Today’s low bond yields and high equity valuations have led many to jettison the traditional 4% initial safe-withdrawal rate (SWR) assumption. But I will show that the optimal “safe” withdrawal rate depends considerably on the retiree.

Today’s low bond yields and high equity valuations have led many to jettison the traditional 4% initial safe-withdrawal rate (SWR) assumption. But I will show that the optimal “safe” withdrawal rate depends considerably on the retiree.

Yields on 10-year U.S. government bonds are close to 1%, which is well below their long-term historical average yield of closer to 5%.

Lower assumed returns will reduce initial withdrawal rates (and increase required savings), ceteris paribus, and a growing body of research has suggested that 4% may no longer be a “safe” initial withdrawal rate for retirees.

While it’s definitely important to use expected returns in projections (don’t be lazy and use the historical long-term averages), it’s also critical to understand how adjusting other key assumptions will impact the results. For example: retirement doesn’t always last exactly 30 years, retirees can adjust withdrawals as needed, many retirees don’t increase spending annually with inflation, and common metrics (like the probability of success) don’t often accurately portray the impact of a bad outcome.

If I update returns to reflect today’s investing environment, then 3% (or even 2%) becomes the “new 4%”; however, depending on other assumptions and the preferences of the retiree, a 5% initial withdrawal rate (or higher) could work as well.

I acknowledge that 4% is a good starting point with respect to initial SWRs (i.e., you need 25-times your pre-tax portfolio income goal when you retire) because that’s what it should be … a starting place. But the optimal withdrawal rate will vary based on the unique preferences and situations of each retiree.

4% for all!

Early research by Bill Bengen resulted in what has become known as the “4% rule.”[1] This suggests a retiree can withdrawal 4% of the initial portfolio balance upon retirement, where that amount is increased by inflation (annually) for the length of retirement, which is assumed to last 30 years. This seminal work, along with other subsequent research, relied on historical returns, and the Ibbotson stocks, bonds, bills, and inflation data series (which goes back to 1926) was commonly used.

As bond yields declined, more recent research has shown that Bengen’s 4% estimate could be a tad optimistic. Lower assumed returns are going to result in lower SWRs, ceteris paribus; however, some of the key assumptions used in retirement spending models are worth revisiting before saying a permanent goodbye to 4%.

For example, researchers commonly assume a retirement lasts a fixed period, like 30 years. In reality, the retirement periods could be less than 30 years (a single, unhealthy individual), or longer (a married couple in excellent health). Using a fixed period for testing purposes also doesn’t capture “failure” because the true goal of retirees is not to maintain income over a fixed period, but to have income as long as they are alive. Mortality could be included as a stochastic variable in Monte Carlo simulations, but most planning software does not include this feature.

Additionally, the vast majority of retirement spending research and tools assume spending is static throughout retirement (i.e., constant in real terms). But spending is likely to evolve as the portfolio changes over time. As the balance goes up, spending can go up, and vice versa. Dynamic spending models can incorporate how spending evolves and are more realistic than static-spending approaches. Dynamic spending rules have been around for decades in the literature but aren’t common in financial planning programs.

Research and financial planning tools have also largely assumed portfolio withdrawals increase annually lock-step with inflation. My research looked at this and found that spending exhibits a “smile” shape throughout retirement in real terms. This means retiree spending tends to decline by 1% to 2% annually compared to inflation until around age 85, when spending potentially increases (significantly) if there is, for example, a health shock.

The fact that spending tends to decline (in real terms) during the first few decades of retirement is especially important because other income sources are typically tied to inflation, such as Social Security benefits. This means the required spending from the portfolio could be significantly less.

Finally, research on SWRs has largely used the “probability of success” (the percentage of Monte Carlo simulations that accomplish the goal) as the outcome metric. The probability of success metric is especially common in tools used by financial plans (again, Monte Carlo-type tools). A problem with success rate as the outcome metric is that it doesn’t capture the magnitude of failure. It is technically possible to fall $1 short in the final year of retirement (year 40!) and the strategy would be deemed to “fail.” But a retiree is likely to have other income sources, like Social Security retirement benefits, that could significantly lessen the impact of a portfolio shortfall.

A better approach than success rates is metrics that provide some perspective on goal completion. For example, what is the amount of income generated by a given strategy at age 95 (i.e., year 30 of retirement) in the worst 1-in-10 (or 1-in-five) outcomes? Focusing on the amount of income generated provides some context around what the total income will be if things go bad (e.g., it includes pension benefits). Just because a strategy “fails” (from a Monte Carlo perspective), it doesn’t mean the retiree is broke!

Safe-initial withdrawal rates

Using historical long-term average U.S. returns, the probability of success for a 4% initial withdrawal rate (assuming static, real withdrawals) is around 95% over a 30-year retirement period, assuming a balanced portfolio (e.g., 50% stocks, 50% bonds). The probability of success will decline if returns are reduced to reflect today’s investing environment.

For this analysis, I assumed the returns on bonds are 1% for the first 10 years of retirement and 4% thereafter, with a standard deviation of 7%. I assumed the return on stocks are 5.5% for the first 10 years of retirement and 8.5% thereafter, with a standard deviation of 16%. I’m effectively assuming a constant 4.5% arithmetic equity risk premium, which translates into approximately a 3% geometric equity risk premium, which is roughly consistent with long-term global averages. I assumed the correlation between stocks and bonds is zero and 50/50 portfolio allocation that is static throughout retirement. I also included a 0.5% portfolio fee and inflation of 2.2%.

Using these forecasted returns, the probability of success of a 4% initial withdrawal rate (static, real) over a 30-year period drops to approximately 50% (versus about 95% using historical long-term U.S. data). To get a 95% success rate, the initial withdrawal rate must be approximately 2.5%.

If I were to further reduce returns or assume a longer retirement period (retirees are living longer, after all!), a 2% initial withdrawal rate is realistic.

Does this mean 2% is the new 4%?

Not necessarily … let’s see how adjusting some of the other assumptions impacts the results.

I’m going to use a dynamic retirement-spending model where portfolio withdrawals evolve throughout retirement based on the portfolio value. The specific model is based on how RMDs are calculated (roughly one divided the assumed remaining retirement period, calibrated to the initial withdrawal amount). Next, instead of focusing on a single outcome metric (e.g., the probability of success), I will review and provide context on the entire distribution of income during retirement.

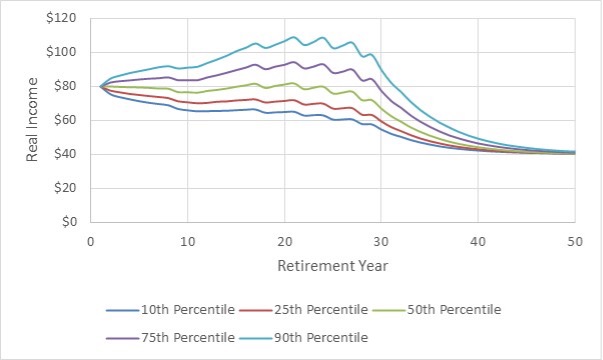

These results are below and assume a 4% initial withdrawal rate from a 50/50 portfolio with a $1,000 balance (i.e., the initial withdrawal is $40). I also included a $40/year assumed Social Security retirement benefit. The results in real terms (i.e., today’s dollars).

Distribution of portfolio withdrawals using a dynamic withdrawal model and forecasted returns

The median result has income of about $65 at year 30 (e.g., $65,000 assuming an initial balance of $1 million, in today’s dollars). The worst one-in-10 outcomes (10th percentile) has an income of $55 at year 30. Even when the portfolio fails, the retiree isn’t broke, because of the Social Security retirement benefits.

For retirees who need $80 in real income every year in retirement for 30+ years with a high level of certainty, 4% is not going to work, and a lower initial withdrawal rate would need to be selected (e.g., 3% or lower). However, this potential distribution of spending may be fine for retirees with significant pensions who can cut back on spending, if need be.

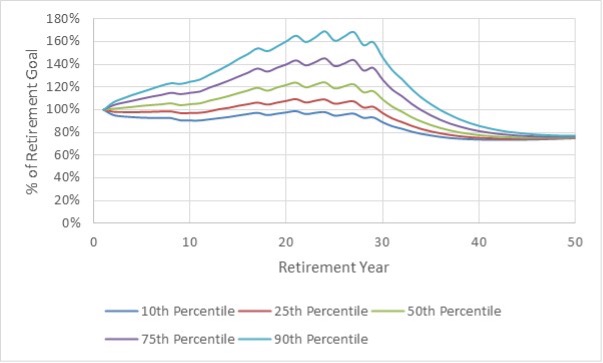

What if the portfolio spending goal is nominal, though, not real? In other words, what if Social Security retirement benefits are expected to cover the real increases in spending during retirement and the portfolio just needs to generate nominal income (i.e., an amount that doesn’t increase with inflation).

To make it easier to understand the results, I converted the distribution of income into the percentage of the goal that is completed. The results are included below.

Distribution of retirement goal attained using a dynamic withdrawal model and forecasted returns

When withdrawals don’t have to increase annually with inflation, a 4% initial withdrawal is pretty safe, even using forecasted returns. Even for the worst one-in-10 outcomes (10th percentile), the retiree will generate 89% of their retirement goal by year 30 – not too shabby.

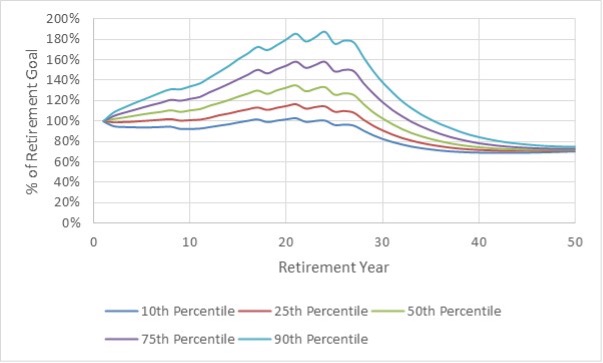

Let’s assume my return forecasts are too pessimistic, though. Perhaps they’re just too low and maybe a more diversified portfolio (e.g., with small cap, emerging market, etc.) would generate higher returns with the same level of risk and/or the advisor can generate some additional alpha (or all three!). I’m going to rerun the previous analysis but assume a 5% initial withdrawal rate, where the portfolio income goal is nominal, where returns are increased by 2% per year.

Distribution of retirement goal attained using a dynamic withdrawal model and forecasted returns

In this updated forecast, assuming a 5% initial withdrawal rate, the retiree still gets about 80% of the target income goal in the worst one-in-10 outcomes (10th percentile) at year 30. The median outcome is around 100% of the income goal. There’s also a good chance the income is significantly higher from years five to 25 of retirement. While I’m sure some retirees might not be okay with this potential distribution, I’m also sure there are many who would be. In other words, 5% all of sudden doesn’t seem so crazy.

I realize the results aren’t going to look as good if Social Security retirements benefit are reduced, but at the same time even a 5% withdrawal strategy can look overly conservative if the retiree has other forms of guaranteed income. Regardless, framing the analysis around cash flows (and goal completion), along with adjusting the target retirement need (to not increase annually with inflation), can result in a significantly higher initial target withdrawal rate.

Conclusions

While returns are likely to be below historical long-term U.S. averages in the near future (especially for fixed income; equities are more uncertain), that doesn’t necessarily mean advisors need to scare the bejesus out of retirees with incredibly low initial withdrawal rates (2%!!!).

Advisors must understand the key assumptions behind their projections and how they interact with the unique preferences and situations of each client.

Overall, 4% is an appropriate starting place for a conversation with retirees when it comes to “safe” initial withdrawal rates (i.e., required savings levels), because that’s just what it should be – a starting point. Some retirees are going to need more than 25-times their target-portfolio income level (1/4%=25) and some are going to need less. But one should not “prescribe” an initial withdrawal rate until you’ve appropriately “diagnosed” the client!

David M. Blanchett, Ph.D., CFA, CFP®, is head of retirement research for Morningstar’s Investment Management group and an Adjunct Professor of Wealth Management at The American College of Financial Services.

Views expressed are his own and do not necessary reflect the views of Morningstar Investment Management LLC. This blog is provided for informational purposes only and should not be construed by any person as a solicitation to effect or attempt to effect transactions in securities or the rendering of investment advice.

[1] Bengen, William P. 1994. "Determining withdrawal rates using historical data." Journal of Financial Planning, vol. 7, no .4: 171-180.

Read more articles by David Blanchett

Today’s low bond yields and high equity valuations have led many to jettison the traditional 4% initial safe-withdrawal rate (SWR) assumption. But I will show that the optimal “safe” withdrawal rate depends considerably on the retiree.

Today’s low bond yields and high equity valuations have led many to jettison the traditional 4% initial safe-withdrawal rate (SWR) assumption. But I will show that the optimal “safe” withdrawal rate depends considerably on the retiree.