Investment managers produce annual equity return forecasts, and the consensus is much more pessimistic than that of academics. I’ll take a closer look at why the forecasts are so different and the implications for advisors working with clients.

Investment managers produce annual equity return forecasts, and the consensus is much more pessimistic than that of academics. I’ll take a closer look at why the forecasts are so different and the implications for advisors working with clients.

The most important assumption in financial planning is the future portfolio return, and future stock returns are the most uncertain component. The most structured way of creating stock-return forecasts goes back to the Graham and Dodd dividends-plus-growth approach. Roger Ibbotson has been the key academic researcher in refining the Graham and Dodd model, and his work over the past 20 years with other researchers has produced long-term forecasts of stock returns that are close to historical averages.

However, prominent investment managers’ forecasts are much lower, and I will explain why.

Definitions

Before getting into the forecasts, we need to sort out some confusion over return definitions. There are a variety of ways to calculate returns and, unfortunately, those making predictions often fail to be precise about what they are forecasting. We hear predictions like, “I expect stocks to average about 9%.” But we don’t know if this prediction includes dividends or just reflects price appreciation. Is this a nominal return (including inflation) or a real return with inflation removed? Further, we don’t know if this predicted “average” is a simple average of future yearly returns (an arithmetic average) or if it is based on a compounding of future yearly returns (geometric average).

It’s straightforward to explain returns with and without dividends and nominal versus real returns, but forecasters often leave out their assumptions for dividends or inflation, and this creates confusion. For example, if one wants to convert a nominal return forecast to the underlying real return, there’s the question of whether to subtract historical inflation (about 3%) or market-based forecasts of future inflation (about 2%). This will depend on how the forecaster originally built their forecast, which may not have been stated.

Less straightforward is developing an understanding of arithmetic average returns versus geometric or compound returns. If we take the yearly real returns for large-company U.S. stocks going back to 1926 from the Ibbotson data and calculate a simple average of those 95 returns, we get 9.22%, which is the arithmetic average. We might also ask the question, “What annualized return would an investor have earned on a lump sum invested at the beginning of 1926?” To do the calculation, we add a one to each of the annual returns (creating what are known as return relatives), calculate the product of the return relatives, apply the 1/95th power, and finally subtract 1. The result is 7.25%, which is called the geometric average, or compound return.

For any series of returns that vary from year to year, the geometric average will be less than the arithmetic average, and for durations longer than 20 or so years, the difference can be approximated as one-half the standard deviation squared or variance. For the historical returns in this example, the standard deviation is 20% so the approximation comes close to the actual difference.

When forecasters refer to “expected returns” or “average returns” we don’t know whether they are talking about arithmetic or geometric, and oftentimes they don’t know themselves. There would be much less confusion if those making predictions defined what they are predicting.

Ibbotson and affiliated researchers

Over the past 20 years, Ibbotson has worked with other researchers in refining the Graham and Dodd “dividends-plus-growth” approach, both in explaining the sources of past stock returns and estimating future returns. Key studies include Ibbotson and Chen (2003), Ibbotson and Straehl (2017), and Laurence Siegel (2018). Those authors have provided in-depth analysis and carefully defined their return measures, an example others should follow.

The basic principle underlying these studies is that stock returns are composed of:

- Cash paid to owners (historically dividends);

- Growth of such payments; and

- Change in the valuation of future payments.

This is a “supply-side” approach in that it focuses on funds supplied to stockholders and their growth trajectory. This is contrasted with “demand-side” approaches that focus on return premiums investors require to invest in risky assets.

The historical (1926-2020) geometric average real return of 7.25% noted earlier can be split into an average dividend yield of 3.77%, growth of 2.48%, and valuation change of 1.00%. This last element is based on the change in the CAPE or Shiller P/E measure since 1926; investors are now paying more for future cash flows from stocks than the 95-year average. These percentages are a rough split of sources of return, and the studies offer much more refined breakdowns. In particular, they recognize that over the past 40 years stock buybacks have partially replaced dividends in returning cash to investors.

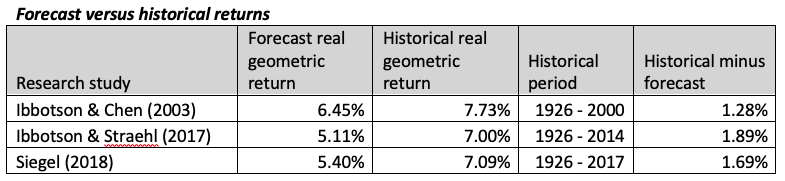

In each of the studies, the authors have provided their estimates of long-term future returns on large-company U.S. stocks, and the following chart compares these estimates with historical average returns from 1926 to when each of their studies were completed.

All three forecasts utilized versions of the supply-side approach with values of components based on either long-term history or more recent results as the authors deemed most appropriate. In addition to dividends, the authors included the effect on returns of stock buybacks, and Siegel also estimated the additional impact of cash acquisitions. These forecasts of long-term returns assumed market efficiency in that they did not build in an assumption for future valuation changes. Therefore, returns are based on the funds paid to stockholders and the growth of such payments.

The historical returns exceed the forecast returns by 1.28% to 1.89%, depending on the forecast. However, the historical returns include a valuation change component that I estimated at 1% per year. If I exclude this, the differences between historical and forecast returns are less than 1%. These forecasts project that the cash flows from corporations to stockholders will continue to generate attractive returns.

At the end of each of the papers, the authors note that they have produced geometric or compound returns, and those doing Monte Carlo forecasting and generating yearly returns need to convert their estimate of the average to an arithmetic return. This can be accomplished by adding half the assumed variance, which works out to 2% based on a historical 20% standard deviation (5.4% geometric becomes 7.4% arithmetic).

In all three studies, the authors noted that their forecast returns were significantly more optimistic than other studies that were published at the same time. In his 2018 study, Larry Siegel paraphrased Mark Twain in declaring that “the death of future equity returns has been greatly exaggerated.”

Investment manager forecasts

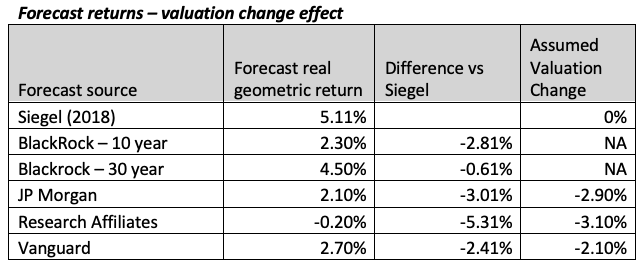

Each year, Christine Benz, the director of personal finance at Morningstar, provides a valuable summary of the asset-class return forecasts from investment managers, including links to supporting material. In the chart below, I compare the latest forecasts from a subset of managers versus Larry Siegel’s 2018 forecast. These are for large-company U.S. stocks, and I have converted the nominal returns in Christine’s summary to real returns based on inflation estimates provided in the supplementary material from the investment managers.

The managers I chose all utilized a supply-side approach for predicting future returns, but what intrigued me was that they were forecasting much lower returns than Siegel and the earlier Ibbotson-related studies. As it turns out, the key difference is that the investment managers all assume a significant hit to returns from future valuation changes.

These forecasts are typically medium-term (about 10 years) rather than long-term, so the impact of valuation change merits more attention. JP Morgan, Vanguard, and Research Affiliates provided specific estimates in their supporting material of the impact on projected returns of valuation change. JP Morgan and Vanguard’s assumptions for the impact of valuation change explains most of the difference between their forecasts and Larry Siegel’s. BlackRock provided forecasts for different durations but did not provide a specific valuation-change assumption for its 10-year and 30-year forecasts. It did estimate a valuation-change return impact of minus 5.8% annually in its five-year forecast, so it’s certain that at least its 10-year forecast contained a significant impact as well. Its 30-year forecast, with any underlying valuation change spread over a longer period, is not far below Siegel’s long-term forecast based on zero valuation change.

The outlier in this chart is Research Affiliates – its forecast is much more pessimistic and assumed valuation change explains only about 60% of the difference versus Siegel. It also takes aim at the growth component, and challenges growth models relied on by others. For example, it notes that, “earnings and dividend growth have always been meaningfully slower than overall economic growth,” and points to such contributing factors as net dilution of shares and poor management decisions in the deployment of capital.

I characterize the different forecasts as follows:

- Research Affiliates highly skeptical about market efficiency;

- Ibbotson-related forecasts assuming significant market efficiency; and

- the other investment manager forecasts falling in between.

Choosing a forecast to rely on depends to a large extent on views about market efficiency. Overall, except for Research Affiliates, both the older and newer forecasts are reasonably consistent in estimating future contributions to returns from cash flow to stockholders and growth. The main differences are in the valuation change component and to some extent the forecast timeframe.

Valuation change uncertainty

The investment managers’ forecasts discussed above are reasonably consistent in predicting lower stock returns that reflect the elevated CAPE in the mid-30s. However, the CAPE measure is not adjusted for current interest rates. If we invert the CAPE ratio, it produces an earnings-yield measure of about 3%. Although low by historical standards, this earnings yield provides a significant margin over risk-free real interest rates (TIPS yields), which are below zero. So perhaps the future for valuations is not quite so ominous. Robert Shiller, who brought CAPE to prominence, has recently been promoting this inverted measure, which he calls excess-CAPE yield.

Shiller was not the first to propose a yield measure. The Ibbotson-related studies discussed earlier produced a measure called cyclically adjusted total yield (CATY), based on cash returns that stockholders receive.

Unfortunately, there’s no good way to make a firm judgement based on history about how to incorporate low interest rates in stock-return forecasts. There are so many moving parts in the financial world that one cannot look back and find a time when all the variables lined up similarly to today.

Conclusion

What should advisors do when selecting stock return assumptions to use in preparing projections for clients? Focusing on yield measures rather than PEs, plus assuming continuing healthy income and growth measures, may give cause for cautious optimism. But even if we can get comfortable with a more optimistic view, the inherent year-to-year volatility of stock returns will still leave a wide range of potential outcomes in making projections for clients. Any uncertainty about future average returns adds another layer of forecast variability. The most important issue for advisors is not the point estimate for future average returns, but how to deal with the range of potential outcomes.

Running Monte Carlo simulations is useful in showing potential ranges. To recognize the additional uncertainty in average stock return assumption, it is useful to also run separate simulations assuming different average returns.

Regardless of the approach, focus not on just the middle-range outcomes, but also on the lower percentiles, for example, getting into detailed discussion with clients about how their retirement plan would work out based on a 10th percentile outcome. Would they be okay with the planned stock allocation or should they opt for a heavier allocation to fixed income, more lifetime income, or maybe even setting up a reverse mortgage line-of-credit? Those are the questions advisors and clients need to consider. Building resilient plans adds a dimension to the value advisors can provide.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire, England. He thanks Philip Straehl and Larry Siegel who have been very helpful in explaining nuances of the supply-side approac

More Fixed Income Topics >

Investment managers produce annual equity return forecasts, and the consensus is much more pessimistic than that of academics. I’ll take a closer look at why the forecasts are so different and the implications for advisors working with clients.

Investment managers produce annual equity return forecasts, and the consensus is much more pessimistic than that of academics. I’ll take a closer look at why the forecasts are so different and the implications for advisors working with clients.