After the disruptions of the past few years, many of us are looking for a return to normal. For investors in emerging-market bonds, normal would mean a world in which global inflation is in check, interest rates are no longer rising, China is healthy, and traditional asset correlations resume.

Evan Harp sat down with financial advisor Ramona Maior. Maior reflected on how financial advisors can better serve LGBTQ+ clients. She offered a number of quick and useful tips for advisors.

Aggressive monetary policy tightening in developed markets led to a drawdown in house prices in 2022, but not a meltdown.

A month or two ago, people were having a conniption about commercial real estate. An absolute meltdown.

Financial advice often focuses on boosting personal savings rates and maximizing return on investment during a worker’s accumulation years. Equally important, however, is the decumulation process, when people spend those savings in the form of income.

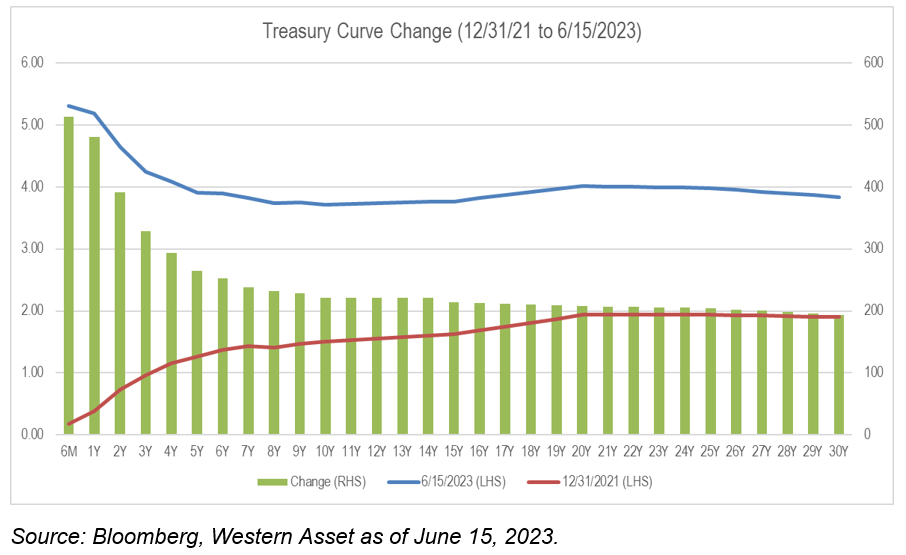

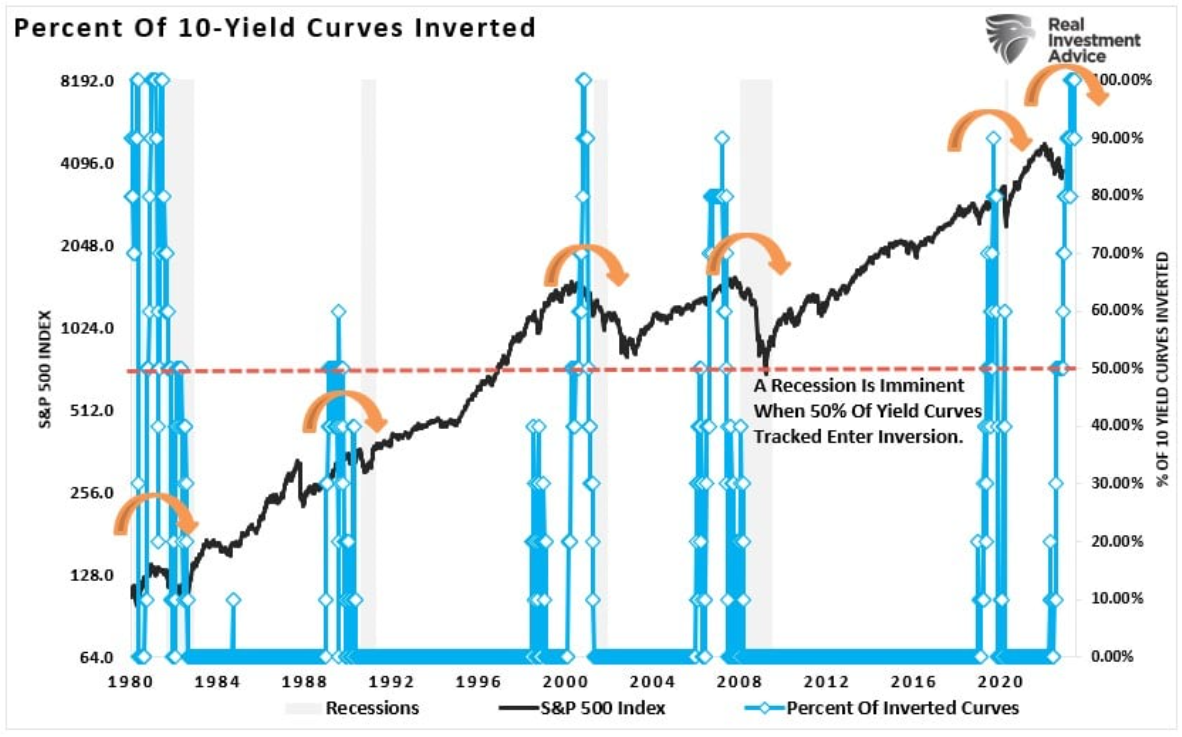

We review the key themes of the first half of a busy year.

Activities that help companies avoid emissions are an attractive investment opportunity, according to Templeton Global Equity Group Portfolio Manager Craig Cameron. By actively seeking opportunities to reduce emissions, he says investors can align themselves with sustainability goals that contribute to a low-carbon economy.

The Federal Reserve (Fed) still has a very tough job ahead to bring inflation down to its 2% target over the long run while facing pressures from markets, which have a very different timetable than the Fed.

The World Silver Survey is an annual report published by The Silver Institute since 1990. It provides market participants with supply and demand statistics for critical sectors of the silver market, along with price and trade data.

The European Central Bank (ECB) hikes rates and signals more tightening ahead.

After falling into its own recession last year, the housing market has started to turn decisively higher; but a sustained recovery might not be the strongest elixir for the economy.

In this article, we’ll closely examine the EM bond ETFs that have performed the best over the past year.

In a hawkish move coming on the heels of data that showed a reacceleration in inflation, the Bank of England raised its key lending rate by 50 basis points at today’s policy meeting.

1969 is often remembered as one of the biggest years in pop culture history.

After yesterday’s testimony by Fed Chair Jerome Powell to the US House of Representatives I analyzed its sentiment on key issues compared to his previous four FOMC policy statements, using ChatGPT. The table below shows the results.

Howard Marks (Co-Chairman) and David Rosenberg (Co-Portfolio Manager, U.S. High Yield, Global High Yield, Global Credit) discuss topics from the June 2023 edition of The Roundup. They consider the evolution of the high yield bond market, investor optimism, and why this time might actually be different in financial markets.

Sam Weitzman of Western Asset Management highlights the overlooked potential of municipal bonds as a high-quality asset class. With fixed income yields reaching near-decade highs and higher tax rates impacting taxable fixed income investing, municipal bonds are offering above-average after-tax returns and downside protection, making them attractive for income seekers.

Striking the right balance between interest rate and credit risk can be a good idea in the late stages of a credit cycle. We think it’s a particularly good idea in this credit cycle.

We expect generally good performance during the second half of the year, although volatility may increase, especially for high-yield bonds.

The US Federal Reserve (“Fed”) paused rate hikes in June, but signaled it expects to deliver 50 basis points of additional hikes this year.

While a severe hurricane for the global economy looks less likely than a few months ago, we are still likely to encounter a tropical storm that could cause significant damage. Much will depend on how major central banks confront the trilemma of simultaneously maintaining price, growth, and financial stability.

With June being Pride Month, advisors and market participants are paying renewed attention to strategies relevant to the LGBTQ+ community.

This past Wednesday marked the official start of summer! The summer solstice represents the best time of year – the maximum amount of daylight coupled with warm temperatures.

“Signs” was a song by the Five Man Electrical Band in 1970 about the hippie movement. The song came to mind as I was looking at the economic data recently.

Today we’re going to look at two stocks – Visa vs. Mastercard – that seem to be oblivious to that. Frankly, they’re two better-performing companies from a standpoint of operating results but also from the standpoint of price as pointed out in the original video.

In this article, we will delve deeper into some of the top-performing Japan ETFs, analyzing their YTD performance. We will also discuss whether advisors and investors should consider investing in them.

We get a big bunch of data reports this week: GDP revisions and economy-wide corporate profits for the first quarter; durable goods, new home sales, personal income, and consumer spending for May; home prices for April.

An ounce of optimism, a pound of prudence. It’s still a good time to be measured about taking risks in equities, but we believe the longer-term horizon holds particular promise for active stock pickers.

After an outstanding 2022, global liquefied natural gas (LNG) prices have weakened in 2023. However, the long-term outlook for LNG remains constructive as customers continue to sign 20-year purchase agreements with US exporters. This note discusses growing US LNG export capacity and how this benefits midstream companies.

The Northern Trust Economics team shares its outlook for U.S. growth, employment, interest rates, and inflation.

Today's U.S. equity market is highly concentrated, with seven stocks contributing to an astonishing 96% of the Russell 1000 Index's year-to-date return.

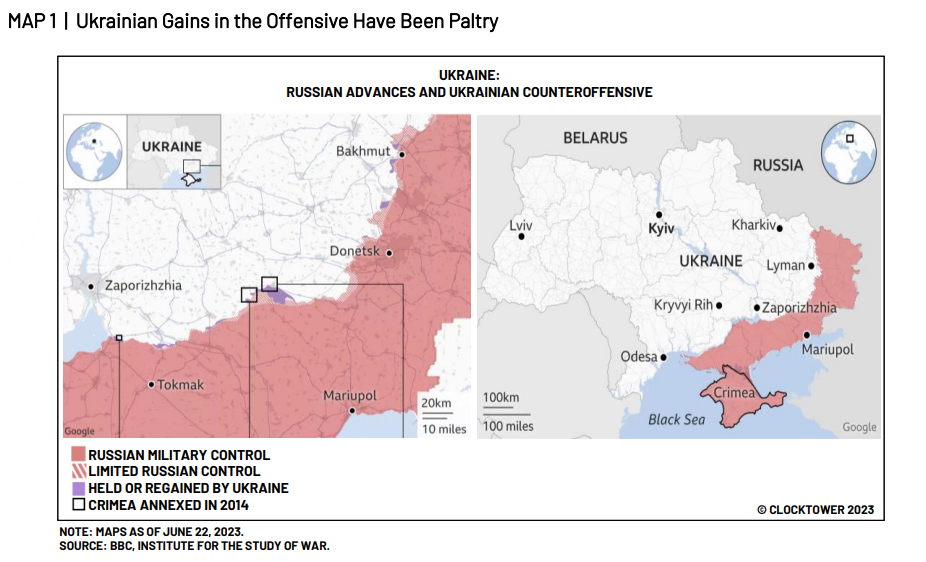

We continue to watch the fascinating developments in Russia. While the coup has failed and Yevgeny Prigozhin is either in exile or meeting a worse fate, the reality of the situation is that Russia is on a path to internal strife.

Stress in the banking sector — whether or not more banks fail — remains an area of concern for us because of potential implications for the Treasury and agency MBS markets.

The current market speculation surrounding artificial intelligence (A.I.) has garnered everyone’s attention.

This article will cover some of the top small-cap ETFs based on their year-to-date (YTD) performance.

Today the minutes of the April 27-28, 2023, Bank of Japan meeting were released. Below in italics are the top ten highlights generated by our AI engine.

Heading into 2023, a looming recession dominated the headlines.

Macroeconomic uncertainty has remained front and center in 2023 as the new investment regime continues to play out. Inflation remains above central bank targets and some signs of economic weakness have started to surface in the wake of rapid monetary tightening.

Volatile input prices have been a major inflationary force.

The complexity of some risk management platforms can lead to a steep learning curve for institutional investors, draining resources and creating stress.

Is recession still coming? Of course. But some funny things are happening on the way there.

Imagine a new digital environment where our data is portable and democratized, challenging the current monopolies. Web3 promises to be such an environment, using blockchain technology.

Exchange Advisor Council members Anna N’Jie-Konte and Keith Beverly have merged practices. The two advisors have set their sights on the goal of creating the first black-owned RIA with over $1 billion in client assets.

To recap, we tested the following metrics, drawn from each company’s fiscal year-end reports and stated in USD, and correlated them with the percent price return in local currency over the past five years.

Since the March trough the S&P 500 Index has gained around 14% and ten-year Treasury yields have risen roughly 0.50%. As market conditions have improved, inter-asset correlations have also shifted.

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

The exit from a decade of very low interest rates, via the most aggressive hiking cycle since 1980 has laid bare the distorted financing incentives that became entrenched in the years between the Global Financial Crisis in 2008 and the end of pandemic-era monetary policies in 2022.

This article will explore the expense ratios and YTD returns of four ETFs investing in AI with some of the lowest fees in the market. By comparing these key metrics, investors can evaluate which ETF may be the most cost-effective option for gaining exposure to the AI industry.

Japanese stocks may help boost the performance of international markets although the unique nature of Japan's economic and business structure could pose some risks.

Though recent data suggests China's re-opening growth has slowed, it's likely temporary. As China's recovery continues, it may have implications for U.S. inflation and rates.