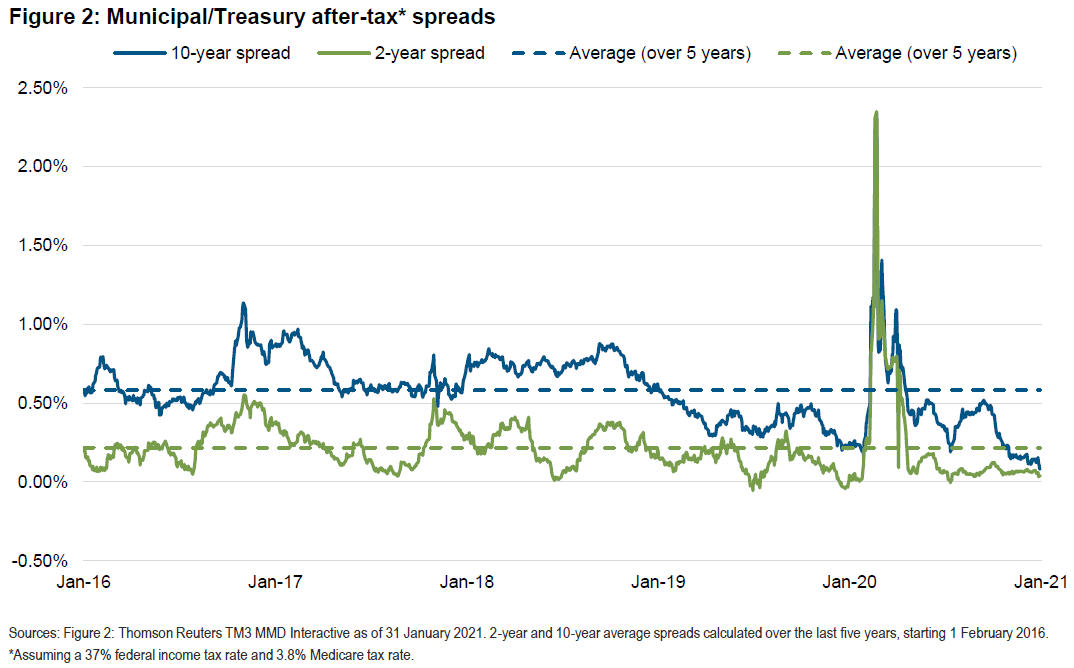

im Grabovac looks at the recent muni market selloff and why he thinks it was a valuation correction rather than a market response to actual selling.

As inflation expectations have risen, the market seems to be concerned that stronger economic growth might force the Fed to act sooner than anticipated, prompting a market selloff – particularly in growth stocks. As rates rise, valuations and earnings growth expectations decline, driving investors to seek cyclical stocks with more attractive pricing. With the 10 year now about even with the dividend yield of the S&P 500, fixed income investors might also be reallocating to bonds.

It would appear that nothing can pop the stock market bubble, but there is one straightforward “pin” that will do the job – rising interest rates.

The main fund from Cathie Wood’s Ark Investment Management slipped in pre-market trading on Thursday, as it struggles to stabilize following a 20% drop from its February peak.

Gold hasn’t been getting much love from investors lately due to rising bond yields, and bullion-backed gold mutual funds and ETFs have seen significant outflows so far this year through the end of February.

Long-term interest rates have continued to rise. While part of the increase has been fed by inflation fears, those concerns are overdone.

Our Fixed Income CIO Sonal Desai has been ahead of the curve in flagging the risks of inflation and rising rates that have now entered the mainstream debate.

We compare the current value of bonds versus stocks within the context of the equity risk premium. We couple this analysis with an evaluation of possible Fed policy direction. Our conclusion is that risk assets, such as US equities and corporate bonds, are poised to benefit as are gold and other commodities due to tumbling real yields and dollar weakening.

Investors’ reach for yield puts downward pressure on 10-year Treasury rates, likely rendering the current yield unsustainable.

Bond traders have been saying for years that liquidity is there in the world’s biggest bond market, except when you really need it.

Thomas Costerg doesn’t usually go to bed with a computer, but he couldn’t help himself Thursday night after what had just happened in the Treasury market.

Though rising yields may be indicative of an economic recovery, market volatility and inflationary fear could produce future hurdles.

Accelerating growth is generally a good thing for stocks, evidenced by bond yields and stock prices typically rising and falling together.

The late-February spike in U.S. Treasury bond yields sent ripples throughout the global markets. As yields surged to the highest level in a year, stocks and commodities sold off sharply, while the dollar rallied.

There is hope that economies will see a more sustainable and robust recovery this year, given unprecedented levels of monetary and fiscal stimulus and as more individuals are vaccinated against COVID-19. But one question for investors is what happens next—will inflation and higher interest rates be a consequence?

In the near term, markets should not be too worried about a possible spike in demand driving up inflation and interest rates, causing asset prices to fall across the board. But longer-term inflation risks are skewed much more to the upside than many investors and policymakers seem to realize.

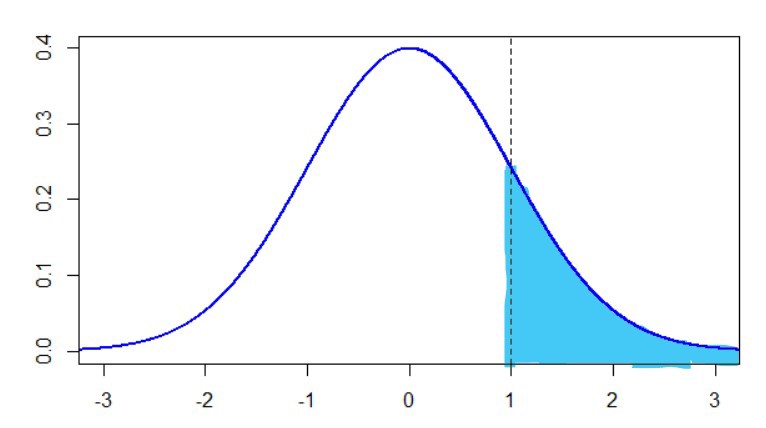

Much statistical analysis in finance depends on the assumption that variables have normal distributions. This assumption is far from correct. As a result, as Nassim Nicholas Taleb has rightly pointed out, most statistical results in finance are wrong. Now, a disciple of Taleb has tried to extend Taleb’s research by relating it to an obscure mathematical concept.

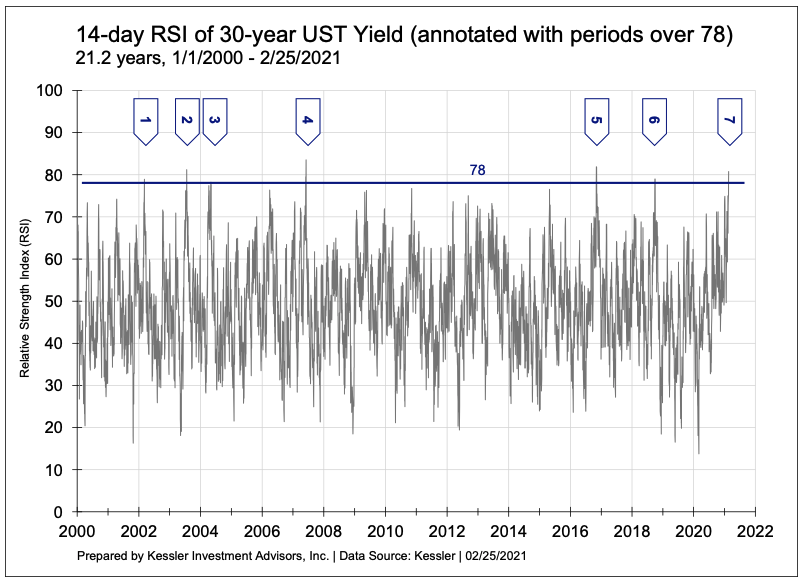

A technical indicator with a reliable history is signaling that 30-year Treasury yields will soon decline.

Yields have jumped so much, in fact, that they’re giving stocks a serious run for their money. The 10-year yield is now higher than the S&P 500 dividend yield, which may have added to the selling pressure that cost stocks close to 2.5% yesterday.

What normalcy will it be? I don’t expect to simply go back to the way things were. The economy as it was structured in December 2019 is gone forever. The world is different now. The economy will be different, too.

Despite the recent weakness in equities, Raymond James CIO Larry Adam expects positive stock growth over the next 12 months.

The Queen’s Gambit miniseries helped propel Netflix to a winning earnings report last quarter, but in fact the chess strategy it is named after has helped propel chess players to winning games for decades.

Italy’s new prime minister, Mario Draghi, has a well-earned reputation for turning around difficult situations. But can he reverse Italy’s relative economic decline? And what does his program mean for Italian bond yields?

The rout in popular technology shares accelerated after the 10-year Treasury rate spiked as much as 23 points, fueling worry that the Federal Reserve will be forced to raise interest rates.

Today’s low bond yields and high equity valuations have led many to jettison the traditional 4% initial safe-withdrawal rate assumption. But I will show that the optimal “safe” withdrawal rate depends considerably on the retiree.

Rather than worrying about the prospects of higher long-term expected inflation, the US Federal Reserve is exuding confidence that it can maintain price stability should the need ever arise. It should think again, before the inflation genie has escaped from the bottle.

More than 90% of investors believe the economy will be more robust in 2021, with a consensus it’s a V-shape recovery. For the first time since January 2020, chief investment officers want to increase capital spending rather than improve balance sheets.

Target date funds should be designed to reduce the risk of rash selling.

The unprecedented $9 trillion rescue mission by central banks to haul the world economy from its coronavirus recession is being tested as rising bond yields and inflation bets threaten their ability to keep borrowing costs down.

Casualties are piling up across the stock market as bond yields rise.

The biggest slide in months for Cathie Wood’s funds is testing the resolve of investors who plowed billions of dollars into one of the hottest firms on Wall Street.

The GMO Asset Allocation Team has released its latest 7-Year Asset Class Forecasts through January 2021.

The obstacles to higher yields in the world’s biggest debt market are slowly melting away.

The details of the January Producer Price Index showed a further surge in prices of raw materials. Breakeven inflation rates (the yield spread between inflation-adjusted Treasuries and fixed-rate Treasuries) have continued to move higher.

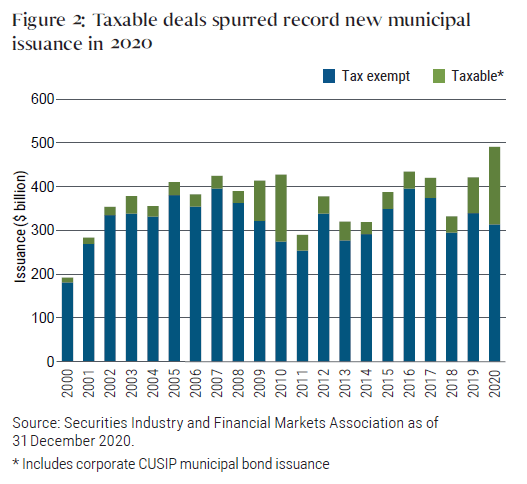

Political change, continued fiscal support will drive municipal markets in 2021, although outcomes are likely to vary.

As COVID-19 vaccines roll out and resrictions lift, a US economic rebound could lead to tighter Federal Reserve policy and higher yields. Municipal bond investors may worry about how rising yields could hurt their portfolios.

What a week for price data! We have been writing about the possibility of higher inflation for months now, most recently here. We have also highlighted the most likely assets to benefit from higher inflation like copper, oil and energy stocks.

Investment managers produce annual equity return forecasts, and the consensus is much more pessimistic than that of academics. I’ll take a closer look at why the forecasts are so different and the implications for advisors working with clients.

Many investors think there are only two options in a market where participants have become overly exuberant, either 'I want in' or 'Get me out.' Our strategies are more nuanced, and we believe fit better with what we expect to transpire.

Rather than going deep into one theme, this week we will do a “Random Thoughts” from the Frontline. Today we will cover several topics in shorter form: valuations, infrastructure, the debacle in Texas, and a lot more.

Millions of Texans were without power this week when the state was hit with a record setting winter storm. An overhaul of its aging infrastructure would require massive amounts of metals and other materials, which would be positive for miners and producers.

In late 2020, a new kid emerged on the bargain-of-the-decade block. UK stocks, and notably UK value, reached very cheap levels relative to value stocks in other developed economies. Today, UK value remains at remarkably low valuations relative to most of its fundamentals.

A vaccine-fueled economic recovery and investors’ surging appetite for risk mean that the European equity rally can keep going in 2021, according to strategists.A vaccine-fueled economic recovery and investors’ surging appetite for risk mean that the European equity rally can keep going in 2021, according to strategists.

It’s tempting these days for some investors to question the role of fixed income in portfolios. After all, real yields have plunged, potentially leading to less income today and smaller capital gains tomorrow.

A brief monthly update on what's happening in the municipal bond market.

U.S. Treasury yields rose to the highest since February 2020 and are at risk of climbing further, as investors start to factor in the full economic impact of a stimulus plan totaling as much as $1.9 trillion.