Heading into 2023, a looming recession dominated the headlines. Moody’s Chief Economist Mark Zandi quipped at the time, “CEOs are falling over themselves to say we’re falling into a recession. . . . Every person on TV says recession. Every economist says recession. I’ve never seen anything like it.” Fast-forward to today at the midyear point of 2023, and the data is telling a different story.

Inflation has fallen by 2.5 percent, more than 1.8 million jobs have been created in the past six months, and the S&P 500 has had one of its best starts in 25 years. Many investors are now asking, what happened to that recession? Let’s take a look back at how we got here—and what we can expect for the rest of the year.

Strong Start to 2023

Although many economists were firmly in the recession camp at the close of 2022, Commonwealth’s Investment Management team foresaw a Goldilocks economy (i.e., an ideal state with full employment, economic stability, and stable growth) and believed there were tailwinds for growth.

Indeed, we did see a very strong first half. And there’s reason to believe that the tailwinds will continue to blow through year-end, specifically those related to inflation, employment, and the consumer.

Inflation: Prices Stabilizing

Inflation was a contributing factor to consumer and investor skepticism in 2022. But over the past 12 months, it has continued to moderate toward the Fed’s mandate of 2 percent (see chart below). Prices on common expenditure areas like butter, milk, and gasoline have declined 20 percent, 34 percent, and 36 percent, respectively, over the past year.

Overall, inflationary pressures should continue to moderate in the coming quarters as supply-demand dynamics balance. The result should be a reprieve for Americans at the pump, grocery stores, and elsewhere, ultimately putting more money back in the consumer’s pocket.

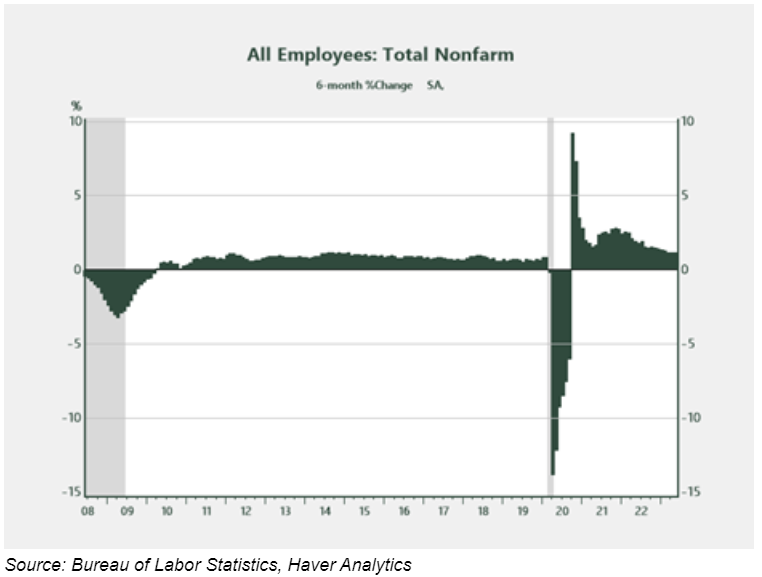

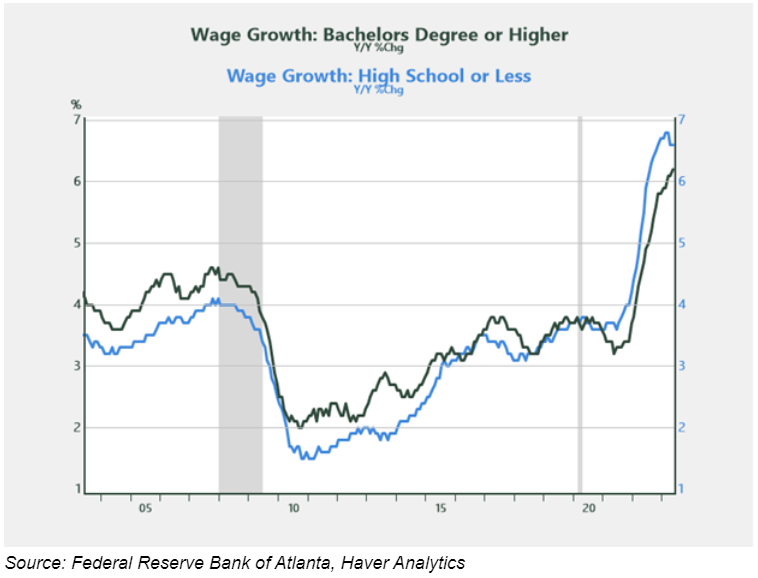

Employment: Labor Demand and Wages Growing

Over the past 12 months, the economy has added 4 million jobs, with approximately 40 percent of those gains occurring in the first five months of 2023 (see chart below). The mismatch between labor demand and supply is the largest on record, with 10 million job openings compared to only 5.7 million unemployed.

This strong demand for labor has resulted in above-average wage growth, especially for those in lower-skilled occupations (see chart below). After years of lackluster wage gains, many individuals are now seeing more dollars in every paycheck, which is contributing to the spending patterns experienced as of late.

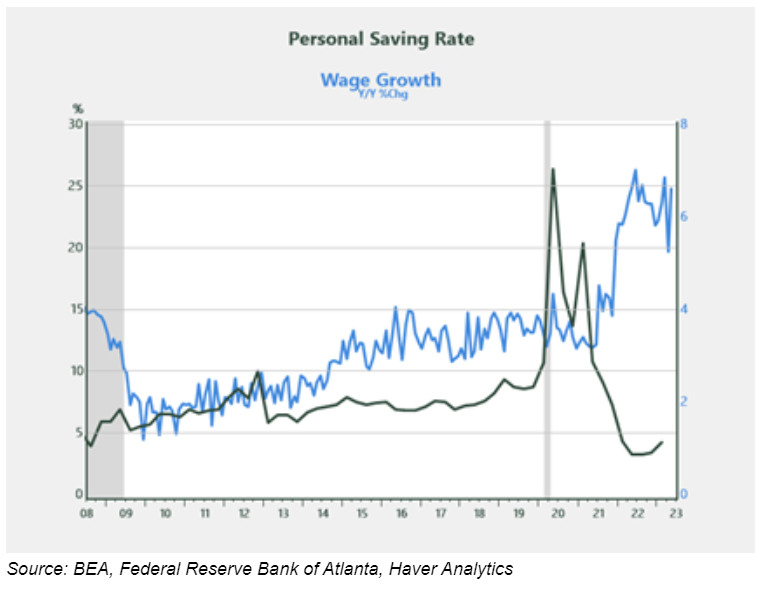

Consumers: Spending Rising, Savings Falling

With more dollars in every paycheck, consumers are spending. Plus, they’re doing so at a pace that’s above historical norms, as evidenced by the decline in the personal saving rate in recent periods. Since the pandemic, Americans have been on a spending spree, which began with purchases on goods and has since moved toward services like leisure, travel, and hospitality.

The surge in spending bodes well for an economy that is approximately two-thirds consumption. Unless there’s a significant uptick in the savings rate in the coming months coupled with a decline in consumer confidence, it’s reasonable to assume that the economy will stay on track as it did in the first half of 2023.

Trending Toward Half Full

Heading into the year, many believed the economy was half empty, with the likelihood of recession right around the corner. With the benefit of hindsight, however, we know that it was half full, following a 3.9 percent increase in GDP in the first quarter and strong equity gains year-to-date. There’s reason to believe that the trend will continue.

The job creation rate in the past six months is greater than any six-month period in the decade before the pandemic. Wages are following suit. Americans are working more, earning more, and spending their hard-earned dollars, which is a win-win from an economic perspective. With a significant breakdown in confidence between now and the end of the year being an unlikely scenario, the positive momentum should continue.

Disclosure

The information on this website is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets.

The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. All indices are unmanaged and investors cannot invest directly in an index.

The MSCI EAFE (Europe, Australia, Far East) Index is a free float‐adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Index consists of 21 developed market country indices.

One basis point (bp) is equal to 1/100th of 1 percent, or 0.01 percent.

Third-party links are provided to you as a courtesy. We make no representation as to the completeness or accuracy of information provided on these websites. Information on such sites, including third-party links contained within, should not be construed as an endorsement or adoption by Commonwealth of any kind. You should consult with a financial advisor regarding your specific situation.

Member FINRA, SIPC

Please review our Terms of Use.

Commonwealth Financial Network®

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Commonwealth Financial Network

Read more commentaries by Commonwealth Financial Network