Chief Economist Scott Brown discusses current economic conditions.

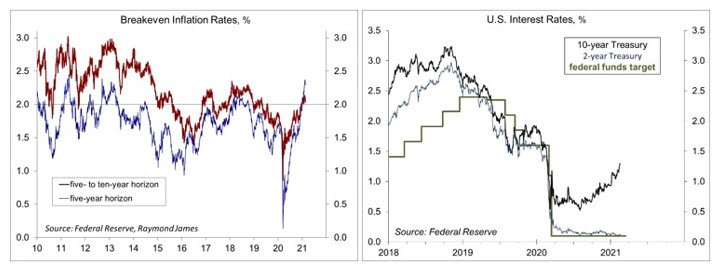

The details of the January Producer Price Index showed a further surge in prices of raw materials. Breakeven inflation rates (the yield spread between inflation-adjusted Treasuries and fixed-rate Treasuries) have continued to move higher. Retail sales were unexpectedly strong in January, fueled (apparently) by an increase in pandemic assistance, boosting fears that further fiscal support will add to inflation pressures. However, the outlook for consumer price inflation hasn’t changed much. Inflation fears have been a factor in lifting long-term interest rates, but bond yields should rise as the economy recovers.

It's important to recognize that it takes a gigantic increase in the prices of raw materials to have much of an impact on consumer price inflation. That’s because there are many other costs in bringing finished goods to market (such as labor, transportation, advertising, etc.). Moreover, services account for about 63% of the Consumer Price Index.

Economists do not fully understand the great inflation of the 1970s and early 1980s. The story we tell is that an oil price shock fed through to the overall consumer price inflation, lifting wage inflation and inflation expectations, accommodated by easy Fed policy. The double-dip recession of the early 1980s was necessary to wring inflation expectations down, but it was still a long battle for the Fed to win the public’s confidence as an inflation fighter. That battle has long been over. Expectations remain well-anchored.

Breakeven inflation rates, which aren’t exactly the same as inflation expectations (but close enough), have picked up from the lows of last year, but aren’t especially high (2.3% over the five-year horizon, 2.2% over the 10-year horizon). That is consistent with the Fed’s revised monetary policy framework. Following a period of inflation below 2% (as we’ve seen recently), the central bank will shoot for a period moderately above 2%. "Moderately” likely means 2.5% or 3%. Also note the breakeven inflation rates reflect expectations for the Consumer Price Index. The Fed’s 2% goal is for the PCE Price Index, which tends to trend a few tenths of a percentage point less than the CPI on a year-over-year basis.

Click here to enlarge

Retail sales jumped in January. While some of that reflects the seasonal adjustment (a smaller decline following a weak holiday shopping season), it appears to have been supported by the extension of unemployment benefits. While it’s still early, the retail sales figures have lifted expectations for 1Q21 GDP growth and added to fears that further fiscal support (Biden’s $1.9 trillion proposal) will add to inflation pressures. In fighting economic downturns, the mistake usually made is not doing enough or taking away support to soon. Erring on the side of doing too much may lift inflation somewhat in the short term, but should not have a long-term impact.

In his monetary policy testimony to Congress, Fed Chair Powell is expected to downplay inflation fears. We are likely to see the CPI rise to 3% y/y this spring, but that reflects a rebound from the low levels of a year ago. In the FOMC minutes, Fed officials “stressed the importance of distinguishing between such one-time changes in relative prices and changes in the underlying trend for inflation, noting that changes in relative prices could temporarily raise measured inflation but would be unlikely to have a lasting effect.”

Recent Economic Data

Retail sales jumped 5.3% in January (+7.4% y/y), up 5.9% ex-autos (+6.1% y/y). Some of January’s strength reflected a smaller decline in the unadjusted figures (-17.3%, vs. -18.5% in January 2020) following a weak holiday shopping season. However, unadjusted figures were still substantially higher than a year ago, suggesting that improvement was likely fueled by the resumption of extended unemployment benefits.

Click here to enlarge

Industrial production rose 0.9% in January (-1.8% y/y). Manufacturing output rose 1.0% (-1.2% y/y). Year- over-year results varied across industries. The index of oil and gas well drilling advanced 11.3%, following +8.3% in November and +10.3% in December, although still down 50.5% from a year ago.

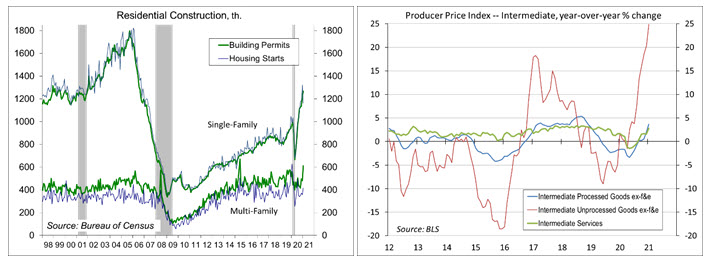

Building permits jumped 10.4% in January (+22.5% y/y), partly reflecting the usual volatility in the multi-family data. Single-family permits rose 3.8% (+29.9% y/y). Housing starts, which are reported much less accurately, fell 6.0% (-2.3% y/y), with single-family starts down 12.2% (+17.5% y/y).

Click here to enlarge

The Producer Price Index jumped 1.3% in January (+1.7% y/), up 1.2% ex-food, energy and trade services (+2.0% y/y). Wholesale gasoline prices rose 13.6% (+14.5% before seasonal adjustment, -11.4% y/y), following a 13.5% gain in December. Intermediate indices included in the report reflected a surge in prices of raw materials.

Import prices rose 1.4% in January (+0.9% y/y), up 0.8% (+2.6% y/y) ex-food & energy. Ex-fuels, prices of imported raw materials rose 4.3% (13.3% y/y). The index for consumer goods ex-autos fell 0.1% (0.1% y/y).

Gauging the Recovery

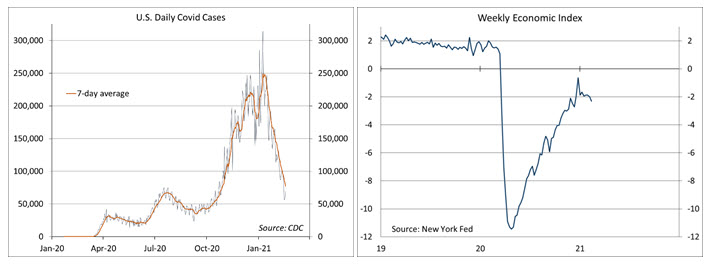

The number of new daily COVID-19 cases has continued to decline sharply, but from a highly elevated level in early January. The drop has led to a relaxation in social distancing directives, which should help the economy into 2Q21. The number of U.S. deaths from the coronavirus is nearing 500,000.

Click here to enlarge

The New York Fed’s Weekly Economic Index fell to -2.31% for the week ending February 13, down from -1.98% a week earlier (revised from -2.25%) and a low of -11.45% at the end of April. The WEI is scaled to four- quarter GDP growth (for example, if the WEI reads -2% and the current level of the WEI persists for an entire quarter, we would expect, on average, GDP that quarter to be 2% lower than a year previously).

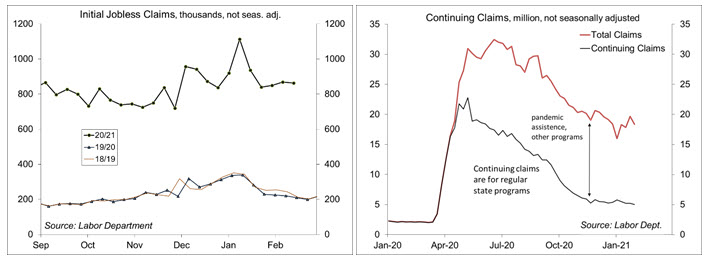

Jobless claims rose to 861,000 in the week ending February 13 (862,351 before seasonal adjustment), still very high by historical standards. The previous week was revised to 848,000 (from 793,000). Five and a half million claims have been filed in the first six weeks of this year (in comparison, unadjusted nonfarm payrolls fell by 2.8 million from December to January).

Click here to enlarge

The University of Michigan’s Consumer Sentiment Index fell to 76.2 in the mid-month assessment for February (the survey covered January 27 to February 10), vs. 79.0 in January and 80.7 in December. The report noted “the entire loss was concentrated in the Expectation Index and among households with incomes below

$75,000.” Surprisingly, “consumers, despite the expected passage of a massive stimulus bill, viewed prospects for the national economy less favorably in early February than last month.”

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

© Raymond James

Read more commentaries by Raymond James