Key Takeaways

- The Fed’s tightening cycle may not be over

- Earnings trends will be key to watch for equity direction

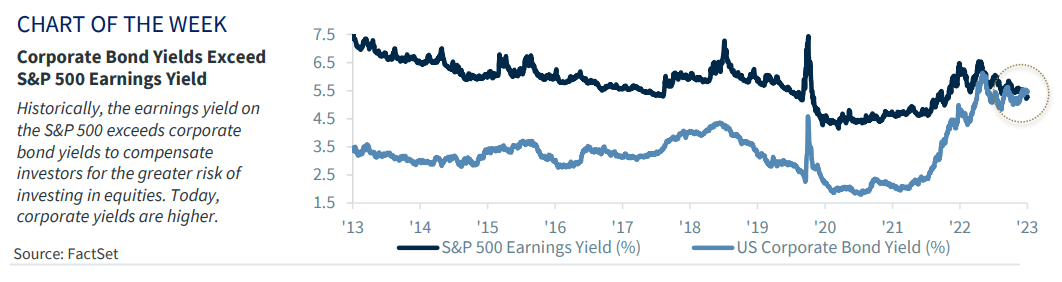

- Corporate bond yields exceed S&P 500 earnings yields

This past Wednesday marked the official start of summer! The summer solstice represents the best time of year – the maximum amount of daylight coupled with warm temperatures. In many ways it's the perfect season – school’s out, family vacations, barbeques and beach trips! It sure is fun, that is, while it lasts. And speaking of the maximum sunlight, the sun has been shining on the S&P 500 the last several weeks as it sits just below our year-end target of 4,400. A better-than-expected Q1 earnings season, decelerating inflation, growing optimism about a soft, non-recessionary landing, the AI-powered tech rally, and the Fed nearing the end of its tightening cycle have been key drivers behind the recent upswing. However, with much of the good news now priced in, the equity market is in a more vulnerable spot, susceptible to disappointment. Below are some catalysts that we’re watching to gauge the next direction for the markets:

The sun may not have set on the Fed’s tightening cycle

This week, the markets had a chance to hear directly from Fed Chair Powell and several other Fed officials after last week’s hawkish shift in the dot plot. Powell maintained a hawkish tilt during his semi-annual update to Congress, reiterating the Fed still has more work to do to bring inflation down to the central bank’s 2.0% target. There were mixed comments from other Fed officials, but one common thread emerged and that is, rate cuts are a long way off. Persistently high core inflation data (most recently at 5.3%) has unnerved Fed policymakers, but that is to be expected as they try to calibrate the right amount of restraint needed at this point in the cycle. With the economy still showing signs of resilience and core inflation sticky, it is not surprising the Fed wants to keep its options open for further rate hikes. That is why our economist is now calling for one additional rate hike, with the fed funds rate now expected to peak at a top rate of 5.50%. This, combined with the global flurry of interest rate increases from the UK, Swiss, Europe, Australia, Canada and Norway central banks, remains a key risk to further upside in the equity markets – particularly since central banks have a history of ‘over’ tightening.

Will earnings take another dip or will it be smooth sailing?

As we discussed in prior Weekly Headings, the earnings recession that plagued the market for much of the last year has shown signs of stabilizing. Turns out that analysts were way too pessimistic – just as we forecasted. The resilience of the economy, cost-cutting measures (i.e., layoffs) and disinflationary trends that boosted margins and growing enthusiasm around AI helped put a floor under the declining earnings trends. In fact, the S&P 500’s forward earnings estimates bounced off their recent lows of $226 to ~$232 as the corporate profit outlook brightened. This has contributed to the broader risk-on trend in the markets over the last few weeks, which admittedly, is likely stretched – at least in the near term. In a few weeks' time, we will flip the page to second-quarter earnings season and will monitor whether companies will be able to sustain these trends in the wake of more challenging consumer and economic headwinds. Early reporters have flagged weakening demand (FedEx), a difficult macro environment (Darden Restaurants) and lower tech spending (Accenture).

Recession concerns still cast a dark cloud

The debate about when the recession will begin, if one will begin at all, is likely to dominate news headlines until there is definitive evidence that the labor market is cracking. While there have been signs of cooling labor demand (i.e., rising trend of initial claims, increased corporate lay-offs, fewer people voluntarily quitting their jobs, slowing demand for temporary workers, and a declining number of hours worked) the labor market remains strong by any historic standard. In fact, this is a key reason why our economist recently pushed out the likely beginning of recession from Q3 to Q4 2023. But as we have stated in the past, we remain skeptical that the recent strength can continue and believe that the payroll data may be overstating job growth – particularly given the noise between the establishment and household surveys. And we are expecting there to be a strong slowdown in job creation over the coming months. This, plus the ongoing deterioration in the Conference Board’s leading economic indicators, which has fallen for fourteen consecutive months, suggests that a recession is more likely than not. With equity markets rallying on hopes of a soft landing, disappointing economic news could lead to a potential setback.

Hot bond yields could challenge equity flows

After the massive reset in interest rates last year, bonds look increasingly attractive versus equities. With the recent rally in equity market, the S&P 500 earnings yield (the inverse of the price-earnings ratio) has fallen to 5.3%. Compare that to the 5.5% yield on the U.S. corporate bond index or the 5.1% yield on cash instruments and suddenly stocks look a little less attractive on a relative basis. While equity flows have recently increased as investors chase the strong returns of the last few weeks, we suspect this dynamic could reverse, particularly if economic data disappoints.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Raymond James

Read more commentaries by Raymond James