Though rising yields may be indicative of an economic recovery, market volatility and inflationary fear could produce future hurdles.

Though the shortest month, February was long on optimism. Vaccinations increased in pace, and market consensus seems to be coalescing more around the idea of a strong economic rebound this year. Continuing accommodative policy from the Federal Reserve (the Fed) and the expectation that Washington will produce another round of fiscal stimulus play into the reaction we’ve seen in the market.

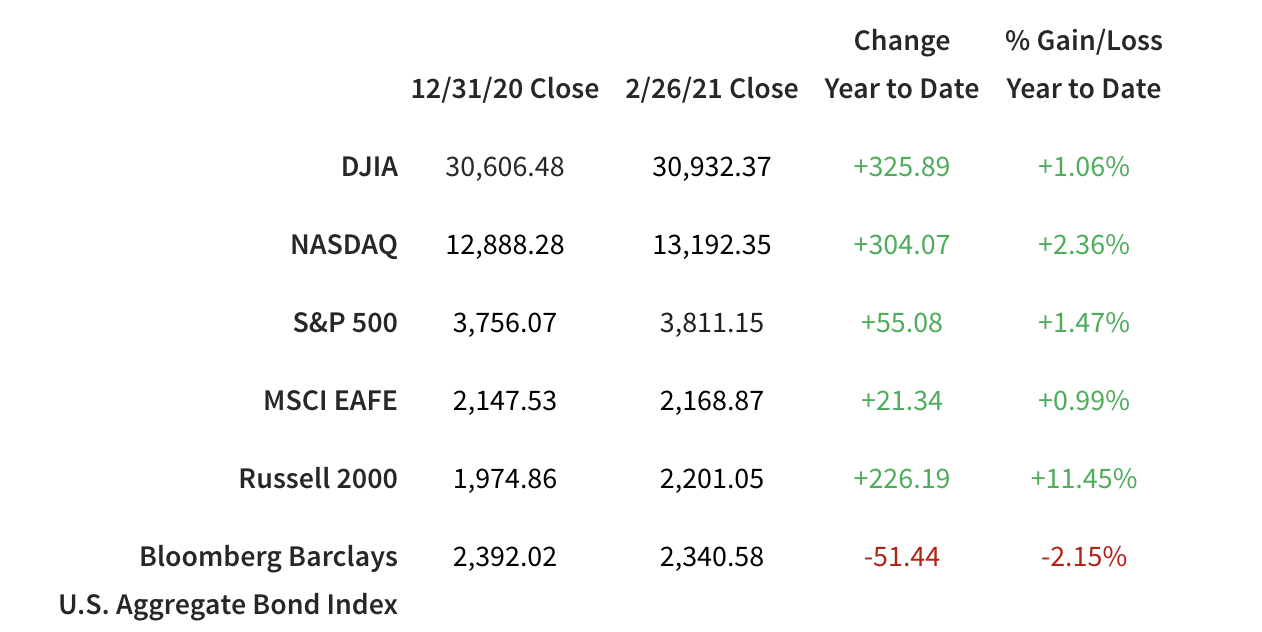

Through that, the equity market gained 2.8% with seven of 11 sectors in the green. Volatility was seen late in the month as the speed of rising rates caught the market off guard. The yield on the 10-year Treasury reached 1.46%, the highest level in a year, before settling back to end the month at 1.39% – but rising yields can be indicative of an economic recovery.

There has been, however, a turn to inflationary fears in some corners – which may be contributing to the rising long-term bond yields. One should always be cautious of too much market optimism, but Raymond James Chief Economist Scott Brown offers a counter argument to the simmering discussion.

“Within its revised monetary policy framework, the Federal Reserve will shoot for a period of inflation above 2% – following a period below 2%, as we’re seeing now – but the central bank remains firmly committed to its long-term goal of 2% inflation,” Brown said.

In the short term, Brown said he expects to see inflation rise to about 3% on a year-over-year basis, “but that simply reflects a rebound in prices that were held down during the lockdowns a year ago.” Market expectations of inflation for the next five years have risen rise to about 2.3%, but inflation is expected to settle to the Fed’s 2% goal in the five years to follow.

The reported unemployment rate of 6.3% understates the weakness in labor market conditions. Federal Reserve Chair Jerome Powell noted that the rate would be closer to 10%, adjusting for the decrease in labor force participation and classification issues, leaving the central bank “a long way” from achieving its goals. On a positive note, consumer spending is up after a lackluster holiday season, and manufacturing activity continues to improve, and in Europe, there is a comparable rising optimism, for similar reasons.

This optimism continued to flow into some of the sectors most beaten up by the pandemic. Unlike the mid-to-late 2020 “tech and then everything else” trend, there is now broader participation underlying the equity markets’ year-to-date advance. That’s a welcome development.

Performance reflects price returns as of market close on Feb. 26, 2021.

The $1.9 trillion question

The biggest hurdle to the passing of President Joe Biden’s $1.9 trillion stimulus package is a split among Senate Democrats over a proposed minimum wage hike to $15. This provision appears to be on the way out, but Washington Policy Analyst Ed Mills said he expects political pressure, and eyes to the consequential 2022 midterms, will create enough incentive to pass a bill close in value to the one initially proposed without the minimum wage increase. Discussions can be expected to turn toward an infrastructure bill, an administrative priority that will likely contain bigger policy decisions and a broader scope than a “road and bridges” package. Expect that debate to ramp up around late April and early May.

Fourth quarter earnings show strength

Most of the S&P 500 companies have reported fourth quarter earnings, with 79% beating estimates by an average of just under 15%, giving support to equity market performance.

Consensus estimates show earnings growth of 24% through 2021, but that could be a conservative view, said Joey Madere, senior portfolio strategist, Equity Portfolio & Technical Strategy.

“We see the potential for significant upside to this in the event of the economic reopening and the additional fiscal stimulus going as planned,” he said.

Climate orders limited by scope

The nature of executive orders, that they cannot change existing law and cannot spend money not appropriated by Congress, means the impact of two sets of climate change and energy orders signed by the new administration has been limited. Larger scale changes like the proposed net-zero CO2 emissions mandate, a carbon-free electricity mandate and $2 trillion in decarbonization spending would have to climb Capitol Hill, which is likely to be very steep on these issues, considering the tight majorities in both chambers and the relative power of moderates in this environment.

The energy sector continues to pay close attention to executive actions, but “other than a ‘pause’ on the issuance of new oil and gas leases on federal acreage, what the administration has done thus far comes under the category of narrow, technical or even symbolic,” Energy Analyst Pavel Molchanov said.

The bottom line

There are good reasons to be optimistic about the future and to look forward to a rebound once vaccinations reach a critical level, perhaps as soon as spring, but we’re far from a complete economic recovery.

Your advisor will continue to share any new developments that affect your financial plan. In the meantime, please reach out to them with any questions.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Raymond James Chief Investment Office and are subject to change. There is no assurance the trends mentioned will continue or that the forecasts discussed will be realized. Past performance may not be indicative of future results. Economic and market conditions are subject to change. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australia, Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. The performance mentioned does not include fees and charges which would reduce an investor’s returns. Small cap securities generally involve greater risks. Companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

© Raymond James

Read more commentaries by Raymond James